Published on April 4, 2024 by Jeetendra Prakash, CFA and Mohit Choudhary

-

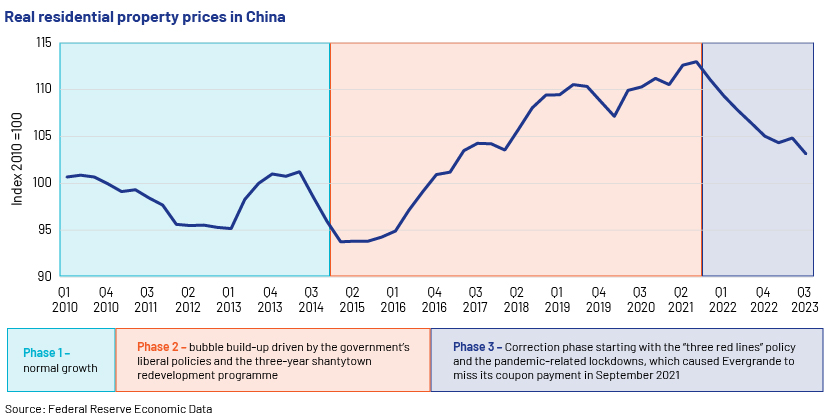

China’s real estate sector is slowing down. The effect on the economy is magnified, as the sector contributes the most (c.30%) to GDP and is highly leveraged, with real estate debt/GDP at c.28%, the highest in the world

-

More than 50 real estate developers, accounting for c.40% of China’s home sales, have defaulted since 2020, driven by the government’s close regulation of the sector through the “three red lines” property rules and later, the slowdown in sales due to the pandemic

-

The real estate total return index for Chinese dollar bonds was down 29% in 2022 and declined further to 31% in 9M 2023, in stark contrast to the positive returns on bonds of China’s other sectors

-

The government is trying to engineer a soft landing by introducing measures to support the sector, which, if successful, would open up opportunities for investors looking to de-risk and improve portfolio returns

Real estate – an important cog in China’s bond market

China’s real estate sector has USD5tn of debt outstanding, accounting for c.28% of the country’s GDP (vs 16% of GDP for the US and 7% for the UK). However, with rising rates and liquidity shortages, the sector has witnessed an unprecedent wave of defaults since 2020. Weak sector activity remains a drag on local governments too, as the sector accounted for 35-40% of total fiscal revenue of all local governments and generated the most employment.

What led to the downfall?

China’s policymakers have used the real estate sector time and again to drive growth or pull the economy out of a slump, implementing multiple measures such as low interest rates, tax cuts, stimulus packages and increasing land supply. These have incentivised real estate developers to increase leverage and buyers to increase purchases.

As risks in the sector increased, regulators stepped in, first by restricting purchases of second homes (to curtail speculative purchasing) and then reducing credit supply (in the form of the “three red lines” rules in August 2020). Furthermore, new-home sales declined when the pandemic hit in 2020. This, coupled with the regulatory restrictions, exposed the sector’s fragility.

In 2020, more than 90% of properties sold in China were only on paper versus an actual completion rate of 60%[1], indicating the scale of speculative purchases. Given the lack of credit supply and the slump in new sales, project completions were delayed, leading to a number of big-ticket defaults.

High default rate and low recovery in China’s real estate bonds

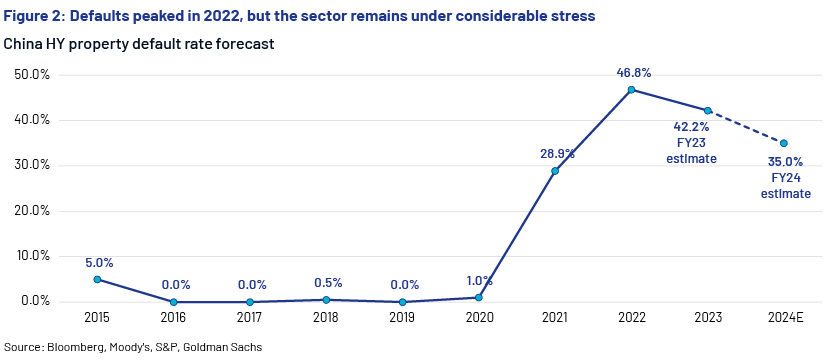

Three hundred and thirty-one offshore bonds were defaulted on in 2020-23, of which c.87% were from the real estate sector. Although default rates of China’s high-yield (HY) real estate sector improved in 2023, they were still significantly higher than in the past and are expected to remain elevated in 2024.

In terms of recovery, dispute resolution is faster for real estate players than for non-real-estate players, especially if resolved out of court. Investors prefer out-of-court settlements; court-directed settlements are generally the last resort, and cash recovery is much lower (2.8%) than with out-of-court settlements (30-35%). In a recent ruling by a Hong Kong court, China Evergrande, one of China’s largest real estate players, was ordered into liquidation, as creditors could not arrive at a resolution out of court. Company bonds are trading at USc2.

Policy response

Unlike in previous instances, the government is now taking measured steps to ensure that the crisis is contained without further inflating the real estate bubble. In the most recent policy response, the government identified 50 real estate developers that would be provided liquidity for delivering ongoing projects. Most of the rescue efforts are focused on tier 1 cities, where oversupply is less severe.

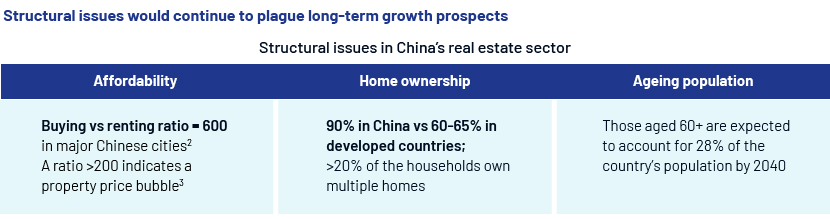

Given the structural issues and years of speculative buying, especially in tier 3 and tier 4 cities, the market is likely to experience a slow L-shaped recovery over the next few years. The recent policy response would favour state-owned entities given their easier access to relief measures from government policies and their presence in tier 1 markets. The sector’s credit profile remains fragile; as such, policy measures would be a key driver in determining credit events over the near term. Investors would need to keep a close watch on policy measures, as these would widen the gap between the strong and weak players.

How Acuity Knowledge Partners can help

Global organisations and research houses leverage our sector- and region-specific expertise to make strategic decisions. Our team of seasoned real estate credit analysts, based in China, India and Sri Lanka, supports institutional asset managers, alternate investment managers and hedge funds by conducting bottom-up and top-down fundamental credit assessments. Our delivery centre in Beijing provides clients with multiple advantages such as a ready research centre with on-the-ground expertise and local-language support.

Sources:

-

[1] China-Britain Business Council

-

[2] As of June 2022, according to real estate data firm Zhuge Zhaofang

-

[3] According to state think-tank the Chinese Academy of Social Sciences

What's your view?

Thank you for sharing your Comments

Share this on

About the Authors

Jeetendra Prakash has close to 15 years of work experience in investment research, with a focus on oil and gas and real estate. He currently supports a large US-based hedge fund. The process involves credit research of high-yield and investment grade credits for different strategies. In addition, he is also actively involved in training and quality control of deliverables. He holds an MBA and is also a CFA charter holder.

Mohit Choudhary has over 7 years of experience in investment research with a focus on real estate, cable and media sectors. He has cleared CFA level 3 exam and is a bachelor of commerce.

Blog

Blog

The US Public Finance Department’s national de....

Introduction The US faces a significant challenge in managing national debt, which has be....Read More

Blog

Blog

Is a US debt default impending?....

The US accounted for 25% of global GDP in 2022, but its debt-to-GDP ratio was at 122%. It ....Read More

Blog

Blog

Russia-Ukraine war: ramifications for Russia

On 21 February 2022, Russian President Vladimir Putin recognised Donetsk and Luhansk, the ....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox