Published on May 10, 2018 by Anandita Ray

The number of participants in the financial services ecosystem has multiplied in recent years, expanding beyond their niche and offering additional services to maintain market competitiveness. Previously defined sectorial boundaries are gradually blurring; for example, digital giants such as Amazon and Tencent were pioneers in their field, but others are now closely following their path, making the system indistinct.

Traditional banking models are falling apart and digital/non-bank players are increasingly foraying into the space. India’s financial services landscape is an example of how the banking industry has been disrupted by the emergence of several payments banks – once small-scale mobile wallet providers.

Alibaba-backed Paytm has c. 215 million subscribers versus the largest state-owned bank State Bank of India’s 207 million

Launched in September 2017, Google’s payments app Tez processes c. 75 million digital transactions a month; this is the same number of transactions handled by Axis Bank, the country’s fourth-largest bank

Similarly, in the UK, the rise of challenger banks is revolutionizing the banking system. While incumbent banks are stumbling on legacy issues, new digital-only banks are outperforming the big five on growth, cost to income and return on equity.

Are incumbents poised for advantage in the current scenario?

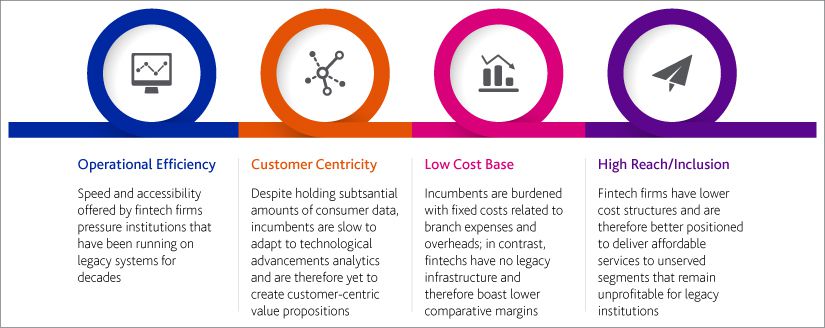

Traditional banks have vast customer bases and rich capital structures but are restricted from growth by remediation costs and legacy systems.

New technology providers are increasingly eroding market share of traditional banks for the following reasons:

The road ahead

The future will likely thrive on an open eco-system with a number of different players (both financial and non-financial), working together to create value for customers

Incumbent institutions are likely to employ parallel strategies. While they will compete directly with new entrants, they are well positioned to leverage their own legacy assets to provide those same new entrants with infrastructure and access to services

Preserving market share will require not only re-imagining technology implementation in core business operations, but also re-working on customer experience

While incumbents brace themselves to weather these changes, it has yet to be seen whether they would be able to match the level of personalization, speed, and convenience offered by the likes of Google, Amazon, and Alibaba.

Acuity Knowledge Partners is experienced in helping big financial institutions enhance their business practices. We have dedicated teams of highly qualified analysts (holding MBA’s, CFAs and CAs) that support clients in strategy research assignments, including market attractiveness assessments, competitor strategy analyses, peer benchmarking, target identification and evaluation, and financial modelling. Further, our Business Excellence and Automation Tools are designed to empower the financial services ecosystem and enables traditional firms to stay ahead of the curve.

Sources:

https://institute.fintechcircle.com/

https://www.bai.org/banking-strategies/

https://economictimes.indiatimes.com/

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Anandita Ray has over 7 years of experience in the research and consulting industry. She currently works in the Strategy Research and Consulting practice at Acuity Knowledge Partners and supports clients in the payments and remittance industry with assignments related to growth strategy formulation, go-to-market strategy, market entry and expansion, and competitor analysis and benchmarking. Anandita holds B.Com (Hons.) from Calcutta University and Masters in Finance from Amity University.

Blog

Blog

Advantages of having a remote executive assistan....

“They’re troubleshooters, translators, help desk attendants, diplomats, human database....Read More

Blog

Blog

Technology a catalyst for future deals....

Technological advancements have made past ways of transacting obsolete. Trends are changin....Read More

Blog

Blog

Top technology trends in financial services 2

The 21st century has been marked by rapid digital penetration, evolving consumer preferenc....Read More

Blog

Blog

The Third-mile Challenge in Remittances: Can

The role of remittances in economic development, especially in developing nations, cannot ....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox