Published on May 8, 2024 by Chamini Apeksha Thalakotunna

Climate change is acknowledged as the most significant threat of the century, according to the Intergovernmental Panel on Climate Change (IPCC) and the United Nations Framework Convention on Climate Change (UNFCCC). The decade that ended in 2020 was the decade of the highest temperature, with global average temperature increasing 1.1°C above pre-industrial levels in 2019. An escalation of 2°C compared to pre-industrial levels is associated with severe adverse effects on both the natural environment and human wellbeing. To mitigate this, the international community has recommended keeping the annual increase in global warming well below 2°C, preferably at 1.5°C.

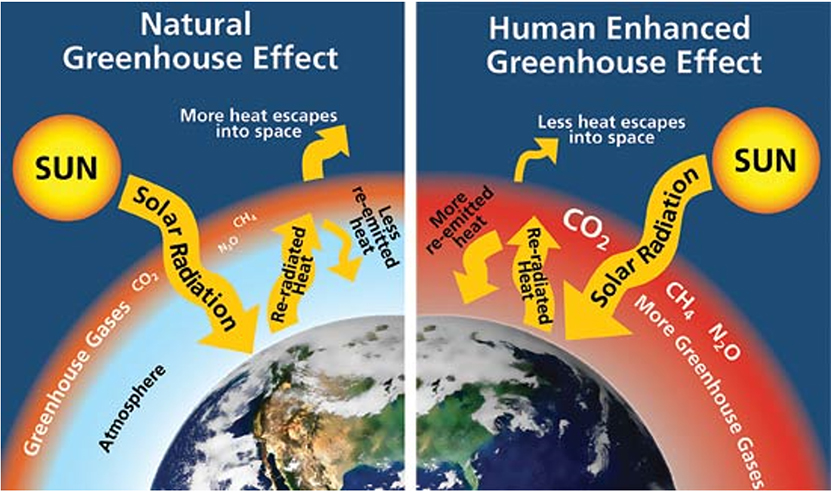

The main reason for climate change is the greenhouse effect, where certain gases in the Earth's atmosphere function similar to the glass of a greenhouse. The atmospheric concentration of CO2 had increased by 48% as of 2020 from its pre-industrial level before 1750.

Triggers of transformation: exploring the catalysts of climate change

There are several causes of climate change; these fall mainly under two umbrellas:

-

Natural causes: The Earth’s climate is affected by natural causes such as ocean currents, volcanic activities, the Earth’s orbital changes, cloud contributions and solar variations.

-

Human causes: Research by Paehler in 2007 showed that changes in climate are due to human-induced greenhouse gas (GHG), from the combustion of fossil fuels for purposes such as electricity generation, transport and residential heating. This includes practices such as gas flaring in oil fields, as observed in locations such as Nigeria. Modifying land use and deforestation also contribute to the accumulation of GHGs.

Earth under pressure: the evolving impact of climate change

The effects of climate change are widespread and impact various aspects of the Earth's systems. Heightened temperatures and sea levels rising are some of the key effects of climate change. Increases in global temperature have led to more frequent and intense heatwaves. This could have direct effects on human health, agriculture and ecosystems. It could also contribute to the spread of vector-borne diseases, such as malaria and dengue fever, while extreme weather events such as hurricanes, droughts, floods and wildfires can lead to injuries, displacement and mental health issues. Finally, the absorption of excess atmospheric CO2 by oceans results in increased acidity that can harm marine life, such as coral and certain shellfish.

Risk on the rise: the impact of climate change on credit risk

Considering the increasing repercussions of climate change, a number of sectors face considerable exposure to either physical or transition risk, or both. Specifically, certain segments may have activities, products or services that are vulnerable to carbon-related risks, anticipating structural changes in their business models. Based on analysis by MSCI, 16% of the investment-grade issuers in the sample could face downgrades to high yield in a “net zero by 2050” scenario.

The banking sector is the key force behind the global economy and finds itself at the forefront of these transformative shifts. To withstand the impact of global warming, banks need to take a leadership role, incorporating climate change-related considerations into their risk management framework. Regulatory and supervisory bodies such as the Task Force on Climate-related Financial Disclosures (TCFD) and the Network for Greening the Financial System (NGFS) have taken a number of initiatives and measures in recent years.

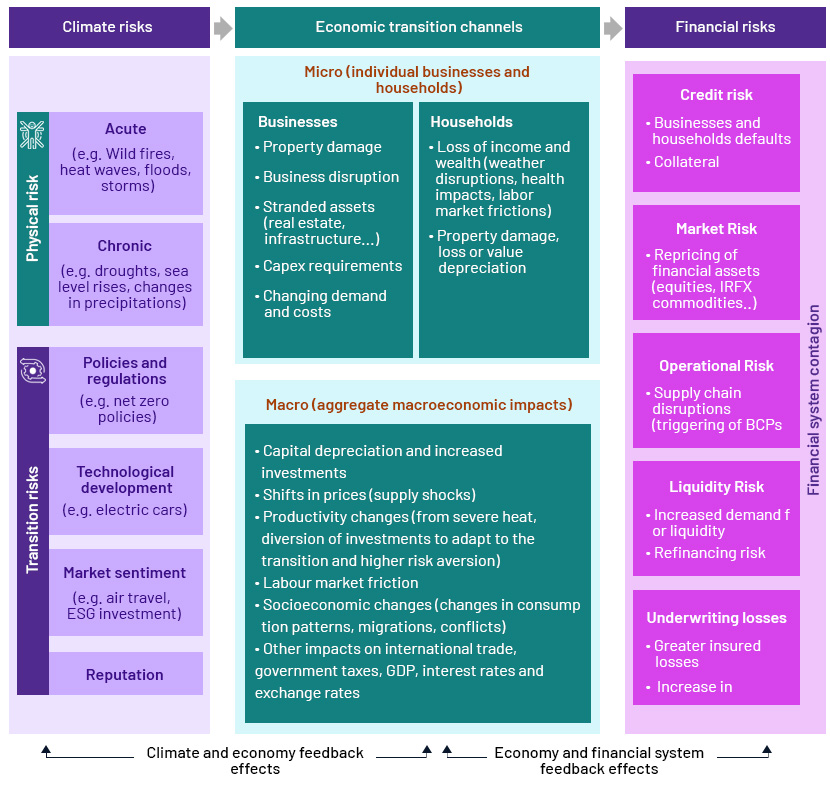

The banking sector faces exposure to climate change through both macroeconomic and microeconomic channels, stemming from physical and transition risk drivers. The influence of climate risk drivers on banking institutions can be detected across a number of financial risk categories such as credit risk, market risk, liquidity risk, operational risk and reputational risk. The graph below illustrates the impact of climate risk on financial risk, specifically credit risk.

Figure 3: Impact of climate-related risk on financial risk

Source: Integrating climate risk into credit risk modelling: Avantage Reply

| Transition risk | Physical risk | |

| What is it? | Risk emerges when an organisation manages and adapts to the internal and external pace of change to reduce GHG emissions and transition to renewable energy | Risk results from the impact of climate change. It could be event-driven (acute) or associated with longer-term shifts in climate patterns (chronic) |

| How can it affect a firm’s cash flow? | R&D expenditure Capital investments Reduced demand for carbon-intensive products and services Increased production costs due to high input prices and output requirements | Reduced revenue from decreased production capacity (e.g., due to supply-chain interruptions) and lower sales Increased operating costs (e.g., due to the need to source inputs from more expensive suppliers) Increased capital expenditure (e.g., to repair damaged facilities) |

| How does it affect a firm’s assets? | Potential re-pricing of idle fossil fuel assets Changes in real estate valuation | Direct damage to assets Write-offs of assets in high-risk locations |

| Examples | Policy and regulation (e.g., carbon tax) Technological developments (e.g., electric vehicles) Consumer preference Market reputation | Chronic (e.g., temperature rising, sea levels rising) Acute (e.g., heat waves, floods) |

Table 1: Transition risk vs physical risk

United for change: collaborative efforts in climate risk management

Paris Agreement

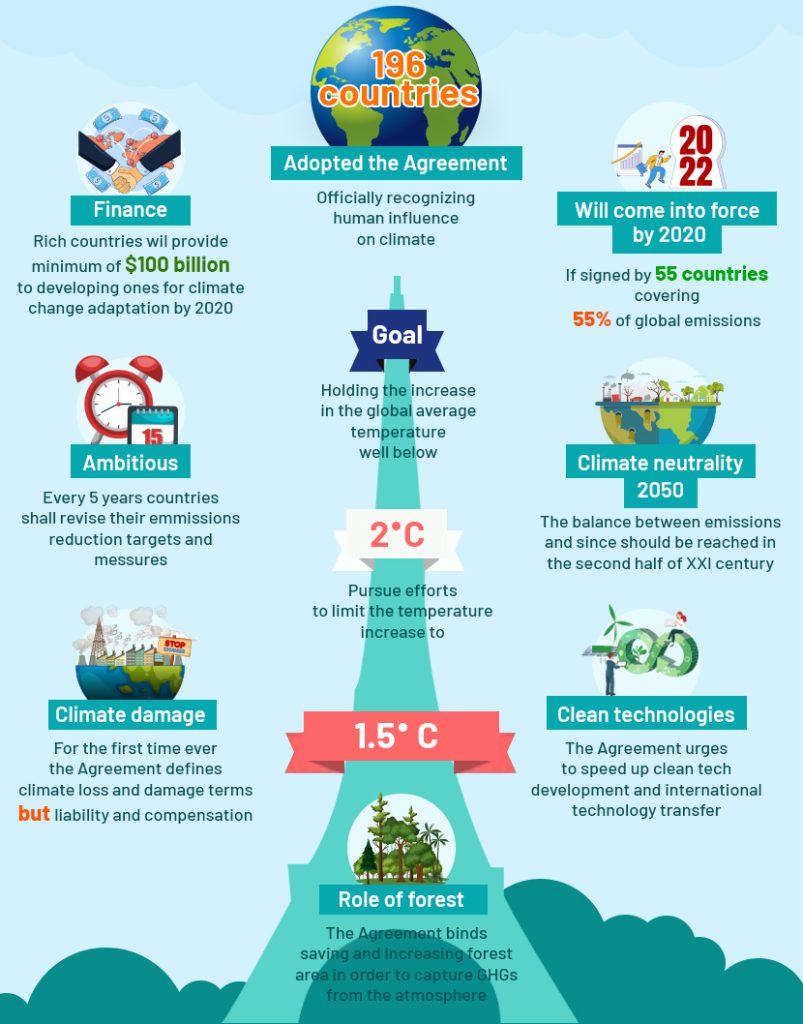

The Paris Agreement is a legally binding international UN treaty under the UNFCC. It was embraced by 196 parties at the change conference in Paris in 2015. It aims to keep the annual increase in global warming to well below 2°C, with the ambition to limit the increase even further, to 1.5°C compared with pre-industrial levels. To limit it to 1.5°C, GHG emissions would need to peak before 2025 at the latest and decline by 43% by 2030.

Although measures to mitigate climate change need to be expedited if the goals of the Paris Agreement are to be achieved, the introduction of the agreement has already triggered low-carbon solutions and new markets, and the establishment of carbon-neutrality targets and zero-carbon solutions.

Net-Zero Banking Alliance (NZBA)

Figure 5: Net-Zero Banking Alliance

The NZBA is recognised as part of the Glasgow Financial Alliance for Net Zero (GFANZ), which consists of seven alliances, each covering a specific part of the financial sector. The NZBA is an international coalition of banks that currently account for approximately 40% of global banking assets. These banks have pledged to reduce emissions from their portfolios to achieve net-zero status by 2050.

Banks that register with the NZBA make the following commitments:

-

Adjust operational and attributable GHG emissions from their lending and investment portfolios to conform with pathways leading to net zero by 2050 or earlier

-

Within 18 months of joining, establish targets for 2030 (or earlier) and a 2050 target, with intermediate goals set every five years starting from 2030

-

The initial 2030 targets will concentrate on priority sectors where they can have the most significant impact, specifically those sectors with the highest GHG intensity in their portfolios. Additional sector-specific targets will be established within 36 months

-

Annually disclose absolute emissions and emission intensity according to best practices and, within a year of setting targets, report progress against a transition strategy reviewed at the board level, outlining proposed actions and climate-related sectoral policies

-

Have a strong approach to offset their transition plans

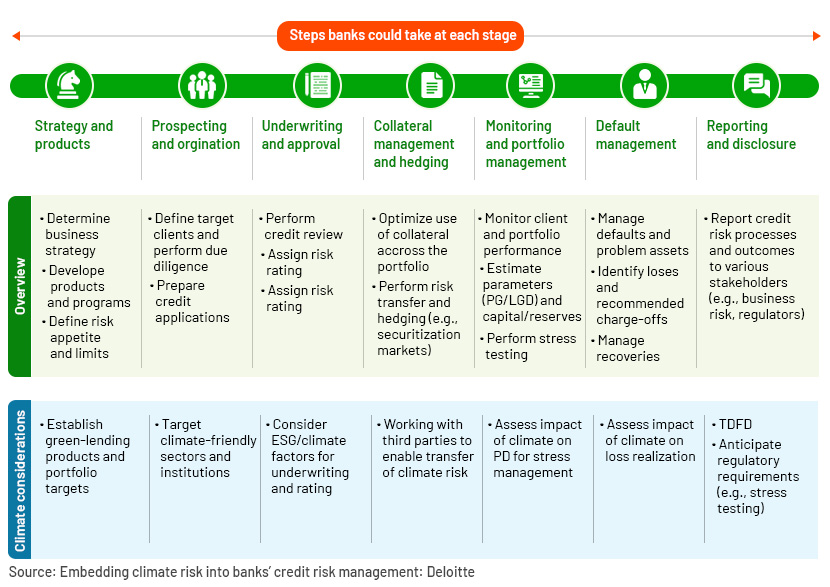

Beyond banking: initiatives to mitigate climate risk in credit lifecycles

Figure 6: Actions banks could take to mitigate climate risk over the credit lifecycle

Strategy and products

To begin with, banks should review their credit business strategies by reevaluating potential markets, segments and clients, as well as the products and innovations they aim to introduce. The updated strategies should align with the banks' sustainability commitments, which may include targets for lowering financed emissions or minimising overall risk exposure.

Banks must create a taxonomy and a chart detailing climate risks and the pathways through which they are transmitted, such as macroeconomic consequences, shifts in customer preferences or disruptions to business operations. They should translate the overall credit business strategy and product emphasis into suitable risk tolerance, credit risk procedures and policies. Moreover, they can accelerate product innovation to factor in climate risk and decarbonise their portfolios. A number of banks are broadening their range of green-lending products to offset financed emissions.

Prospecting and origination

At the start of a new client relationship, a bank should evaluate its effect on physical and transition risks. Prospecting and origination should be guided by the bank's business strategy in terms of selecting sectors and clients.

The level of due diligence depends on factors such as the client’s economic sector, size and location. Banks examine businesses at the know-your-customer (KYC) stage of documentation by requesting additional information including energy use for new business flows, supply-chain data and emissions per unit of revenue. In addition, credit risk departments should collaborate with other units to prioritise deals that reduce climate risk or introduce eco-friendly tech opportunities.

Underwriting and approval

As the third step, a bank should integrate climate risks into its credit rating and underwriting process. Banks are now creating standalone borrower-specific climate risk scores. These assessments should consider a client’s physical and transition risks, its resilience to climate change and procedures to minimise climate-related threats. Banks should review factors such as the client’s progress towards decarbonisation, use of renewable-energy sources and production plans.

Banks can use advanced technology such as big data in the risk assessment process; some create shadow rating systems that report climate-related default probabilities alongside typical default probabilities and adopt mitigation efforts in the event of a discrepancy.

Collateral management and hedging

The next step that requires increased focus is collateral management and hedging. Both physical and transition risk could affect collateral value. Due to being an emerging market and incompetent market participants, banks have limited opportunities to transfer climate risks. Furthermore, limited data on carbon intensity and difficulties in modelling the indirect impact of climate change, such as supply-chain disruptions, could make it challenging to develop hedging strategies.

Portfolio monitoring and management

Ongoing monitoring and management of credit portfolios require banks to develop new methodologies to assess the quantitative effects of climate risk on default probabilities and expected losses. To support this, scenario analysis could be conducted in two ways. The top-down approach starts with analysing the fundamental impact of climate scenarios on financial statements, while the bottom-up module combines forecasts to generate scenario-adjusted financial statements at the individual counterparty level. Client engagement in net-zero transition plans can also be considered during this stage. Banks need to evaluate how climate risk affects the creditworthiness of borrowers and incorporate climate risks into their portfolio management.

Finally, banks should closely monitor whether clients adhere to sustainability-linked covenants since a borrower’s lapse in transition and resilience strategies could have adverse implications for a bank’s climate-related commitments and debt recovery.

Default management

Another significant area where banks may need to adjust due to climate risks is default management. First, banks should examine the root causes of defaults and determine whether climate was a factor. They should integrate information on delayed and defaulted payments due to climate change into their assessment of credit risk. They should also consider how defaults at other institutions may trigger subsequent losses, affecting their balance sheets due to the interconnectedness of the financial system.

Reporting and disclosure

Regulators, investors and other stakeholders are demanding more comprehensive and prompt disclosures concerning businesses' climate-related risks and opportunities. Although there is no universally accepted framework for corporates’ climate-related reporting in the private sector, there are a few established standard-setting bodies such as the Sustainability Accounting Standards Board (SASB), the Global Reporting Initiative (GRI), the TCFD and the Science Based Targets initiative (SBTi).

The following are recognised as important developments in the regulatory landscape:

-

Corporate Sustainability Reporting Directive (CSRD): The CSRD is a European Union (EU) law that came into force in 2023. It mandates that EU companies disclose their environmental and social effects, as well as how their actions in these areas, along with governance, impact their business.

-

UK Transition Plan Taskforce (TPT): The TPT Disclosure Framework was initiated by HM Treasury in 2022. It enables companies to make significant progress in developing and executing their strategies to achieve net-zero targets.

-

US Securities and Exchange Commission (SEC) requirements: In 2024, the SEC introduced regulations on climate disclosure, supplementing regulations such as the CSRD and California's disclosure mandates. These regulations compel companies to disclose details about climate-related risks that could significantly affect their business or financial statements.

How Acuity Knowledge Partners can help

We keep our banking clients updated on the latest climate change-related trends and standards across sectors and help them assess whether a borrower’s climate change-related targets align with these. We also assess how these targets can be linked to facilitate offering sustainable finance products to potential borrowers. Through sustainable finance analysis and assessments, we suggest how borrowers need to set their climate change-related KPIs in line with current trends and standards by proposing suitable potential KPIs and monitoring them periodically. We also manage multiple databases in terms of a number of ESG-related aspects including client transition and impact monitoring.Banking outsourcing services

Sources:

-

https://www.banktrack.org/ourproject/tracking_the_net_zero_banking_alliance

-

https://www.msci.com/www/blog-posts/how-climate-change-could-impact/02803746523

-

Integrating climate risk into credit risk modelling (reply.com)

Tags:

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Chamini is an Analyst in the Commercial Lending vertical at Acuity Knowledge Partners since 2022. At present, she is a part of the Sustainable Finance Team and is responsible for preparing pitch decks, performing checks on the sustainability of the deals, as well as managing a database for sustainable finance deals. Prior joining Acuity, she worked as a research intern at Uzabase Inc. She holds a bachelor's in Finance (Special) from University of Sri Jayawardenepura, passed Finalist of Chartered Institute of Management Accountants (CIMA) and Reading for Chartered Financial Analyst (CFA).

Blog

Blog

Are Indian equities nearing saturation point?....

The Indian equity market has seen a notable rise in recent years, fuelled by a confluence ....Read More

Blog

Blog

Sustainable finance – regulations and trends 2....

Introduction Sustainable finance has become a critical theme internationally to pave th....Read More

Blog

Blog

Navigating the green highway: sustainable tra

The global transport sector accounts for the second-highest GHG emissions The global tra....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox