Published on September 21, 2022 by Sridhar Shivaram

Amid weak global economic conditions and higher demand for safe haven assets, high-yield (HY) debt issuers have become increasingly cautious when it comes to market participation. Of late, issuers in the HY category have either tightened control on deals or switched to other means of financing after struggling to gain investor confidence in a muted primary market.

HY debt papers come with high interest rates, as these issuers pose greater risk of default given that the entities categorised as HY are either highly levered or financially distressed. This category of issuers could also include smaller or emerging ones, which may need to raise funds via HY bonds to offset their unproven operating histories or serve their business trajectories that might be speculative or risky. As a result, the yield on such instruments is typically higher to bring in investors and compensate them for the degree of risk they take on. Investors with greater risk tolerance find these debt papers attractive, particularly in low interest rate environments. From a credit rating perspective, Moody’s rates these bonds as Ba1 or below, and S&P and Fitch rate them as BB+ or lower. In the financial markets, these bonds are also known as junk bonds or speculative-grade bonds.

Given the ongoing uncertainty and rate hikes, issuers or borrowers are now cautious about engaging in the HY market. US HY deals, for instance, did not gain traction during the first week of May 2022, and the ones that supposedly had the timelines in place eventually got withdrawn. Moreover, HY investors have been shying away from the market lately, observing that preliminary and actual corporate earnings are showing declines, particularly adjusted EBITDA and sales. Rating agencies have also remained guarded, assessing that issuers may be highly levered.

In May 2022, Bioventus, a US-based pharma player, struggled to place its proposed senior notes offering in the primary market; the planned issuance was intended to finance its acquisition of CartiHeal, a pharmaceutical entity headquartered in Israel – Bioventus’s third acquisition since 2021. The USD415m five-year non-call senior notes issuance was set to hit the market at a high cost, with an initial price talk range of 9.75-10%, remaining way above the average effective yield of 6.96% on the ICE BofA US HY index. However, considering unfavourable investor feedback and current market conditions, the company decided to explore alternative financing options for the acquisition.

HY bond losses have also accelerated after mixed signals from the Federal Open Market Committee (FOMC), causing uncertainty over the number of rate hikes in the coming months and their repercussions on economic growth. Primary markets witnessed some issuers charging towards taking advantage of this risk-on mood prior to the commencement of the Jackson Hole Symposium – at which the Federal Reserve’s (the Fed’s) chairman Jerome Powell eventually delivered hawkish comments.

HY investors reclaim negotiating power

Amid this current market scenario, HY investors have been able to put pressure on issuers to make certain amendments in debt covenants as they became cognisant of issuers’ growing need to raise new debt from the market. After years of erosion seen in bond documentation, the current poor market environment has given investors the upper hand in negotiating debt covenants, although some still overlook the aggressive language in the indentures as long as the transaction comes at an attractive price or yield. In addition, over a decade of extremely cheap liquidity had meant that investors had little option but to accept the never ending assertive terms in the offering documents. However, as central banks across the globe began to reverse quantitative easing to fight inflation, investors have finally realised the opportunity to demand greater covenant security and rein in some of the exceptional amount of freedom given to borrowers in recent years.

To define covenants, these are a set of rules and terms mutually agreed by all parties involved in a deal; on the basis of these, limits and constraints are set in raising finance via different asset classes. Covenant documentation signifies a binding relationship between an investor and issuer. The agreements can permit or put a constraint on an activity during a particular transaction. Certain binding clauses, when breached, may trigger a compensatory or legal action. Covenants could be both negative and positive/affirmative. Negative covenants often refrain issuers from actions that could lead to a deterioration in their credit reputation or ability to repay existing debt. Common examples could be dividend declaration, restrictions on management fee from related parties etc. On the other hand, positive or affirmative covenants allow the issuer to perform certain actions. These commonly include maintaining adequate levels of leverage, ensuring compliance with applicable regulations and maintenance of credit rating and proper accounting books. A breach of positive covenants may lead to an outright default.

The market’s moderate risk appetite has enabled investors to curb issuers’ movements, forcing underwriters and entities to agree upon restrictions that lend strength to investors’ interest payment prospects. In a recent case, 888 Holdings, an issuer belonging to the casino and gambling industry, was made to amend some of the terms in its debt indenture. The debt comprised a EUR400m, 7.558% senior secured five-year bond non-callable for two years (5NC2) and a EUR300m senior secured 6NC1 floating rate note. The agreement initially contained an aggressive covenant package that permitted the entity to exclude material amounts of debt from its key ratios, which would have changed the direction of covenant calculations in its favour. One amendment involved the reduction of the leverage ratio from 4.0x initially to 3.5x, and the corresponding part of the acquisition financing was also similarly reduced. The company was also forced to cut out other unusual provisions that would have allowed it to increase debt levels beyond permitted thresholds. Eventually, the two tranches of 888 Holdings’ bond offering was priced at a discount of c.85, lower than initially estimated.

Instances such as this also serve to show that investors are generally inclined towards the price of a security and favour good companies with poor covenants rather than bad ones with good covenants. In the case of 888 Holdings, for instance, investors were willing to participate in the issuance given the company’s financial strength and, particularly, the yield of 11.5%.

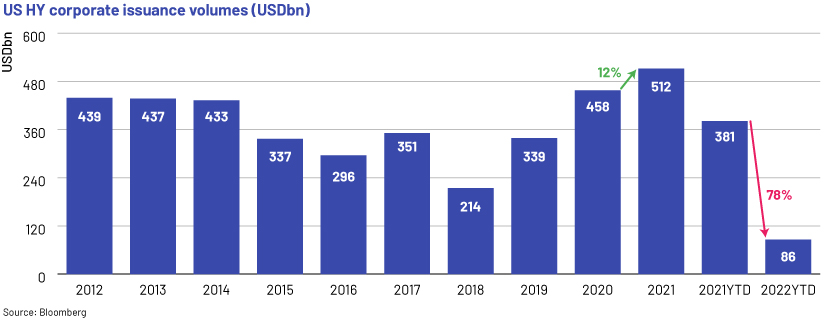

HY debt markets have rarely seen deals with document rewrites when compared with the loan market, which is not a surprise, as loan markets have actively been creating such instances. That said, such covenant modifications could grow in number in debt markets, as issuers have been desperately seeking sources to raise funds amid the current hostile market conditions, ultimately giving HY investors the upper hand over companies. As of YTD 2022, US HY corporate debt issuance volumes amounted to USD86bn, 78% lower than the same period in 2021, amid rate hikes and central banks’ measures to reduce stimulus, which have turned the tables for market participants as borrowing costs have surged.

Battered HY bond market – the road ahead

The HY market remains challenging and dysfunctional as companies with higher-risk profiles have had to put a hold on raising funds from debt markets and explore other alternatives as borrowing costs surge and investors ready for an economic slowdown. HY refinancing bond deals could also be negligible in the near term. Investors could continue to force HY issuers to modify covenants and mould these agreements to their benefit. That said, despite inadequate supply, the primary market will welcome high-quality issuers raising via secured paper, offering strong covenants and healthy recovery prospects at a single-digit yield.

In addition, the recent rally driven by comments from the Fed has improved investor sentiment, turning it towards HY funds for the first time in two months, providing relief to fund managers who were hit hard by the outflow seen this year. The Fed, in its July 2022 meeting, raised the interest rate by 75bps for the second month but at the same time indicated that the pace of hikes might slow down in the coming meetings, propelling a rally in risk assets, including HY bonds. The markets could see a turnaround after inflation starts nearing the Fed’s 2% target, which would slow the pace of further tightening and provide room for investors to participate in HY debt markets.

How Acuity Knowledge Partners can help

Acuity Knowledge Partners is a leading provider of high-value research, analytics and business intelligence to the financial services sector. We support over 440 financial institutions and consulting companies through our specialist workforce of over 4,250 analysts and delivery experts across our global delivery network. We provide bespoke support to the debt capital market (DCM) teams of investment banks and advisory firms across the world through a wide range of solutions for corporate DCM, financial institutions group (FIG) DCM, sovereign, supranational and agencies (SSA) DCM, sustainable DCM and HY teams. Our team of experts regularly tracks macroeconomic factors affecting markets and provides end-to-end support, from deal origination to execution, including the most intricate financial analysis and aftermarket support. The DCM team also provides assistance with covenant analysis on different types of debt products by actively monitoring and capturing the covenants being incorporated by issuers in the offering circular, interpreting the ultimate purpose of the investments and how far they will benefit investors, and helping issuers raise funds.

Sources:

https://www.bioventus.com/bioventus-completes-cartiheal-acquisition/

https://www.cnbc.com/2022/08/12/investors-are-piling-into-junk-bonds-what-to-know-before

https://www.reuters.com/markets/us/us-high-yield-bond-funds-draw-cash-recession-fears-ebb

https://digitalcommons.uri.edu/cgi/viewcontent.cgi?article=1348&context=oa_diss

https://www.federalreserve.gov/newsevents/pressreleases.htm

https://www.dbs.com.hk/treasures-private-client/investments/product-suite/fixed-income/

https://www.managementstudyguide.com/high-yield-bonds.htm

https://www.sifma.org/resources/research/us-treasury-securities-statistics/

Tags:

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Sridhar has been working with Acuity’s Global Capital Markets (GCM) team for over 4 years. He is currently supporting the GCM team of a major European investment bank and has demonstrated his proficiency in comprehending the Investment Grade and High Yield bond markets across the United States, Asia and EMEA. Prior to joining Acuity, Sridhar was working with an Indian mid-size investment bank where he was responsible for providing assistance to Investment Advisory and DCM Origination and Sales teams in their fund raising initiatives. Sridhar holds a Post Graduate Diploma in Management, specializing in Finance from New Delhi Institute of Management. He is also passionate about the equity markets,..Show More

Blog

Blog

Interest Rate Divergence in 2024: A Global Conte....

Interest rates are diverging sharply in major economies, most notably in the US and the Eu....Read More

Blog

Blog

Drowning hopes of lower Treasury yields amid the....

The US Treasury market is in a precarious situation as dwindling demand from traditi....Read More

Blog

Blog

Driving the success of compliance functions: Acu....

In the fast-paced and highly regulated world of finance, compliance is not just a necessit....Read More

Blog

Blog

A dovish Federal Reserve: a ray of hope for c

Rate cuts – a strategy for risk management The US Federal Reserve’s (Fed’s) Decembe....Read More

Blog

Blog

The Federal Reserve’s trajectory – side-t

The bank run that resulted in the collapse of Silicon Valley Bank (SVB) derailed the US fi....Read More

Blog

Blog

The impact of rising interest rates on bond m

The pandemic delivered the most severe blow to the global economy since the Great Depressi....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox