Published on February 17, 2021 by

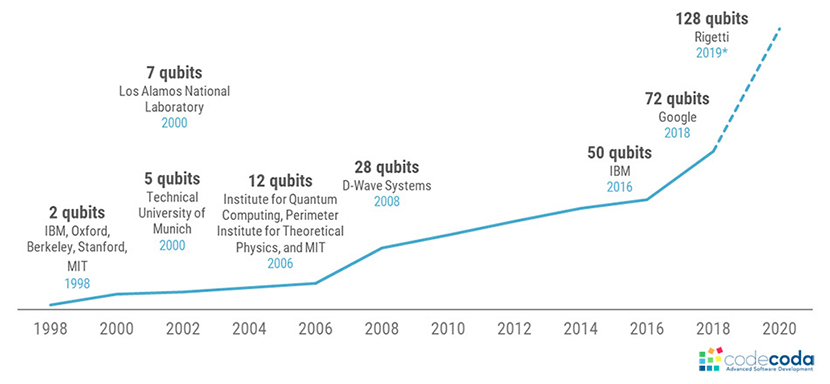

As the world trudges forward amid the “new normal”, the fourth industrial revolution is beginning to evoke its importance as the vital force across sectors and industries. Like artificial intelligence (AI), robotic process automation (RPA) and blockchain technology, quantum computing is a concept that has created interest across multiple sectors. Quantum computing has evolved significantly in terms of capacity and processing power, especially from 1998 to 2020 (see chart below).

Source:https://codecoda.com/en/blog/entry/understanding-quantum-computing (2020)

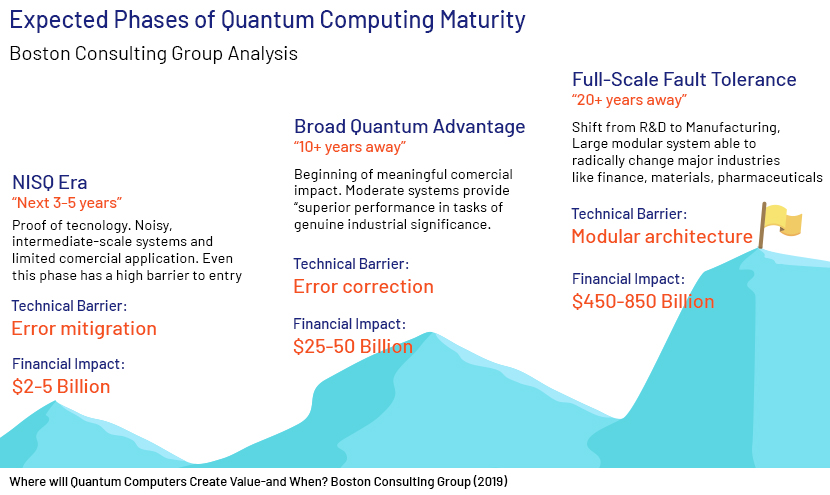

The hardware requirements of quantum computing could limit its application in the short term. However, growth in cloud computing would accelerate adoption of quantum computing by a wide range of users and facilitate the seamless flow of the phases highlighted in the diagram, while the lower costs of adoption would enable institutions to obtain prompt results in a financially positive manner.

Source:https://www.zdnet.com/article/ionq-ceo-peter-chapman-on-quantum-computing-adoption-innovation-and-whats-next/ (2020)

Classical computers vs quantum computers

The classical computers that most use process data using bits (sequences of 0’s and 1’s). These bits can only be 0 or 1 at any given time. In contrast, quantum computing uses quantum bits (qubits) that could be 0,1 or both 0 and 1 in simultaneous positions (using a process named superposition). Hence, innumerable calculations can be carried out instantaneously. In addition, quantum computing uses a process called entanglement that enables the quantum particles to be correlated and linked. This indicates that when the condition of one qubit is altered, the condition of another qubit will change immediately. Both these concepts allow quantum computing to produce the expected results quickly and process large quantities of data.

However, classical computers would still be useful for performing basic tasks in the near term (three to five years), especially within the Noisy Intermediate Scale Quantum (NISQ) devices era, according to the diagram above, as quantum computing evolves. Quantum computing capabilities in the near term could be prone to high error rates; hence, it is vital that a hybrid approach involving classical computers be followed in the short run.

Lending challenges associated with the use of classical computers

The many issues with customer onboarding processes, such as timeliness and data processing capacity, are exacerbated by the current computer systems and capabilities. Onboarding processes take a total of 12 weeks in certain situations and around 34 weeks in others (for manual onboarding), according to research by Forrester and Fenergo. This could be detrimental considering the competition, especially from fintech companies (such as Atom and Volt Bank) that are constantly expanding their service portfolios.

Siloed systems and an unclear structure duplicate information across the many departments that customers interact with during the onboarding process. Moreover, rapidly evolving

regulations pose difficulties for banks trying to amend their onboarding processes. The need to compile a number of documents and the myriad data clusters, along with the unique requirements of customers, necessitate quick and insightful analysis.

The massive datasets banks process during a lending procedure require high computing power; the classical systems fail to compute such large datasets from time to time, resulting in costly delays. This further highlights the importance of quantum computing.

How banks can benefit from transitioning to the use of quantum computing

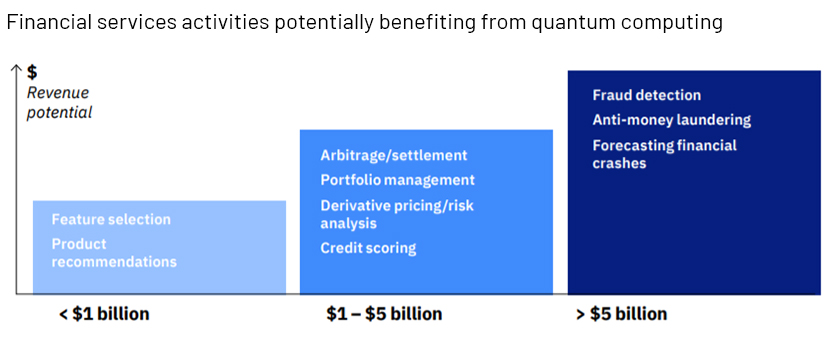

Source:https://www.ibm.com/downloads/cas/2YPRZPB3 (2019)

-

-

AI and RPA, in conjunction with quantum computing, would enable loan applications to be processed quickly (as they facilitate a smooth loan-origination process), while the inclusion of pre-programmed rules could enable automated approval of mortgages and different loan facilities. Customised products could also be recommended (in line with the chart above), minimising customer dissatisfaction. Standard Chartered Bank, for example, is exploring several use cases (such as risk management) while understanding the importance of developing new financial products with assistance from this technology.

-

Credit scoring is a major function of the credit underwriting process, and in the current pandemic scenario, keeping track of changes to credit scoring has become vital. Quantum computing can facilitate this, as it enables a multitude of inputs to be incorporated into a risk-rating model, providing a more insightful risk assessment of client portfolios. BBVA has been working with Accenture and startups such as Multiverse to optimise credit scoring processes, translating into greater accuracy and benefits (as outlined in the chart above). CaixaBank is testing the technology in different banking scenarios while using a hybrid approach with classical computing for risk classification.

-

A Fenergo survey in 2019 estimated that banks and financial institutions lose USD10bn- 40bn in revenue a year owing to fraud-related activity and inefficient data management procedures. The data-modelling capacity of quantum computers would enable finding complex patterns within large datasets, facilitating making proactive predictions pertaining to fraud management (as the chart above shows). Moreover, banks could utilise distributed ledger technologies with strong quantum computing capabilities to enable a more secure and faster KYC process. ABN Amro Bank, for example, is exploring the use of quantum computing in securing online banking, and HSBC has joined the European Next Applications of Quantum Computing (NEASQC) project with the aim of identifying use cases, including security.

-

Quantum computing is an advanced solution to many banking dilemmas, but the poor encryption procedures currently available and unauthorised access to quantum computers could cause costly data breaches not faced previously. Hence, its application should be more thoroughly researched. Financial services firms and banks could partner with like-minded institutions and application developers in the near term to understand how such problems can be mitigated and how the greater potential of this technology can be tapped. This would give first movers a significant competitive advantage as quantum computing evolves.

Sources:

-

https://codecoda.com/en/blog/entry/understanding-quantum-computing

-

https://www.fintechfutures.com/2018/09/the-future-of-client-onboarding/

-

https://sbi.co.in/documents/2182813/4777159/Quantum+Computing+in+Banking_Indian.pdf

-

https://www.hsbc.com/who-we-are/hsbc-news/exploring-the-power-of-quantum-computing

-

https://www.bcg.com/publications/2020/how-financial-institutions-can-utilize-quantum-computing

-

https://ibsintelligence.com/blog/quantum-computing-the-next-frontier/

-

https://www.boldbusiness.com/digital/quantum-computing-banking/

-

https://uwaterloo.ca/institute-for-quantum-computing/quantum-computing-101

-

https://internationalbanker.com/technology/responding-to-technology-disruption-in-wholesale-banking/

-

https://www.computerweekly.com/news/252486296/BBVA-explores-quantum-computing-for-banking

-

https://news.mit.edu/2021/william-oliver-quantum-computing-0119

-

https://www.bcg.com/publications/2019/quantum-computers-create-value-when

-

https://www.finextra.com/newsarticle/36686/hsbc-joins-european-quantum-consortium

-

ABN Amro explores the security applications of quantum technology (2019).

What's your view?

Thank you for sharing your Comments

Share this on

Blog

Blog

Bright spots in distressed debt investing amid r....

Key takeaways: The macro economy began deteriorating during 2022 in the form of l....Read More

Blog

Blog

A new dawn for fixed income assets following an ....

After a dismal 2022, fixed income investors have a lot to look forward to in 2023, a....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox