Published on September 30, 2021 by Alankar Ranade, CFA

Key takeaways

-

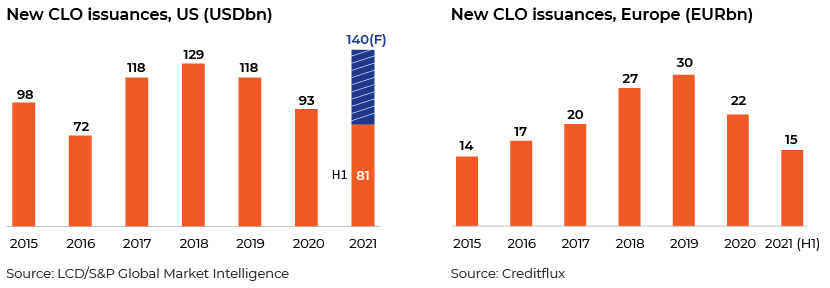

The collateralised loan obligation (CLO) market grew significantly to over USD1tn on the back of record new issuances of over USD100bn in 1H21.

-

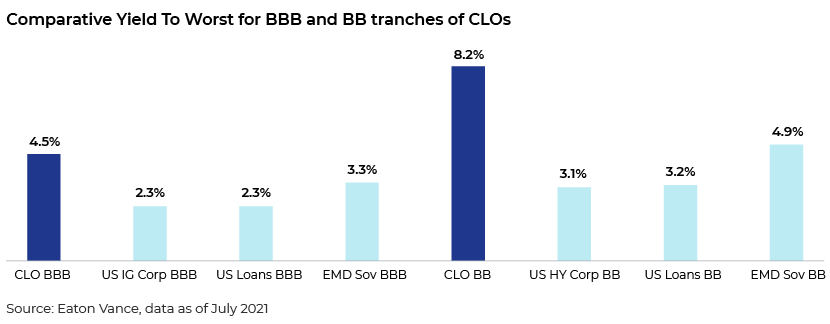

CLOs offer meaningful benefits, both on the upside, through notable yield pick-up (200bps for BBBs), and downside, with considerably lower defaults (2%, compared with the high-yield [HY] default rate of c.4%).

-

However, CLOs could experience some volatility in the coming months from the LIBOR transition, weakening covenants and volatile economic recovery.

-

Acuity Knowledge Partners has been providing end-to-end scalable and customised solutions to CLO asset managers for nearly 15 years. This, coupled with our proprietary LIBOR transition solution, helps asset managers with their overall investment decisions and risk assessment.

CLO issuances hit a record high in 1H21

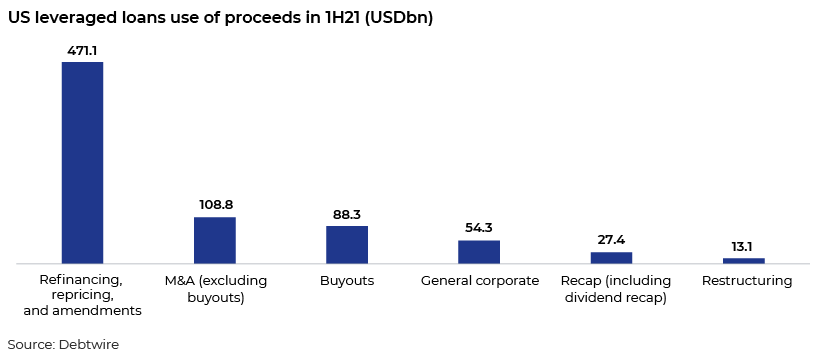

The global CLO market recently hit the landmark of USD1tn in outstanding loans on the back of a sharp recovery in issuances in the US and Europe. US CLO new issuances in 1H21 stood at USD81bn – more than double that in 1H20 – and have accelerated through the period, with 2Q21 issuances at USD44bn. Momentum has remained strong in 3Q21, with c.USD30bn of issuances until 23 August 2021. Strong demand, with improving macro fundamentals, resulted in AAA spreads tightening to 110bps compared with above 200bps last year. S&P Global now expects new issuances of USD140bn for 2021 (against an earlier estimate of USD120bn). Most issuances this year have been from issuers looking to benefit from increased market liquidity and lower yields, with refinancing deals making up more than 60% of the leveraged loans issuance volumes in 1H21.

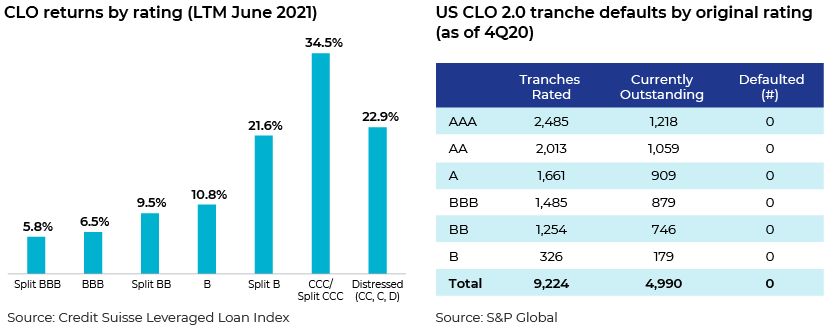

Given the significant turbulence in 2020, excess returns in CLOs were relatively low at 2-3% across rating levels, against excess returns of 10% in 2019. However, 2021 has so far seen a complete turnaround, with returns for the last 12 months (LTM) ending June 2021 ranging from c.6% for the BBB rated category to the highest at 34.5% for the CCC category. In 2Q21, total returns on BB rated CLOs were 4.44% – higher than similarly rated bonds and loans.

Reopening of businesses and the subsequent improvement in corporate earnings have been the main drivers behind these high returns. EBITDA of public companies in the S&P/LTSA leveraged-loan index rose 21% y/y in 1H21.This resulted in the leverage ratio improving to 4.9x – the lowest since June 2019. Improving credit fundamentals have resulted in rating agencies now expecting the default rate for HY companies to fall to 2.5% by June 2022 (compared with an estimate of 6.3% in March 2021).

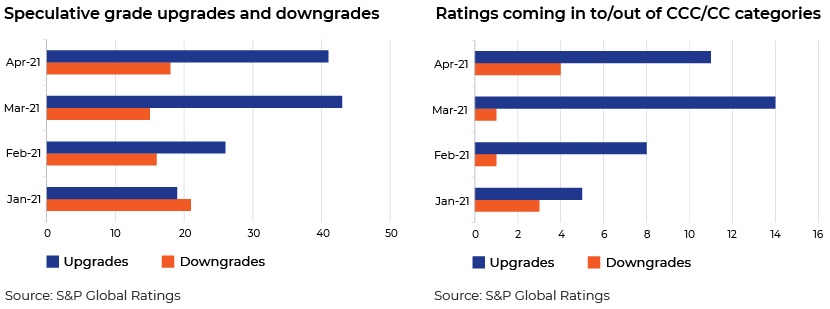

Improving credit fundamentals have also resulted in rating upgrades, with the upgrade/downgrade ratio improving steadily since 3Q20. This momentum has continued in 2021, with upgrades far outpacing downgrades since February and far more issuers upgrading out of the CCC category than downgrading into it.

Structural benefits of CLOs

Other benefits that CLOs bring to asset managers are collateral protection, sector/issuer diversification and higher levels of subordination. Additionally, the minimum overcollateralisation level of CLOs improves the safety net, resulting in a higher recovery rate for investors. Data from Moody’s indicates that the average recovery rate for HY loans stands at 70% against an average recovery rate of c.45% for HY bonds.

Time for caution, after a period of exuberance

A number of institutions expect CLO issuances to hit record levels this year; however, there are three major risks over the near term:

-

Weakening covenants: Moody’s loan covenant quality indicator for North America was 4.47 (on a scale of 5) compared with the five-year average of 4.00, indicating that the quality of covenants has weakened. Furthermore, the share of covenant-lite loans was 90% – the highest level ever.

-

Rating downgrade shock: Given the recent spate of upgrades, credit risk has now shifted to higher rating categories. S&P notes that B- loans accounted for 27% of the HY-rated universe as of 1H21 (compared with less than 5% as of 2Q20). This indicates rating migration from the CCC category as well as new B- credits. A wave of downgrades in 1H20 hit CLO managers, causing some portfolios to breach limits on low-rated holdings.

-

LIBOR transition: Record CLO issuance reflects, in part, a rush to close deals before LIBOR expiration at the end of 2021. Some CLO documents lack language covering the shift to a new benchmark rate, which could spark disruptions in 2022.

Acuity Knowledge Partners’ unique experience in supporting asset managers

Growing interest in the CLO market has brought many new investors and portfolio managers into the space. With the large volume of leveraged-loan issuances, investable assets for portfolio managers have grown considerably. Additionally, the still-volatile economic environment and uncertainty relating to fresh lockdowns and business interruptions remain overhangs on issuers’ credit profiles. Disruptions in the LIBOR transition and fallback language could also emerge as a potential black swan for asset managers.

Acuity Knowledge Partners has been providing CLO managers and investors with end-to-end support for over 15 years, including warehousing, constituent analysis, sector reviews, covenant monitoring and testing, over collateralization testing and portfolio construction and monitoring.

Furthermore, our latest LIBOR transition solutions, which include detailed indenture review and analysis of fallback language, help asset managers understand how prepared issuers are for LIBOR transition. More details on our LIBOR transition solutions can be accessed here.

Tags:

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Alankar has 15 years of experience in investment research and has been supporting high-yield analysts (buy side and sell side) and credit rating analysts for a number of years. He currently supports sell-side analysts of a major trade desk, covering high-yield issuers in EMEA. Alankar holds an MBA in Finance and a bachelor’s degree in Engineering.

Blog

Blog

Interest Rate Divergence in 2024: A Global Conte....

Interest rates are diverging sharply in major economies, most notably in the US and the Eu....Read More

Blog

Blog

Drowning hopes of lower Treasury yields amid the....

The US Treasury market is in a precarious situation as dwindling demand from traditi....Read More

Blog

Blog

Is a US debt default impending?....

The US accounted for 25% of global GDP in 2022, but its debt-to-GDP ratio was at 122%. It ....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox