Published on December 29, 2022 by Sanchit Tuli

The race to remake healthcare – Giant firms are entering the healthtech space to mark the shift from a “fee for service” (FSS)-based model to a “value-based model”

Value-based healthcare is increasing in scope and popularity. The transition to this model would see a downturn in terms of finances in the short term before longer-term cost savings are realised. This model is transforming the way healthcare specialists and hospitals provide care.

The value-based model uses a team-oriented, diversified-network approach with sophisticated technology such as enterprise resource management databases that help with care management. This involves maintaining a central repository of patient information so that care is well coordinated. With the adoption of healthcare technology such as electronic health records, an integrated database can be created so the outcome could be monitored in real time.

Emerging companies such as Bright Health, Ally Align Health, Vitality Health, AMC Health and Troy Medicine are contributing significantly by offering value-based healthcare delivery.

The sector is also seeing consolidation; large non-healthcare companies such as Amazon and Oracle are to partner with healthcare startups to offer solutions to the niche market. Using advanced technology to provide telehealth or virtual care assistance is vital for delivering services in optimum time under this value-based service model.

Healthtech startups revving up the market

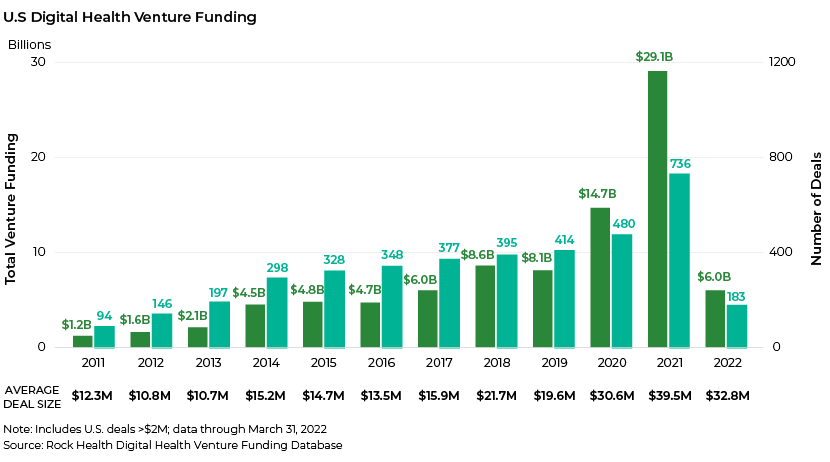

As the healthcare crisis deepened during the pandemic, healthtech companies gained prominence, with their niche offerings providing a robust digital platform to support patient engagement. As investor confidence increased, the number of initial public offerings of healthtech firms skyrocketed in 2021. Total funding for US-based digital health startups amounted to USD29.1bn across 729 deals, with an average deal size of USD39.9m, almost doubled that of USD14.9m in 2020.

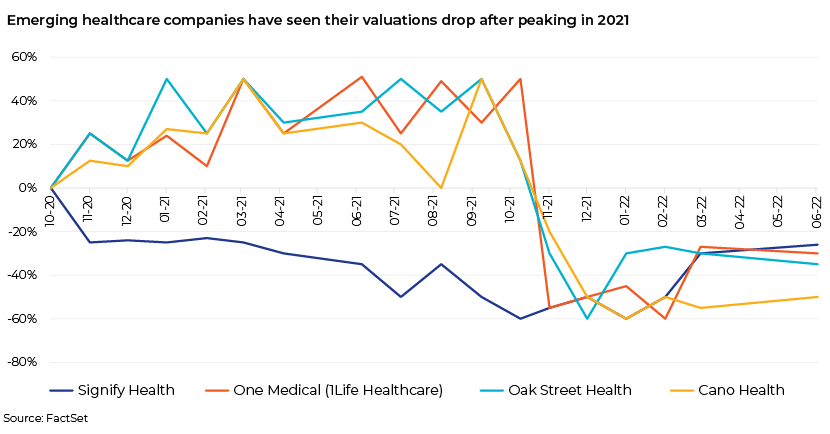

Valuations of companies such as Signify Health, One Medical (1Life Healthcare), Oak Street Health and Cano Health with well-established and structured telehealth and hybrid care offerings peaked in 2021, mainly due to their shifting their operating models from “fee for service” (FFS) to value-based care.

For example, Oak Street Health is a tech-enabled, value-based primary-care startup specifically targeting Medicare-eligible patients. The company went public, with USD328m of proceeds from its initial public offering, with its valuation based on its technology-driven services priced under a value-based primary-care service model.

Healthtech offerings have attracted investors and Venture capitalists to invest heavily in the sector, expecting to capture a large share of this yet untapped market and make a profitable exit subsequently.

Funding scenario for healthtech firms

However, these companies’ funds have dried up on fears of recession, and funding for healthtech companies has tanked sharply, to USD6.0bn (-79.4%) from USD29.1bn in 2021. Venture capitalists who were bullish in 2021 are now withdrawing their investment funds, looking to reduce their exposure to the market, and shifting to safe-haven assets, reflecting high market volatility and low investor confidence. This has forced startups to try alternative routes such as crowdfunding and debt-financing, which are not appealing and are not sustainable in the long term. The increase in borrowing costs limits the profitability of startups, with fewer entities reaching maturity.

Trends that have caused venture capitalists to withdraw their investments are as follows:

-

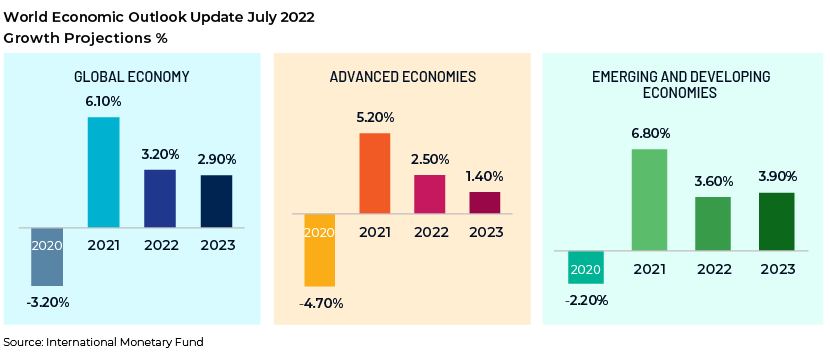

Decline in growth projections – Projections as of July 2022 are for GDP growth to decline from 6.1% to 3.2% in 2022 and to 2.9% in 2023.

-

Bearish stock markets – The stock markets are under pressure, with economic uncertainty peaking in the first half of 2022 and remaining high, bearing the brunt of Federal Reserve policy tightening, shrinking market liquidity and slower economic growth. The S&P 500 was down 9.34% as of September 2022, bringing its YTD return to -24.77%; the Dow Jones Industrial Average lost 8.84% for the month and was down 20.95% YTD; the S&P Mid Cap 400 fell 9.36% for the month, declining 16.55% YTD; and the S&P SmallCap 600 was down 10.05% with a YTD return of ‑24.02%.

-

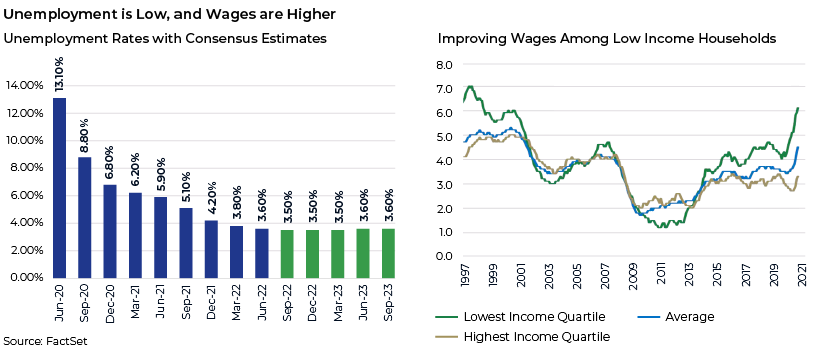

High inflation and low unemployment – The Phillips curve theory states that when inflation is high, unemployment is low and vice versa. The trend of low unemployment seems positive for the economy, but if unemployment is too low, it would drive Inflation higher. Low unemployment is extremely sensitive to government interventions to curb inflation, which could trigger a recession if not balanced.

-

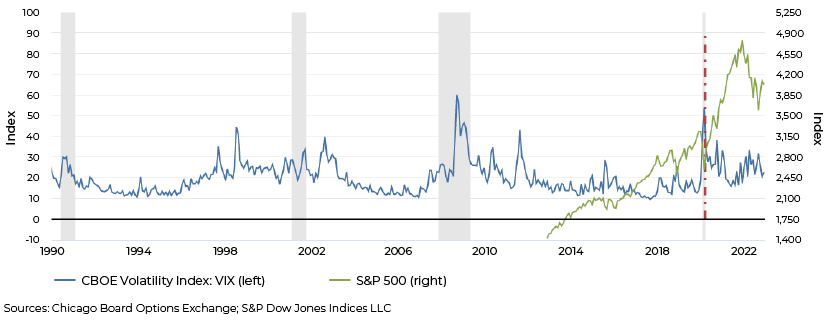

Volatility index vs equity index, trends – There is a negative relationship between the VIX and equity markets. This is evidenced from the following graph, which shows the VIX increased from 17.22 (as of December 2021) to 30.0 (as of October 2022) while the S&P declined from 4,766 to 3,744 (-21.44%).

With all metrics indicating highly volatile and uncertain market conditions, investor concern is increasing, leading to investors withdrawing investments from the healthtech segment.

Giant firms to play smart rather than safe

Despite the healthcare sector being considered a slow-growth sector and excruciatingly slow to adopt new-age technology and unconventional models, it presents a significant opportunity if one is not distracted by the short-term economic uncertainty and volatility.

Demographics make healthcare too big a sector to ignore

Given that global life expectancy is currently c.73 years due to improvements in care and the quality of living, all countries are likely to see an increased proportion of the elderly in the population mix. WHO reports that by 2030, one of six people in the world will be 60 years of age or older, with the share of the population aged 60 and older increasing to 1.4bn from 1bn in 2020 and doubling to c.2.1bn by 2050. Also, by 2050, 80% of the world’s population over 60 years of age is expected to be in low- and middle-income countries.

This trend of ageing populations is expected to include the higher risk of age-related diseases – diabetes, neurodegeneration and fatal diseases such as cancer. This further bolsters the need for preventive medicine. A robust new-age healthtech structure is the need of the hour, supplementing the current strained healthcare system.

Juggernauts enter the race to remake healthcare

Despite the fair share of failed attempts to undertake remaking the sector, global juggernauts such as Amazon have entered the race again. Amazon’s previous attempt with its in-house telehealth business – Amazon Care – did not function as planned; this partnership with Berkshire Hathaway and JPMorgan Chase was wound up after three years, highlighting the difficulty in transforming the sector. Amazon’s plans to re-enter it is evidence of the large opportunity available. Walmart, Walgreens, tech giant Oracle and insurance giant UnitedHealthcare have also entered the race.

These global giants have not shied away from investing amid the cyclicality and uncertainty in the market; they have perceived it as a buying opportunity and have followed inorganic, aggressive strategies to enter the sector by acquiring healthtech firms, albeit at cheaper valuations.

The following deals mark the start of the race to transform the healthcare sector:

-

20 December 2021: Oracle announces acquisition of Cerner, a leading provider of digital information systems used in hospitals and health centres, for c.USD28.3bn in equity value. Together, Cerner and Oracle are to focus on the ability of the interfaces to reduce time medical providers spend in dealing with systems and increase the time they spend directly providing treatment or care for patients.

-

21 July 2022: Amazon agrees to pay USD3.9bn for One Medical, a primary-care concierge service, which ensures Amazon a market share in the healthcare sector. Amazon intends to enter the direct-primary-care business and sell more healthcare products with the help of its pharmacy business that started with the acquisition of Pill Pack for c.USD1bn in 2018.

-

31 August 2022: Walgreens Boots Alliance completes majority-share acquisition of CareCentrix. The partnership with CareCentrix intends to extend care capabilities to homes to create a connected and congenial ecosystem for patients. The company has finalised the investment as rival firms including CVS Health, Amazon and Optum Care express interest in buying Signify Health. Walgreens’s rivals such as CVS Health, Amazon and Walmart are retailers ramping up to add more primary-care and in-home services.

-

5 September 2022: CVS Health announces acquisition of Signify Health for USD8bn. The acquisition will help CVS enhance its on-door medical assistance.

-

7 September 2022: United Health Group and Walmart announce their collaboration to deliver high-quality, affordable healthcare powered by the “Optum” clinical capability. United Health Care, through its medical provider arm Optum Care, has been buying multi-specialty physician practices focused on providing tech-enabled medical assistance. Other flagship acquisitions by United Health Care’s Optum include the acquisition of home healthcare business LHC Group (USD5.4bn) to introduce mobile health clinics, Refresh Mental Health (for an undisclosed amount), Kelsey-Seybold Clinic and Atrius Health.

Outlook

The healthcare sector is expected to see a significant transformation in terms of delivering comfort in addition to medical services, focusing on long-term clinical outcomes and providing more value to patients rather than on short-term volume-driven output, marking the most awaited change from the FFS model to a value-based model. The shift would start from changes in the primary healthcare segment, with a cascading effect on other segments.

The common factor between large global firms such as CVS-Aetna, Walmart, Walgreens, Amazon and UHG-Optum is that they have observed the upcoming trend of direct delivery of medical services, even outside of conventional medical setups. CVS-Aetna, for instance, has started with mini-clinics, employing nurses and pharmacists in retail facilities to administer injections, treat basic medical problems such as colds, and sinus and urinary tract infections, and provide general care. Some venture capital-backed firms have created new models where the financial risk of the cost and quality of medical treatment is borne by the provider, corresponding to an upfront, annual payment, also referred to as “capitation”. These kinds of medical providers are a win-win for all stakeholders, as they calculate and limit waste in the system, build savings and improve working conditions for medical providers while creating a profitable business proposition for investors.

Private entities strive to revive the healthcare sector with the following strategies:

-

Retailers are looking to initiate healthcare service delivery with general medical practice or primary healthcare. To gain customer traction, they are willing to incur losses in the short run, strategically using profits to cross-subsidise their care offerings. They will use primary healthcare as a marketing tool to capture market share and subsequently launch offerings that include the full range of healthcare services.

-

Companies such as UHG-Optum and CVS-Aetna are examples of companies adopting “capitation”, the most-promising concept currently. They assume the financial risk of the cost of care on behalf of fully insured clients and manage expenses for self-insured clients. The concept of capitation reduces costs, enhances quality by maximising incentives on preventive healthcare and effectively monitors chronic conditions to avoid unnecessary hospitalisation. The model minimises the need for expensive specialty care, when a patient could be treated with other inexpensive substitutes or primary care. This cost reduction enables insurers to offer attractive premiums while increasing their retained earnings. This increase in income increases compensation of healthcare providers, unlike under the FFS structure.

This analysis indicates this is the best time for increased investment and support from private firms, venture capitalists and other businesses to transform the healthcare sector and create long-term value for patients without the strain of a financial burden. It is estimated that up to USD265bn worth of care services for Medicare FFS and Medicare advantage beneficiaries could shift to home care by 2025, without a reduction in quality or access. Medical healthcare services would then be just a click away, just as Amazon visualised.

How Acuity Knowledge Partners can help

We are a leading provider of high-value research, analytics and business intelligence. We help corporate clients from diverse sectors understand strategy; we understand the operational concerns and challenges they face, and assist them with decision making.

We offer customised solutions including market and competitive intelligence, benchmarking and analysis, strategy research, due diligence and industry analysis. We provide venture capital and private equity (PE) firms with comprehensive solutions across the investment cycle and help them stay abreast of industry dynamics and trends in consumer behaviour, economics and demographics in both current and new markets. We also offer horizontal support across middle-office and back-office operations to PE firms on the investment side; our services range from portfolio management and advisory to deal finding and target selection.

Sources:

-

https://www.wsj.com/articles/dr-amazon-will-see-you-now-11662715810

-

https://hbr.org/2022/01/can-new-players-revive-u-s-primary-care

-

https://rockhealth.com/insights/q3-2022-digital-health-funding-the-market-isnt-the-same-as

-

https://www.lordabbett.com/en-us/financial-advisor/insights/markets-and-economy/recession-

-

https://www.who.int/news-room/fact-sheets/detail/ageing-and-health\

-

https://www.un.org/en/desa/covid-19-slash-global-economic-output-85-trillion-over-next-two

-

https://www.ibm.com/downloads/cas/N2NNWYXG#:~:text=The%20concept%20of%20value%2

-

https://www.oracle.com/news/announcement/oracle-completes-acquisition-of-cerner-2022/

-

https://press.aboutamazon.com/news-releases/news-release-details/amazon-and-one-medical

-

https://www.walgreensbootsalliance.com/news-media/press-releases/2022/walgreens-boots

-

https://www.cvshealth.com/news-and-insights/press-releases/cvs-health-to-acquire-signify

-

https://www.unitedhealthgroup.com/newsroom/2022/2022-9-7-wal-mart-collaborate

-

https://news.bloomberglaw.com/health-law-and-business/insight-the-healthcare-industrys-shift

-

https://www.forbes.com/sites/simonmoore/2022/06/24/multiple-signals-now-point-to-us

-

https://www.forbes.com/sites/brucejapsen/2022/08/31/walgreens-finalizes-carecentrix-home

-

https://www.imf.org/en/Publications/WEO/Issues/2021/03/23/world-economic-outlook-apri

-

https://www.delveinsight.com/blog/value-based-healthcare-model#Future_Impact

Tags:

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Sanchit Tuli joined Acuity Knowledge Partners’ (Acuity’s) Investment Banking team with over three years of experience. He specialises in the healthcare and consumer sectors. He currently supports the US division of a leading European bank, having demonstrated proficiency in financial statement analysis and preparing credit reports and pitch decks. Sanchit holds a Bachelor’s degree in Business Administration from Christ University, Bengaluru.

Blog

Blog

Independent research firms must scale up to gain....

Executive summary Independent research firms play a vital role in the investment researc....Read More

Blog

Blog

Sustainable finance – regulations and trends 2....

Introduction Sustainable finance has become a critical theme internationally to pave th....Read More

Blog

Blog

Understanding economic efficiency – the imp

The incremental capital output ratio (ICOR) emerged as a result of the Harrod-Domar growth....Read More

Blog

Blog

Transitioning to sustainable fashion mitigate

Fast fashion’s rapid production and consumption cycle has a detrimental impact on the en....Read More

Blog

Blog

Part 1 – Transition from Fee-for Service ba

The race to remake healthcare – Giant firms are entering the healthtech space to mark th....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox