Published on November 26, 2019 by Prashant Gupta

The global private equity (PE) industry has been very successful in the past five years: more capital was raised, invested, and distributed to investors than in any other period.

With the economic expansion continuing in 2019, the global PE industry has continued to make deals, find exits and raise money at the same rate as in the past five years. Limited partners (LPs) are highly active and continue to pour fresh capital into the market. Some large investors, who previously chose to stay away, are now also investing in private markets, as they believe it is an important asset class that offers diversification for overall growth. There are also more general partners (GPs) and LPs participating in the market than ever before. The net asset value of the global PE market grew 7.5x from 2002 to 2017, while public market capitalization grew c.3.5x.

Global PE net asset value has grown more than sevenfold since 2002, outpacing public market equities

The good: The strengths so far:

Despite fierce competition and soaring valuations, which continued to constrain deal count, total buyout value grew 10% to USD582bn in 2018. Similar resilience and strength were also visible through Q1 2019. Since 2014, every year (with the exception of peak years 2006 and 2007) has witnessed higher deal value than any year in the previous cycle. Over this period, the PE industry has benefited from extraordinary investor interest, supported by low interest rates and steady GDP growth in the US and Europe. In terms of its structures and behaviour as well, the PE market is more flexible and offers ways for investors to customize their exposure; it is, therefore, able to accommodate a range of investors and provide adequate diversification.

The bad: While the good times are progressing, some signs of worry are appearing:

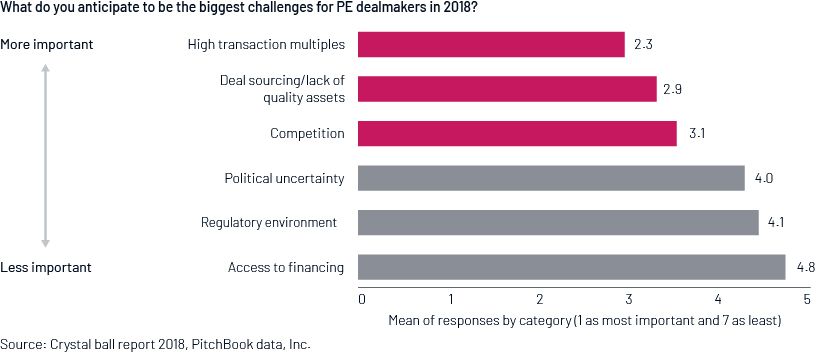

Maintaining the pace of growth is not easy, as with growth comes maturity. Today’s PE marketplace raises issues – both for GPs and LPs – that did not exist initially. The biggest challenges facing PE firms looking to close deals are high deal multiples, the scarcity of attractive targets and heavy competition. Increasing concerns about an economic downturn are also affecting decision making – from conducting due diligence to formulating exit plans. Volatile capital markets, global trade tensions, the ongoing uncertainty about Brexit and the fear of recession have aggravated the ambiguity. Additionally, the speed of technological change is increasing in almost every industry, making it difficult for dealmakers to forecast winners and losers. Although market returns remain stronger than those from other asset classes, they have been declining gradually toward public equity market aver¬ages in the past five years.

The way ahead:

Bull markets do not roll forever, and there is much speculation about when this decade-long expansion in the private market will lose rhythm. Despite solid investment growth since 2014, PE dry powder has been increasing since 2012 and hit a record high of USD2tn in December 2018 across fund types. With such record amounts of capital in hand, PE funds are facing a growing need to invest it. We are also concerned that the industry may be getting ahead of itself, much as it did during the global financial crisis of 2007 and 2008, which stalled deal-making activity, leaving GPs with substantial amounts of dry powder and seeking extensions.

Current characteristics of PE markets resemble those before the crisis in 2007: for example, PE deal volume in 2018 exceeded previous highs, deal pricing is similar, and covenant-lite loans are everywhere. Of course, the future is uncertain, but we believe that with record amounts of capital in hand, GPs have a responsibility to tap the market instead of sitting idle, timing it. We expect them to find ways to manage the increasing macro uncertainty and to plan prudently to profit from the downturn. With memories of the last financial crisis still fresh, we expect PE firms to be more diligent and focus more carefully on downside scenarios this time round.

Acuity Knowledge Partners’ PE/VC experts help clients across the investment cycle. Our support includes screening companies, working on pre-financing strategies, conducting commercial and operational deeper due diligence, and post-investment performance review.

Sources:

McKinsey Global Private Markets Review 2019

Global Private Equity Report 2019: Bain & Company

Q1’19 edition of KPMG Enterprise’s Venture Pulse

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Prashant is a seasoned professional within the Private Market team and has been with the company for over 12 years. His extensive career spans more than 18 years, during which he has garnered a wealth of experience through a diverse range of research and analysis assignments. His clientele is impressive and varied, including top-tier asset managers, private equity firms, and bulge bracket investment banks.

His expertise is broad and deep, with a particular focus on comprehensive end-to-end credit analysis.Prashant’s skill set encompasses capital structure analysis, intricate corporate structure assessments—including guarantees and structural subordination cases—and covenant compliance analysis. Additionally, he is adept at financial modeling and valuation, asset recovery analysis,..Show More

Blog

Blog

Crossing Lines: The Banking Industry’s Fora

Introduction: Banks’ foray into private credit The financial landscape seems to be shi....Read More

Blog

Blog

Streamlining investment success: the integral

Introduction In the complex arena of private credit, the path to investment success is pa....Read More

Blog

Blog

Mastering the market: strategic advisory and

Introduction: Paving the way for strategic growth in private credit The private credit m....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox