Published on May 8, 2024 by Zahoor Bhat and Samrat Prabhu Dessai

The GCC economy, set for a strong 2024 with its favourable demographics, robust government spending, positive sentiment and growing job market, is steadily becoming one of the most desirable regions for investment. According to the IMF’s January outlook, the Middle East and Central Asia are expected to grow by 2.9% in 2024 and by 4.2% in 2025. This is almost double the forecast for advanced economies, which are expected to increase by 1.5%. Although the fundamentals of the economy still revolve around oil, growth in non-oil sectors continues.

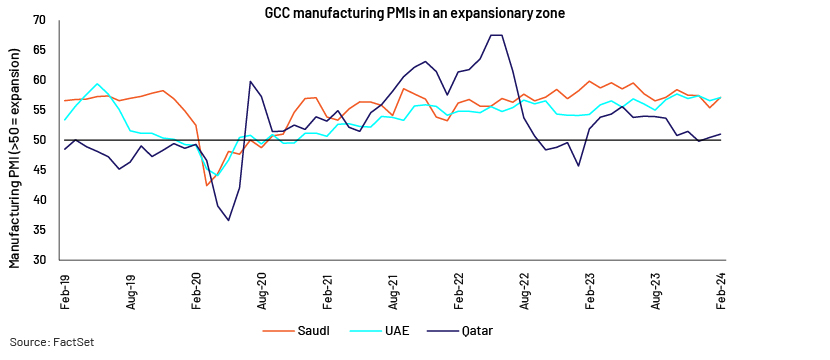

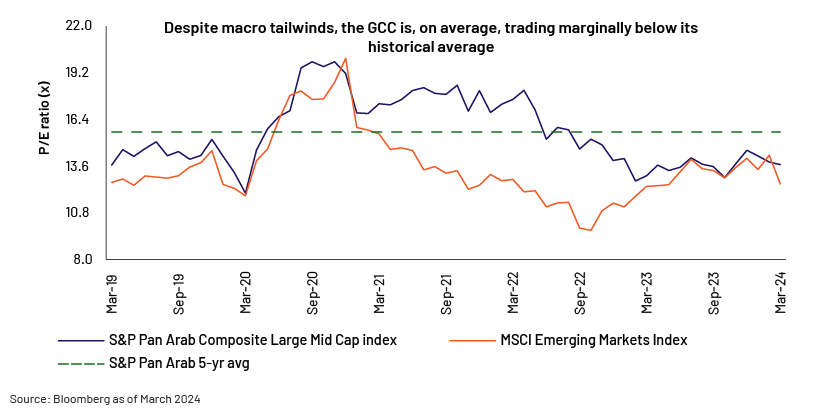

Saudi Arabia and the UAE, two of the largest GCC economies, have reported PMIs of above 50 (>50 indicates expansion) since December 2020, and sentiment is expected to remain firm, pointing to an optimistic demand picture. The region’s relative valuations also remain modest despite the recent de-rating of emerging markets. Large- and mid-cap companies in the GCC market reported dividend yield of 3.9% as of March 2024 versus 3.1% in emerging markets. The S&P Pan Arab P/E is trading at close to 13.7x, c.9% above emerging markets’, reflecting its relatively strong outlook, but c.20% below its own five-year historical average, indicating upside potential. Saudi Arabia, the UAE and Kuwait remains the most attractive markets, considering their structural reforms and higher non-oil growth.

Key markets in 2024

The UAE is likely to be the region’s best-performing market

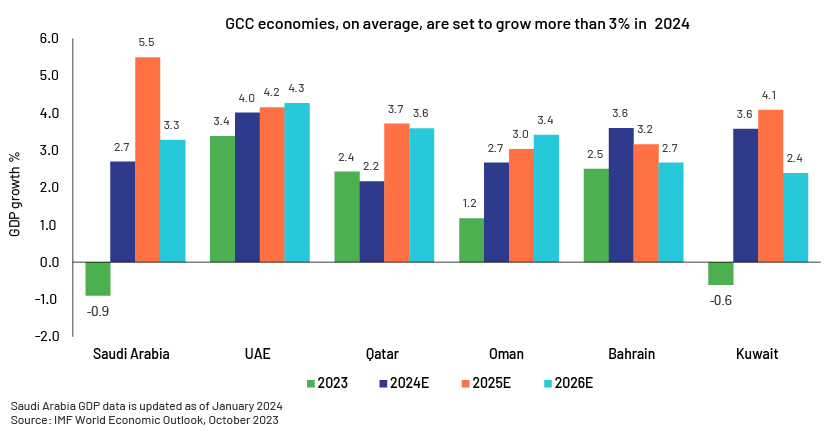

Structural reforms, favourable demographics, strong growth and a growing population make the UAE the most attractive GCC market in 2024. Despite weaker global growth and higher rates in 2023, the UAE is forecast to grow by 3.4% in 2024, ahead of the OECD’s global growth projections. According to the IMF’s October outlook, growth will remain steady at over 4% until 2026. More importantly, this growth has been broad-based, driven by multiple sectors. S&P’s recent PMI data suggests an increase in non-oil activity, with c.36% of respondents seeing an increase in output versus the previous survey period, indicating strong demand. Its job market also remains buoyant. According to Hays Middle East, c.80% of employers in the UAE plan to increase salaries this year. The government has also taken measures, such as implementing visa- and business-related reforms, which should further support the growth plan.

Saudi economy poised for a strong recovery in the coming years

After a tough 2023 due to a decline in oil-related activity, Saudi Arabia (the GCC’s largest economy) is expected to grow by 2.7% in 2024 and 5.5% in 2025, according to the IMF’s latest forecast. While oil remains the key driver, non-oil growth is expected to contribute significantly, buoyed by investment and consumer spending. Saudi Arabia’s non-oil activity grew by 4.4% in 2023, led by social and personal activity (+10.8% y/y), and accounted for c.50% of the country’s real GDP, according to the General Authority for Statistics. Non-oil growth is expected at above 5% in the medium term, likely to outperform the wider region. Government spending also remains strong and in line with its Vision 2030 strategy. Total spending in 2024 is forecast at SAR1.25tn.

Kuwait is on an upward trajectory

Kuwait is currently the 10th largest economy in the Middle East and North Africa (MENA) region. It remains on an upward trajectory, driven by the expansion of non-oil activity, strong corporate performance and a pick-up in legislative reforms, according to the latest report from Kuwait Financial Centre “Markaz”. Net loans and deposits grew at the fastest rate among GCC countries y/y in 3Q23 and are expected to grow by c.6% y/y in 2024, driven by growth in business and household credit. This follows strong credit growth of 26% in 2022. Government spending – estimated at c.50% of GDP – would also boost demand. Kuwait also has large foreign assets in its sovereign wealth fund, managed by the Kuwait Investment Authority, and one of the world’s most valuable currencies.

The GCC has improved its fiscal performance amid global uncertainty and remains poised for growth

The UAE is expected to lead with constant growth of over 4% in the next three years. The GCC’s largest economy, Saudi Arabia, is also expected to rebound after a decline in 2023, although the IMF reduced its growth projection by 1.3ppt in January 2024 versus that in October 2023. Kuwait is thriving as well. Overall, GCC economies, on average, are expected to grow by c.3.4% y/y until 2026.

Government investment also remains robust, with most of the economies investing almost a quarter of their GDP; Kuwait invests the most (more than 50%). Despite this, public finances have improved, with government debt as a percentage of GDP expected to reduce 3ppt in 2024 versus that in 2021.

Strong PMI numbers paint a positive demand picture

Saudi Arabia, the UAE and Qatar reported manufacturing PMIs of 57, 57 and 51, respectively, in February 2024. PMI numbers have been hovering above 50 since January 2023, indicating strong demand and growing job markets.

High lending rates have not affected growth in lending

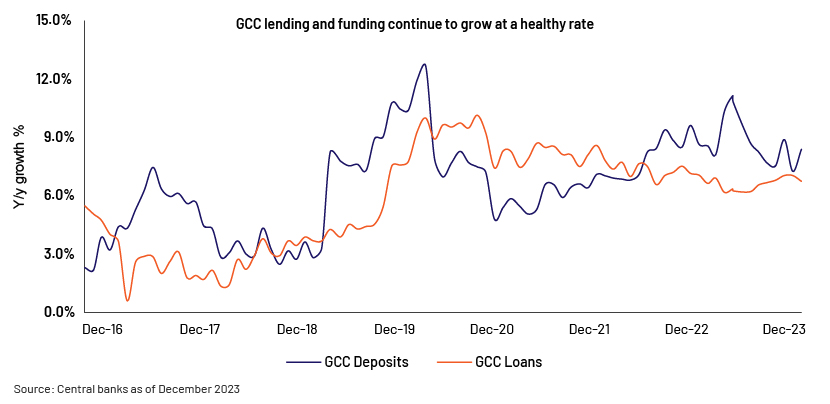

Robust fundamentals, healthy project pipelines, strong demographics and government efforts have ensured strong lending growth., The strong growth is also due to impetus from big-ticket projects and reforms, according to a report by Kamco Invest. Lending in the GCC region grew by 6.8% in 2023 while deposits grew by 8.4%.

Fall in interest rates would further boost the economy

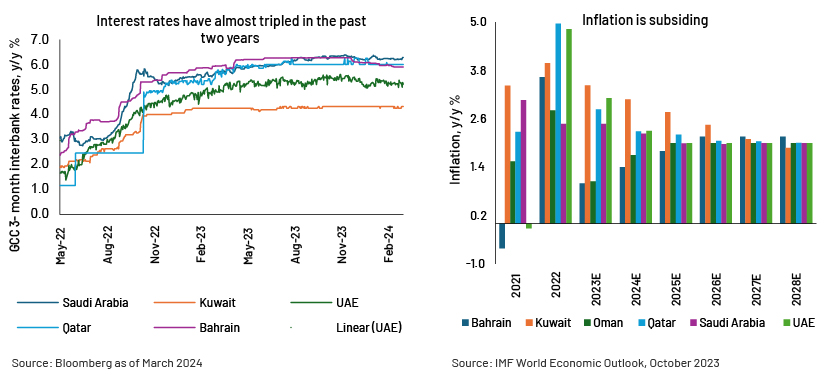

Most of the GCC region's currencies are pegged to the USD. As a result, interest rates tend to move in line with the Fed rate. Interbank rates have almost tripled in the past two years due to rising inflation. The recent decline in prices likely suggests that the region is reaching the end of the rate-hiking cycle. Inflation growth in GCC countries is expected to halve by 2024-25, accelerating rate cuts thereafter.

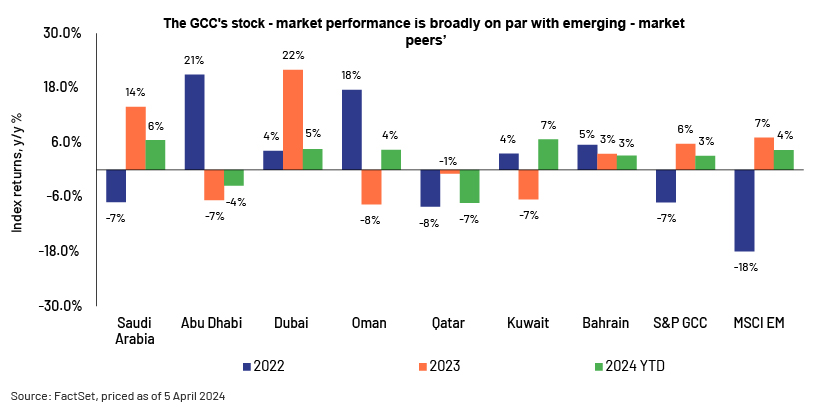

GCC’s stock performance in line with emerging-market peers’ but its premium valuation reflects a strong outlook

The GCC market had a mixed 2023. S&P GCC increased by 5.7%. led by Saudi Arabia (+14%) and Dubai (+22%), whereas Abu Dhabi and Oman were down by 7% and 8%, respectively. Overall, it was broadly in line with emerging-market peers’, which grew by c.7% y/y (see chart below).

2024 has got off to a similar start. S&P GCC is up by 3.0% YTD, broadly 1ppt behind emerging-market peers. Among GCC nations, Kuwait has been the best performer so far in 2024, up 6.7% YTD, followed by Saudi Arabia (+6.5%), Dubai (+4.5%) and Oman (+4.4%); Qatar is down 7.3%.

On a P/E basis, the S&P Pan Arab Composite Large Mid Cap index was trading at 13.7x as of end-March 2024, c.9% above MSCI Emerging Markets but c.20% below its own historical five-year average (see chart below).

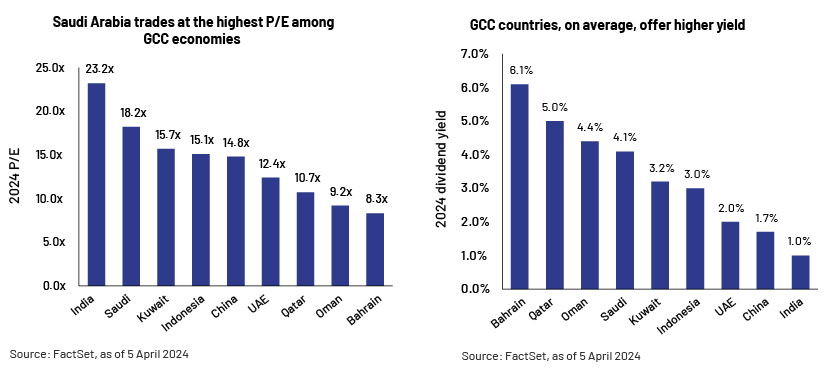

Saudi Arabia’s 2024E P/E is currently at 18.2x, at the highest among GCC economies’, followed by Kuwait at 15.7x, ~20% and ~30% discount to India, respectively, while others are trading at a relatively modest valuation behind India, Indonesia, and China. Bahrain currently offers the highest dividend yield (6.1%) among emerging-market peers, followed by Qatar at 5.0% and Oman (4.4%).

How Acuity Knowledge Partners can help

Global investment banks and asset managers leverage our sector-specific/macroeconomic experience to rapidly increase internal analyst bandwidth and expand coverage. We set up dedicated teams of analysts (CAs, MBAs, CFAs) to support our clients on a wide range of activities including idea generation, macroeconomic research, financial analysis, thematic research, building databases and providing regular sector coverage. Each output is customised, based on the client’s requirement, and made available for their exclusive use. This ensures our clients a unique, sustainable edge.

Sources:

-

S&P Global Dubai PMI – Dubai PMI rises to highest level since May 2019

-

WEO Update, Jan 2024: Moderating Inflation and Steady Growth Open Path to Soft Landing

-

Saudi Arabia's non-oil activities comprised 50% of country's real GDP

Tags:

What's your view?

Thank you for sharing your Comments

Share this on

About the Authors

Zahoor has over twelve years of experience in equity research, covering the technology, banking, telecom and cement sectors , with expertise in financial modelling, valuation methodologies, writing research reports and other research-related work.

At Acuity Knowledge Partners, he supports a private equity and asset management team in the GCC with over USD3bn worth of assets under management. He covers different asset classes (fixed income, equities, REITs) and has developed different investment strategies to help the client earn the highest return on investment.

He previously supported a sell-side client, covering Saudi Arabia’s banking, telecom and cement sectors. He holds a B.E. (Computers) from Jammu University and an MBA (Finance) from ICFAI Business..Show More

Samrat Prabhu Dessai has around 8 years of experience in investment research. He has been with Acuity Knowledge Partners (Acuity) since Aug-2023 and has worked in buy-side engagements. He currently manages delivery for a leading buy-side client in the Middle East, supporting them with their research needs, and covering multiple sectors. Prior to joining Acuity, he worked with HSBC covering UK Industrials. He has experience in equity research and financial modelling. Samrat has cleared CFA level 2 and holds a post graduate diploma in Management from Goa Institute of Management.

Blog

Blog

Navigating through Indian Markets under the Coal....

India’s coalition governments have historically resulted in market volatility in the sho....Read More

Blog

Blog

Silver lining to the inflation curse....

When members of the Federal Open Market Committee (FOMC) express vastly divergent views in....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox