Published on April 28, 2020 by

Global leveraged lending has almost doubled to c.USD1.4tn (the value of loans in indices used to track the performance of leveraged loans) since the financial crisis of 2008, with the US accounting for c.USD1.2tn. However, the actual size could be c.USD2.2tn, according to the Bank of England (BoE), taking into account smaller non-liquid loans and bank facilities.

Source: Forbes.com

Most borrowers (rated B and below by S&P) pose risk of credit deterioration, as they are susceptible to economic downturns due to inherent systemic risks and weakening credit quality. Lenders, in a bid to capture market share, are also resorting to covenant-lite financing (making up over 80% of the total leveraged loan market), with risks to both lender and investor interests.

A primer on covenant-lite financing

Covenant-lite loans are loans with limited restrictions on borrowers. They are not associated with maintenance covenants (which include leverage and fixed-charge cover ratios a borrower has to adhere to; these ratios also indicate non-compliance with covenants). Conversely, such loans have incurrence covenants that are tested only on the occurrence of a specific action or event.

Lenders do not have the flexibility to increase interest, charge more fees or accelerate debt payments in such underwriting until the debt matures. Borrowers, on the other hand, enjoy the ability to liquidate assets and use the proceeds for working capital purposes instead of accelerating debt repayment.

Loan documents allow for subjective add-backs to EBITDA, such as estimated cost savings and acquisition synergies that artificially inflate actual EBITDA. Such adjusted EBITDA is used by borrowers to manipulate loan terms with respect to restricted payments, asset transfer/sale and incurring additional debt.

In a nutshell, covenant-lite financing provides borrowers with weak credit requirements so they can adjust their financials to obtain incremental financing (refinancing) and mask default metrics, putting both the lender and the investor at risk.

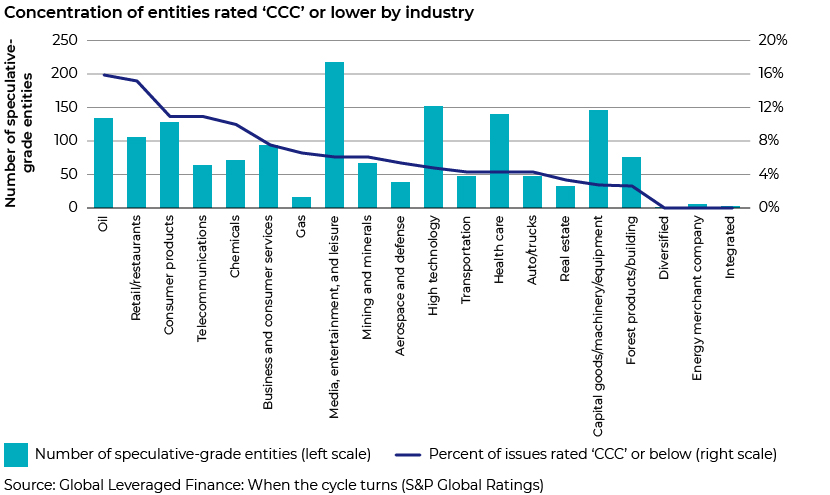

Sector snapshot

Source: Global Leveraged Finance: When the cycle turns (S&P Global Ratings)

Companies in the oil, consumer goods, airlines, high-tech, capital goods, healthcare, restaurant, media and entertainment sectors account for more than 50% of the borrowers rated CCC or below.

Recent volatility in crude oil prices and the COVID-19 outbreak have led to a sharp fall in demand for crude oil from China, the largest oil consumer globally. China’s contribution to global growth cannot be undermined, and the current global lockdowns could have a contagion effect on the sectors that depend on China’s exports. In addition, non-investment-grade companies rated B and below are more likely to opt for debt restructuring based on their weak financial metrics in the coming months.

CLOs, default rates and liquidity

Banks and non-banks sell leveraged loans to special-purpose vehicles (SPVs) that package them as fixed income products called collateralised loan obligations (CLOs). Almost a third of all leveraged loans are in the form of CLOs, with the US accounting for new CLO issuance of USD125bn in 2018 and USD135bn in 2019. Global CLOs amount to c.USD615bn, far more than products such as auto loans (USD223bn), student loans (USD170bn), and credit cards (USD124bn).

Banks subscribe to nearly 50% of CLO issuance, with the remainder subscribed to by asset managers, insurance companies, hedge funds and structured credit funds that are interconnected with banks, as borrowers are counterparties with banks for derivative transactions. A downturn in leveraged lending could lead to liquidity issues for such firms.

The default rate for leveraged loans was 1.9% at end-2019, below the historical high of 4.5% in 2014. This is forecast to edge upwards (2.0-2.5%) due to the headwinds faced by most non-investment-grade issuers.

The oil price shock and COVID-19-related lockdowns will negatively impact cash flow of non-investment-grade companies and may raise default rates above 10% in the US and close to high single digits in Europe over the next 12 months.

The number of leveraged loan mutual funds (MFs) and exchange-traded funds (ETFs) has more than tripled in the past decade. Although such MFs and ETFs allow for immediate redemption, the underlying leveraged loans are traded less frequently, and in an economic downturn, there could be a liquidity mismatch that banks may not be able to bridge.

Attractive yields have been driving significant growth in the leveraged lending space in the past decade. Default rates on CLOs are near zero at present, and the size of the leveraged lending market is manageable relative to other fixed income securities markets.

We believe banks are now in a much better position to cushion themselves against shocks given the various regulatory best practices in place after the 2008 financial crisis. However, the shadow banking framework could pose a threat given the systemic risks it is exposed to and the lax underwriting standards it adopts to gain market position. In addition, the negative impact of COVID-19 on the global economy as a whole and non-investment-grade companies in particular will likely be better analysed in the second half of 2020, when the virus is expected to have peaked worldwide.

The Commercial Lending teams at Acuity Knowledge Partners provide invaluable offshore support to banks, assisting with prudent underwriting of loans to large corporate, mid-corporate and SME customers. Our credit managers in the Leveraged Lending teams provide granular insight at the macro level and help banks’ credit risk teams identify potential risks in lending by rigorously analysing companies’ credit quality and each loan agreement’s structure.

Sources:

What's your view?

Thank you for sharing your Comments

Share this on

Blog

Blog

China’s imports of Japanese food products decl....

Background China has consistently been one of Japan's most important trading partners: Ja....Read More

Blog

Blog

New Trends and Opportunities in SME Lending....

SMEs are generally defined based on parameters such as annual sales, number of employees, ....Read More

Blog

Blog

The mystery of black swans and how to prepare fo....

In the realm of global financial markets, there exist fascinating phenomena known as “bl....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox