Published on September 18, 2020 by Nikhil Francis and Saswata Mohanty

U.S. Municipal market activity was at the rock bottom level due to Covid-19 during March but started showing the sign of recovery after Fed’s intervention which was evident in the market in following months and continues to stabilize. This helps in boosting the confidence among the players in the municipal market.

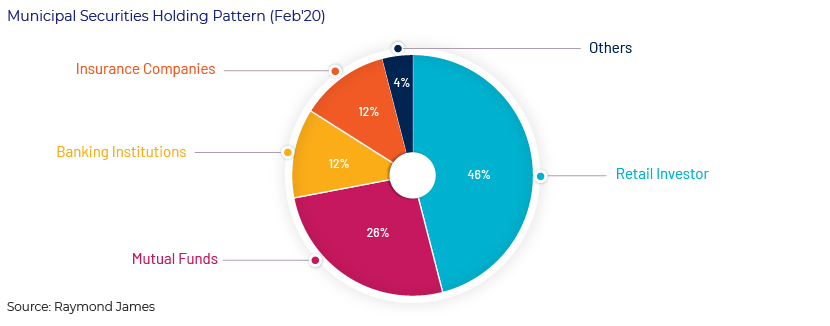

Short Look at the Municipal Securities Holding Structure

The size of municipal bond market was $3.9 trillion during 2019. Retail investor takes the lion share in holding the municipal securities, followed by mutual funds. The remaining 28% of the muni market includes banking institutions at 13%, insurance companies at 12%, and other at 3%.

State and local governments primarily depend on municipal market to execute infrastructure projects including road construction, airports, water and waste water treatment, school buildings, as well as to minimize the short-run imbalances between receipts and payments. Approximately 75% of the infrastructure projects in the U.S. are funded by municipal bonds.

Impact pounding on Municipal Market Due to the Covid-19

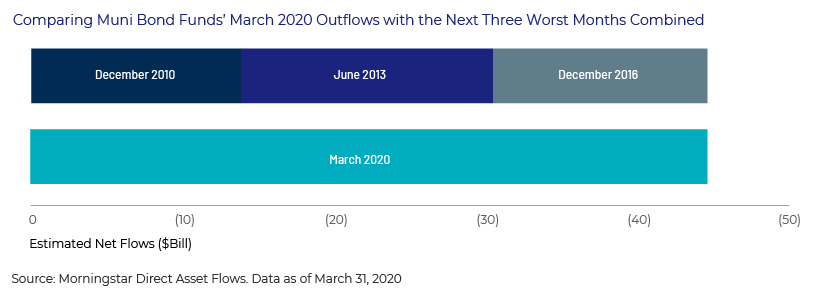

Selling pressure from Investors tumble the market activity leading to low level of issuance

Municipal Bonds is considered a relatively safe investment as the probability of default is generally very low. Over the past few months, overall market sentiment has remained watchful and investors started focusing more on the fundamentals of the issuer owing to the economic slowdown due to of the COVID-19 pandemic. Given the tumble in the financial markets, investors believe to hold onto the liquidity position rather than buying new municipal bonds. This lead to selling of the investors’ holdings in bonds or mutual funds and stopped buying any new issues, the selling pressure on municipal bond peaked during March 2020. For the week ending on March 18th, investors pulled money from the market to the tune of $12 billion, almost 2.5% of assets – and another $13.7 billion in the succeeding week. Between March 9 – 20th, state and local governments managed to sell only $6 billion out of the $16 billion of bonds earmarked for the issue.

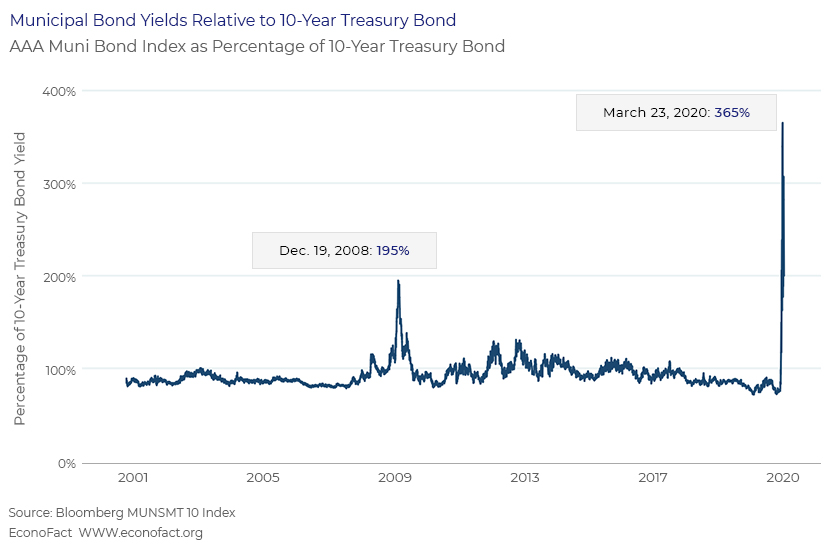

The lower level of demand resulting in higher Municipal-to-Treasury yield ratio, exceeded even the worst hit during 2008 crisis

As per the the exhibits the ratio between 10 year AAA-rated municipal bonds to 10 year treasury bond yield generally been observed less than 100% because the interest on municipal bonds is tax-exempt so these bonds offer a lower pre-tax interest rate than Treasury bonds. However, the ratio climbed to almost 200% during the financial crisis at the end of 2008. During the mid-March, the market observed similar trend and ratio even exceeded the worst depths in 2008 crisis, which has risen to more than 350%. The high ratio signifies negative return posted by the AAA municipal bonds coupled with falling prices and rising yield.

Infusion of $500 billion Municipal Liquidity Facility (MLF) by Federal Reserve to stablize the Market

In late March Federal Reserve intervened to stabilize the market by creating a $500 billion “Municipal Liquidity Facility” (MLF) to directly purchase state and local debt. Under the new facility the municipal bondholders can use these bonds as collateral for borrowing cash from the Federal Reserve System which helped to an extent to ease the liquidity pressure in the market.

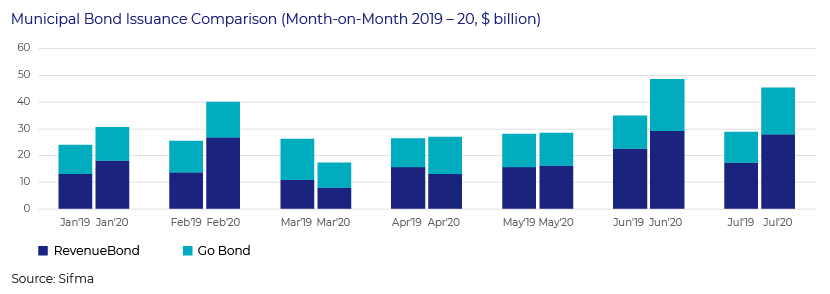

Municipal bond market continued their fall through the month of April, but the losses were squeezed as compared to March. The total municipal bond issuance during April was $23.8 billion, shows the sign of recovery as compared to March’s $19.3 billion, marked the lowest monthly figure since February 2018.

Municipal Bond market started gaining momentum backed by the confidence building measures among the investors by Fed

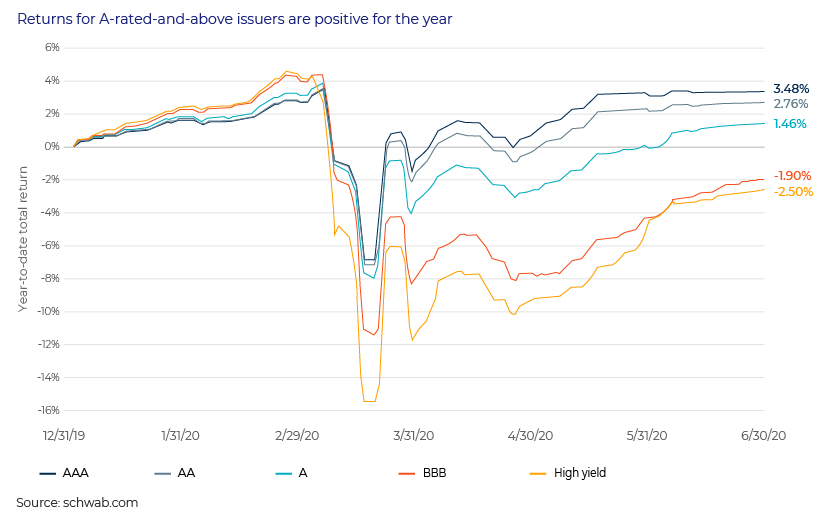

As the investors are more watchful, the high rated bonds posted better return compared to the low rated instruments. While improvement shown from the downward movement from March, municipal bond yields and municipal /Treasury bond ratios remained high relative to pre-pandemic levels. The trend of outflow during March to 1st week of April were momentarily reversed in mid of April, though the month netted approximately $16 billion in outflows.

The month of May saw one of the biggest Municipal Bond market rally with $2.87 billion flowing into municipal funds. The Bloomberg Barclays Municipal Bond Index and the Bloomberg Barclays High Yield Municipal Bond Index posted a return of 3.48% and (2.5%) respectively on a year-to-date basis. The rally was backed by the support from Federal Reserve through the Municipal Lending Facility which was extended through out May and early June. The primary market observed multiple noteworthy deals during this month, with a total new issuance of approximately $23.8 billion.

The new issue in the municipal market continued to improve post March and brought a total of $45.4 billion of supply in July. Year-to-date issuance of $237 billion which is 22% up from the same time last year, primarily driven by the taxable supply which remains approximately 3.0x over last year’s levels while tax-exempt supply is in-line with last year’s levels.

Concluding Thoughts: Municipal market is all set for positive rebound but little cautious

Buyers are cautious in dealing with muni portfolio as Covid-19 impacted differently on different sectors. Water and sewer bonds are performing better compared to other sectors, while hospitals and transportation were the worst hit. In addition, strategists sees some opportunity in education bonds but with watchful approach.

The Federal Reserve intervention through Municipal Liquidity Facility (MLF) has helped in building the confidence among the investors which was well reflected in the Market activity during June and July. In addition, the opening up of the economic activity post lock down is further expected to propel the market activity. Municipal bonds outperformed the U.S. treasury during later part of the 1H’2020 and the demand would further pick up during summer.

Investors primarily focusing on highly rated instruments initially and moving slowly towards high yield muni instruments. Market pundits expecting another round of Fed aid during this summer to further propel the market catalysts.

At Acuity Knowledge Partners, we help investment banking teams scale up their public finance underwriting practices and drive value for their clients. By leveraging dedicated teams of experienced analysts in our offshore delivery centers, clients benefit from operational efficiency and cost optimization. Our team of public finance experts are well versed in covering municipal financing and public sectors and are vested with state-of-the-art modelling capabilities. Many of our clients working with our specialized public finance investment banking teams have benefited from our integrated suite of services along the investment banking advisory value chain.

Sources

https://econofact.org/how-is-the-coronavirus-crisis-affecting-the-municipal-bond-market

http://www.msrb.org/msrb1/pdfs/MSRB-Muni-Facts.pdf

https://www.nuveen.com/en-us/thinking/municipal-bond-investing/municipal-market-update

https://www.blackrock.com/us/individual/insights/municipal-monthly

https://www.rbcwealthmanagement.com/_us/static/documents/insights/file-836257.pdf?v=20200710

http://www.msrb.org/msrb1/pdfs/MSRB-Muni-Facts.pdf

https://www.schwab.com/resource-center/insights/content/2020-mid-year-outlook-municipal-bonds

Tags:

What's your view?

Thank you for sharing your Comments

Share this on

About the Authors

Nikhil Francis has over 2.5 years of experience in Investment Banking domain. Currently, he supports the Public Finance team for a U.S. based mid-market investment bank, with a focus on Municipal Finance and Infrastructure - Public Private Partnership(P3) . He holds Post Graduate Diploma in Financial Management(PGDFM) and Master’s degree in Commerce with specialization in International Business.

Saswata Mohanty has over 13 years of experience working across different value chain in the Investment Banking domain. Currently, supports Public Finance / Project Finance team, with a focus on Municipal Finance and Infrastructure - Public Private Partnership(P3). He is also responsible for quality check and overall functions of Investment Banking team, for a U.S. based mid-market Investment Bank, in Bangalore. Prior to joining Acuity, he was with Verity Knowledge Solution (affiliate of UBS) for close to 6 years. He holds a Master’s degree in Business Administration in Finance.

Blog

Blog

Are Indian equities nearing saturation point?....

The Indian equity market has seen a notable rise in recent years, fuelled by a confluence ....Read More

Blog

Blog

Gamification in Asset Management – A Game-....

Introduction Gamification – the use of game mechanics such as points, challenges, rewar....Read More

Blog

Blog

Emerging markets likely to outperform develop

Emerging markets likely to outperform developed market Emerging markets (EMs) have recove....Read More

Blog

Blog

Changing landscape for technological advancem

Changing landscape for technological advancement Technology has been evolving, and a numb....Read More

Blog

Blog

IPO market building momentum for strong uptur

IPO market: building momentum for a strong upturn The IPO market saw a shift in sentiment....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox