Published on April 12, 2022 by Nishant Mishra

Key takeaways

-

Bans and sanctions on Russia following its invasion of Ukraine would severely cripple and isolate its commercial aviation sector and derail the recovery of Europe’s fragile aviation sector

-

A strong domestic market could save Russian airlines for a while, but the future looks bleak

-

Lessors to Russian airlines are at major risk of mass default on lease payments, unable to get back their jets

-

Western airlines and aircraft manufacturers will likely be partially affected but are likely to find a way to deal with the problem

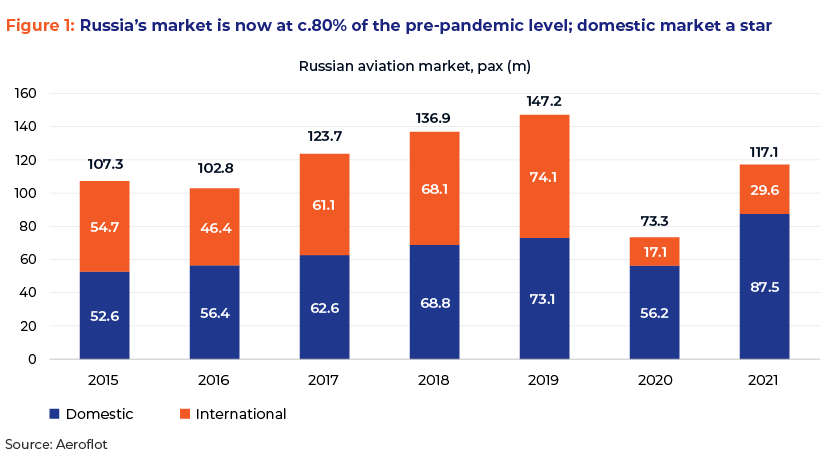

Russian aviation was in the pink of health before the invasion

In 2021, when the global aviation sector was reeling under the pressure of the pandemic, Russia’s aviation market continued to lead the global recovery, despite COVID-19 waves. It was also ranked one of Europe’s top airline markets in 2021 (from #7 in 2019, before the pandemic), mainly due to its robust domestic market. Russia’s total traffic was 20.4% lower in 2021 than pre-pandemic levels, although much better than the global decline in traffic of 58.4% and Europe’s -67.6% (source: IATA). Before the invasion, the markets expected significant growth in Russia’s aviation market in 2022 (traffic was up 47% y/y in January and 28% y/y in February) as the global aviation market, especially European routes, re-opened.

Then came the war, followed by sanctions and bans

Airspace ban.

In response to Russia’s invasion of Ukraine in February 2022, close to 40 countries, including all 27 EU countries, the US, the UK, Canada and Switzerland, shut their airspace to Russian aircraft. Russia retaliated by enforcing similar bans on aircraft belonging to these countries.

Aircraft and spares ban.

All three major aircraft manufacturers, i.e. Boeing, Airbus and Embraer, stopped supplying Russian airlines with planes, spare parts, maintenance and technical support and services. Two-thirds of Russia’s commercial fleet is supplied by these manufacturers (332 Boeing, 305 Airbus aircraft and 23 Embraer); keeping its aircrafts airworthy would, therefore, become a daunting task for Russian airlines.

Online ticket booking ban.

Online booking agents of Russian carriers, Sabre and Amadeus, stopped taking bookings from customers. Moreover, Russian customers can no longer use their Visa, MasterCard or other Western credit cards to book their tickets.

Insurance and reinsurance ban.

The UK government banned Russian aviation and space companies from accessing the services of UK-based insurers and reinsurers directly or indirectly. If the EU or other countries follow this ban, it would paralyse Russian airlines.

Leasing ban.

The EU has mandated all European leasing companies to terminate their links with Russia by 28 March and repossess their leased aircraft from Russian airlines. According to airline intelligence provider ch-aviation, 777 of Russia's 980 passenger planes are on lease, of which 515 planes (worth USD13.0bn) are from foreign aviation firms.

What this means for Russian and international airlines, aircraft manufacturers and lessors

Rating agencies started downgrading Russian transport companies due to their inability to conduct business and service debt. They also downgraded Russia's sovereign ratings to junk (CAA2/CCU/C).

Russian airlines.

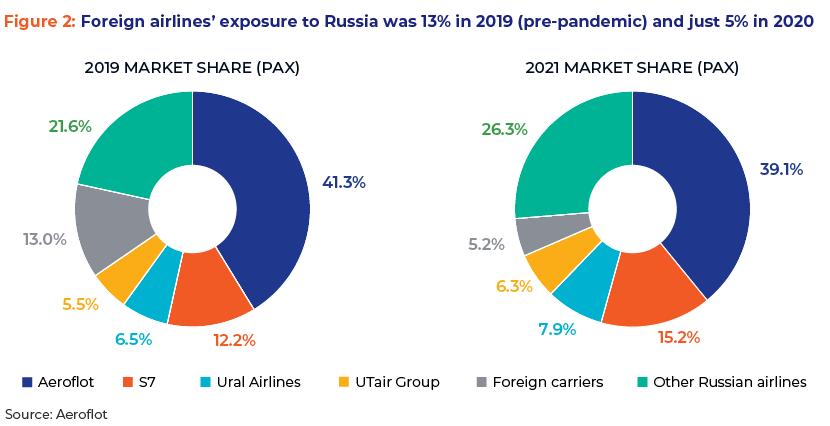

The top four airlines – Aeroflot Group (including Pobeda and Rossiya), S7 Airlines, Ural Airlines and UTair Group – held close to 70% of Russia’s air travel market share in 9M 2021 and would be hit by the airspace ban, as they generate substantial revenue from EU routes. Moreover, the online ticket booking ban would prevent them from selling tickets even for domestic flights. With plane manufacturers announcing a ban on the sale of parts and services, keeping their aircraft airworthy would become a daunting task. In addition, with EU directives for aircraft leasing companies to repossess their planes, the airlines could risk losing their planes if they leave the country.

Western airlines.

The share of international airlines in Russia was 15.2% in 2018 and 13.0% in 2019, but dropped to 5.5% in 2020 and just 4.4% in 9M 2021 due to the pandemic-related travel restrictions. All five of the leading Western European airline groups (Ryanair, Lufthansa, IAG, Air France-KLM and EasyJet) have limited direct exposure to Russia. However, removing Aeroflot (SkyTeam) and S7 Airlines (oneworld) from the worldwide alliances could affect routes not served by members of the alliances.

Moreover, closing airspace over Russia and Ukraine is limiting Western airlines’ routing options, leading to longer flight times, adding 15 minutes to 5 hours per journey. With jet fuel prices surging to near-14-year highs (fuel constitutes 35-40% of an airline’s operating costs), airlines’ recovery plans for 2022 could be jeopardised. The airlines would have no option but to pass on this cost to passengers by raising fares through surcharges. However, this would not be easy given the surge in inflation and lower consumer discretionary income. Those airlines that have hedged most of their fuel requirements would be in a better position than airlines that have not hedged them.

Aircraft manufacturers (Airbus, Boeing and Embraer).

Russian airlines have a total of 332 Boeing, 304 Airbus and 23 Embraer jets, accounting for two-thirds of Russia’s fleet (source: Cirium). Currently, 64 planes are on order by Russian airlines – 22 from Airbus and 42 from Boeing. Given the long lead times, it is not difficult for aircraft manufacturers to sell their new planes. Moreover, Boeing, which depends on Russian imports for 35% of its titanium (a key metal, making up 15-20% of an aircraft), has suspended buying titanium from Russia. However, Airbus, which imports 50% of its titanium requirement from Russia, and Embraer, which sources 100%, may feel a greater impact. With lower production of aircraft due to the pandemic, we believe plane makers currently have enough inventory and are in contact with other suppliers for future requirements.

Lessors.

515 of Russia's 980 passenger planes are on lease from foreign aviation firms; terminating these lease agreements with Russian carriers would cost c.USD13bn. Moreover, many Russian carriers rely on lines of credit to pay for their aircraft and could struggle to pay their dues due to sanctions on banks they use and restrictions on the SWIFT international bank transfer system, which could lead to multiple failed payments. With such restrictions in place, lessors would also find it difficult to get their aircraft out of Russia (only about 24 planes have been repossessed so far). On 14 March 2022, Russian President Putin signed a law allowing Russian airlines to take control of their leased planes and add them to the country’s aircraft register, to be deployed on domestic routes. This could have a sizeable impact, with lessors having to write off these assets and triggering lengthy court battles.

What is the way forward?

To withstand pressure from the West, the Russian government may nationalise its airline industry by taking over other airlines and their leased aircraft and merging them with Aeroflot, the state-owned national carrier, which currently operates the youngest fleet in the industry (average age of just five years). To neutralise the ban from plane manufacturers, the government may encourage and expedite local manufacturing of civil aircraft MS-21 and Superjet-100, although these are mostly smaller airplanes designed for short-haul flights. Russian airlines are currently using only locally manufactured aircraft on international routes; these are owned by Russia and have no risk of being detained abroad. Considering the restrictions in place, Russia does not require wide-bodied planes for long-haul routes. For parts, airlines would have to use their current stockpiles, buy from friendly countries (although China has already refused) or ground some aircraft and cannibalise them for spare parts (prohibited under lease terms). The airlines would also be forced to furlough staff and freeze recruitment. Six Russian airlines (with about 250 flights a week) still fly international routes (limited to 10 countries), while 29 foreign airlines still service Russia, according to Russia’s Federal Air Transport Agency.

Sources:

-

https://www.aerotime.aero/articles/30387-uk-bans-russia-from-aviation-insurance-market

-

Russian airlines face outcast status as jetmakers freeze parts | Reuters

-

Airspace closures create new challenges for airlines around the world (thepointsguy.com)

-

IATA: Global Air Traffic Demand in 2021 Down by 58.4% Over pre-Covid 2019 Levels | GTP Headlines

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Nishant Mishra [Associate Director, Acuity Knowledge Partners (Acuity)] has close to 18 years of work experience in investment research, including 14 years at Acuity, with a focus on the transport, utilities, capital goods and energy sectors. With expertise in both equity and fixed income research, he currently leads teams that provide research support to European buy- and sell-side clients. The work involves building detailed financial models, distressed debt analysis, writing initiation reports and assisting clients with investment decisions for investment-grade, high-yield and distressed-debt companies in developed and emerging markets. He acts as a single point of contact for clients and ensures the team delivers high-quality output in line..Show More

Blog

Blog

Advanced air mobility (AAM): A promising future....

Advanced air mobility, or AAM, refers to a new air transport ecosystem that leverages adva....Read More

Blog

Blog

India’s first international hub: close to beco....

Key takeaways Robust economic growth, an increasing middle-class population and to....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox