Published on November 23, 2023 by Maruti Patnaik

Banking-as-a-Service (BaaS) and composable banking are two developing financial services sector innovations that are changing the way banks provide financial services.

BaaS is a cloud service that enables banks to quickly and simply construct new financial products and services without having to invest in the underlying technology and infrastructure. In the financial sector, BaaS is swiftly gaining traction, as it enables provision of banking services via digital channels as opposed to via traditional brick-and-mortar branches. BaaS is a method for fintech companies to collaborate with banks to make the banks’ financial products (such as bank accounts and credit cards) available to their customers. BaaS entails a bank permitting another organisation (fintech/non-bank) to provide financial services, or a bank offering a new and creative product in collaboration with a technology business.

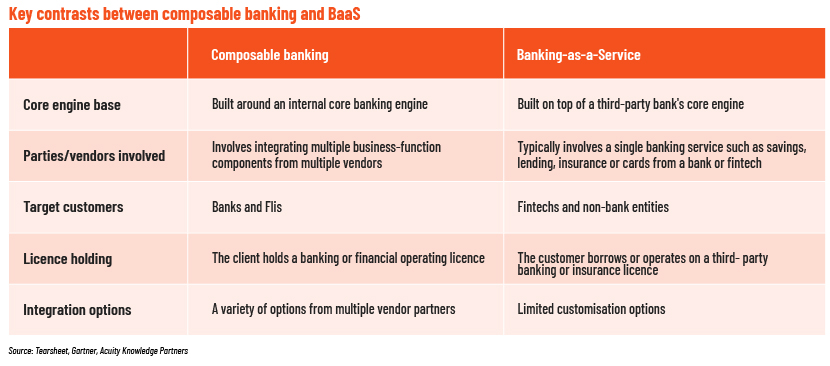

Composable banking, on the other hand, is a newer approach to banking that takes BaaS one step further. It enables banks to construct and disassemble financial services components to develop tailored solutions that match their customers' specific needs.

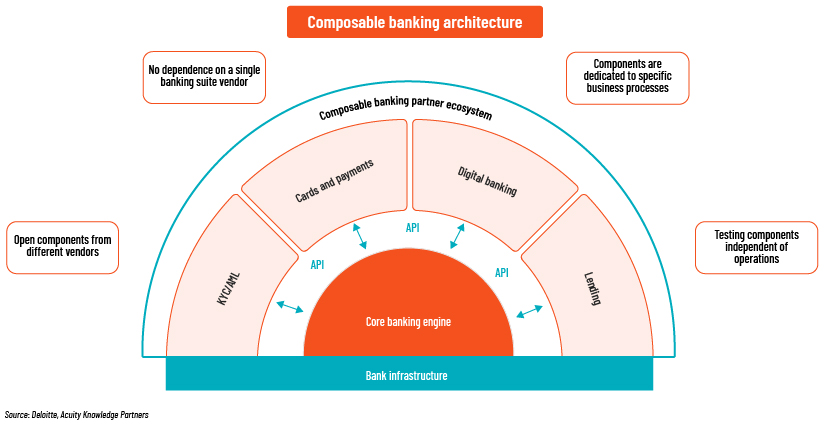

Composable banking is based on the principles of modularity, reusability and flexibility. The approach enables financial institutions (banks and credit unions) to enhance and increase the functionality of their existing technology infrastructure by leveraging modular components from external partners. These components can be reused, repurposed and replaced to keep back-office systems nimble. A central banking engine in composable banking synchronises a number of independent components via open application programming interfaces (APIs).

The composable banking ecosystem

A composable banking platform is independent and can run in any environment, including on the public cloud or as Software-as-a-Service (SaaS). It is database-agnostic and leverages APIs. Composable banking is an approach to designing and delivering financial services, and it continues to evolve based on the rapid and flexible assembly of independent, best-suited systems. As a result, it enables traditional banks to be as flexible as challengers.

Composable banking architecture involves leveraging the best-suited components across segments (lending solutions, onboarding solutions, wealth management, trading platforms, customer-facing solutions, etc.). This helps incumbents fight off disruptors and neobanks by building new business streams rapidly and lowering their time to market.

Key advantages of composable banking:

-

Flexibility: Freedom to quickly combine and test new functions and processes

-

Speed to market: Launch new banks in a short period of time (weeks or months)

-

Low vendor dependency: Banks are not bound to source smaller modules from a single vendor

-

Agile configuration and testing: Developers can trial and test a component without hampering the bank’s operations

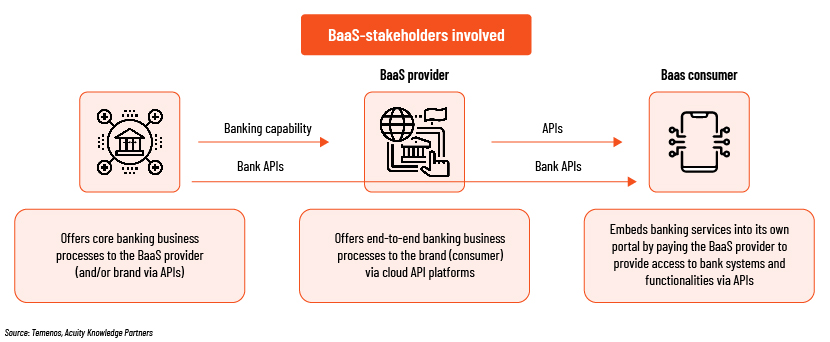

The BaaS ecosystem

BaaS offers a fundamentally different approach to financial services by placing banks’ building blocks in the hands of a wider range of stakeholders. The BaaS ecosystem comprises three stakeholders, namely the fintech (consumer of BaaS), the BaaS provider (tech enabler) and the financial institution (banking licence holder).

-

Fintech – the consumer of BaaS: Its main goal is to establish its own unique core differentiating digital proposition without engaging itself in a banking licence or investing in regulated banking infrastructure

-

BaaS provider – the tech enabler: Provides modular banking services through APIs to customer-facing organisations. These providers either have their own banking licences or partner with banks to leverage their banking licences

-

Financial institution – the banking licence holder: It rents its licence to the BaaS provider by giving access to the underlying technology infrastructure, schemes and products

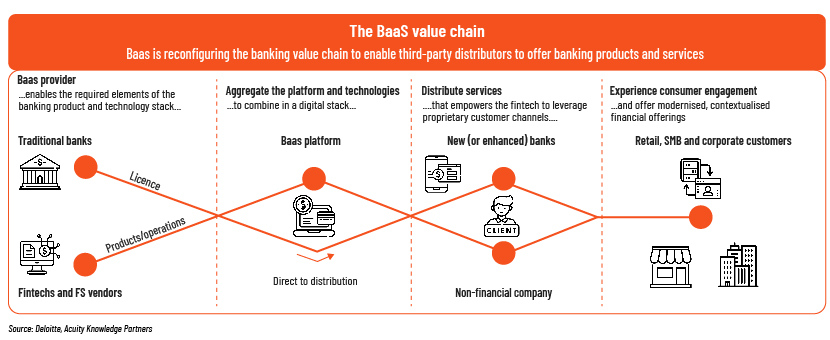

The BaaS model is a means of helping non-banking entities to enhance customer engagement by adding a financial service. For example, it enables an ecommerce provider to build a digital wallet to help customers store and manage money. Similarly, it can enable a point-of-sale (POS) provider to build POS loans/buy now, pay later (BNPL) schemes and empower a marketplace aggregator to distribute financial products such as investments and insurance. Even banks can leverage the BaaS model to build pilot projects and venture into new domains. They could experiment with new digital lending platforms and investment products without having to build and invest in the underlying technology infrastructure.

How Acuity Knowledge Partners can help BaaS and composable banking solution providers

We have the resources and expertise to offer consulting services around these emerging technology domains. We can offer peer insights to BaaS providers in terms of deployment, delivery and distribution strategies, and benchmark capabilities and features with industry leaders. We also help BaaS providers identify and size up their target markets, to develop products and services that meet the needs of these markets.

We also help composable banking providers improve their market position by identifying competitors’ go-to-market strategies, product models, messaging, distribution partners and marketing campaigns.

Sources:

-

Why Composability Is the Future of Banking (internationalbanker.com)

-

banking-as-a-service_100_billion-opportunity_europe_vf.pdf (mckinsey.de)

-

Temenos Wins Best Core Banking Solution Provider at the Banking Tech Awards 2022 – Temenos

-

Banking As a Service (BaaS) Explained & Industry Outlook 2023 (insiderintelligence.com)

Tags:

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Maruti has more than 10 years of experience in technology research and consulting. He currently works with the marketing and research teams of a leading fintech supporting them execute their go-to-market strategies. Prior to joining Acuity Knowledge Partners, Maruti worked for GlobalData where he worked on areas around emerging themes such as AI, business intelligence, cloud, 5G, payments, and retail.

Blog

Blog

Interest Rate Divergence in 2024: A Global Conte....

Interest rates are diverging sharply in major economies, most notably in the US and the Eu....Read More

Blog

Blog

Pros & Cons of Adopting Cloud Based Technol....

Cloud Based Technology in Banking Cybersecurity Risks: The financial sector faces signifi....Read More

Blog

Blog

Driving the success of compliance functions: Acu....

In the fast-paced and highly regulated world of finance, compliance is not just a necessit....Read More

Blog

Blog

Landscape of fintech investments and associat

The fintech sector is growing exponentially, holding the attention of many investors over ....Read More

Blog

Blog

Payments evolving to accommodate cross-border

Cross-border payments and real-time payments are becoming two critical factors in streamli....Read More

Blog

Blog

Alternative lending – an exciting growth op

Alternative lending refers to loan options available to consumers and businesses other tha....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox