Published on January 19, 2023 by Binwei LV

1. The need for electric vehicles

Carbon neutrality has become a global consensus and entered a period of accelerated development. A significant amount of evidence and a number of studies show that since the Industrial Revolution, greenhouse gas emissions, mainly carbon dioxide, have caused global warming, and a series of adverse factors such as extreme weather, natural disasters and military conflict in the process of human industrialisation seriously affect our survival. Reducing greenhouse gas emissions is now the responsibility of all countries.

China has established a high-standard carbon peaking and carbon neutrality leading group and is building a 1+N policy system. The EU has pledged to reduce greenhouse gas emissions by 55% compared with 1990 levels by the end of 2030, and has released a package of plans involving energy for a number of sectors such as transport, manufacturing, aviation, shipping and agriculture. Carbon emissions of the automobile sector, for example, should be reduced by 100% by 2035, achieving zero emissions. The US has announced its return to the Paris Agreement and has proposed that the share of zero-emission vehicles will reach 50% in 2030.

Countries that currently account for 75% of global GDP and 65% of global carbon emissions have announced carbon neutrality goals. From the perspective of energy structure transformation, the world's major economies are trying to build an electric economic chain – developing photovoltaic on the supply side, wind power and electric vehicles on the demand side, and energy storage on the storage side. In efforts to limit the global temperature increase to 1.5°C, global investment in the energy and transport sectors will increase from an average of USD560bn per year to about USD2tn per year in the next 30 years, according to the International Renewable Energy Agency.

2. Growth of electric vehicles

2.1 High demand has led to significant expansion of the sector

Under the "unification of electric power" standards, electrification of the transport sector has become the main way in which to save energy and reduce emissions. The power battery is the core link of the electric-vehicle sector and is about to enter the terawatt-hours (Twh) era. Global power battery technology keeps innovating, balancing and optimising cost, energy density, low temperature performance, cycle life and other aspects, constantly improving volume utilisation and optimising vehicle performance. Global technological innovation accelerates industrial development, provides high-quality supply and accelerates global electrification penetration.

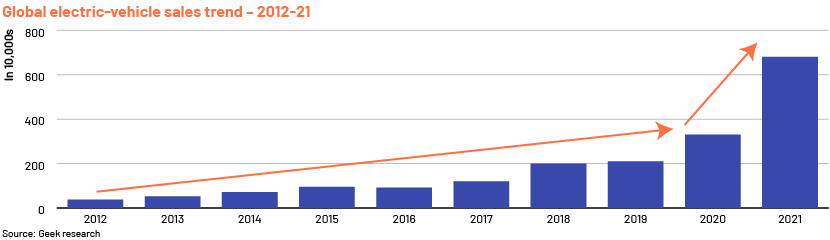

Demand for electric vehicles has grown rapidly since the second half of 2020, and the price of the industry chain has risen sharply amid the supply-demand mismatch.

2.2 The price increase in the industry chain has raised concern about demand

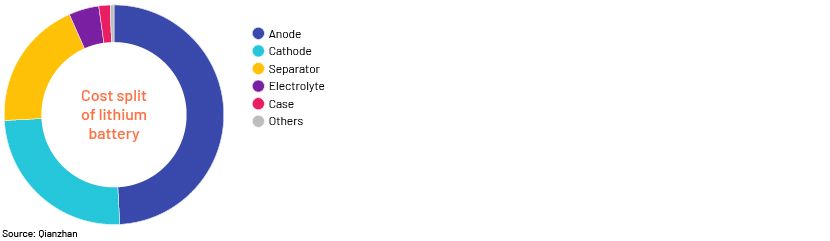

From July 2020 to the end of 2021, single-ton prices of lithium carbonate, cobalt sulphate, nickel sulphate and manganese sulphate – raw materials of the electric-vehicle industry chain – rose by 587.5%, 123.0%, 53.8% and 78.6%, respectively. The price of the battery link has increased significantly, with the greatest impact on anode material. The price of raw material in the anode industry chain represented by lithium carbonate is still expected to remain high, and the anode is still the part that has the greatest impact on costs.

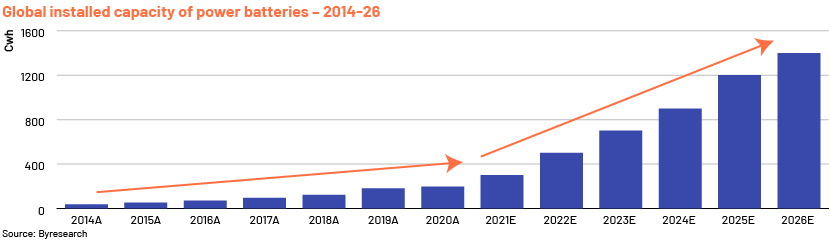

Demand for downstream electric vehicles has increased demand for power batteries. In 2021, the global installed capacity of power batteries was 296.8Gwh, a y/y increase of 88.7%, having grown at a CAGR of 31.8% from 2014. We predict a CAGR of 30.1% over 2022-26, and the global power battery to enter the Twh era by 2025.

High prices in the industrial chain represented by anode material have raised concerns about demand. With the gradual increase in the price of the industry chain, battery companies have successively passed on prices, and vehicle companies had gradually increased prices by the end of 2021. After the price increases of vehicle companies at the end of 2021 and early 2022, prices have increased significantly since March 2022. Tesla has raised the prices of some domestic Model 3 and Model Y vehicles three times in a row; the price increase by Xiaopeng Motors ranges from RMB10,100 to RMB20,000; Li Auto raised the price of the Ideal ONE by RMB11,800. BYD and other car companies have also increased their prices. The rise in the terminal price of electric vehicles has raised market concern about the pace of demand growth. The key driver of battery prices is market perception of development of the anode industry chain.

3.Demand for raw materials – the importance of anode

3.1 Continuous iteration of anode material technology

Anode material is an important part of the lithium-ion battery and accounts for most of the cost of the lithium-ion battery. Its performance directly affects the energy density, safety, cycle life and other core performance indicators. Mainstream anodes mainly include lithium cobalt oxide (LCO), lithium manganate (LMO), lithium iron phosphate (LFP) and ternary anode materials (NCM and NCA).

3.2 High nickelisation improves energy density

The technical upgrade of ternary anode materials is mainly in two directions: (1) The improvement of energy density, according to the formula W = QU (W refers to energy density, Q refers to nickel and U refers to voltage), has evolved in two major directions – one is in improving the content of nickel and the other is in boosting voltage (U). (2) The improvement of stability, cyclability, safety, etc., which mainly includes technologies such as doping, coating and monocrystalline silicon.

The high nickelisation of anode materials is significant. Cobalt stabilises the layered structure of the material, and improves the cycle and rate of performance; the price of cobalt is volatile. Manganese has good electrochemical inertness, which plays a role in reducing material cost and improving material safety and structural stability. Nickel is an important active material; increasing the ratio of nickel doping can improve the energy density of the anode material. High nickelisation refers to increasing the content of nickel in the ternary material, thereby increasing energy density and reducing the cost of raw materials by reducing the amount of cobalt required.

3.3 Nickel resources determine the dominance of the electric-vehicle industrial chain

Taking the nickel component in the power battery as the main classification method, it mainly includes the 6-series and 8-series ternary lithium batteries, and even the 9-series ternary lithium battery, which is under research. It has broad application prospects in medium-range and high-end new-energy passenger vehicles. Under the premise of solving safety problems in the future, the energy density of power batteries for medium-range and high-end passenger vehicles will likely see a qualitative leap. The advantages of higher energy density will drive overall cost close to that of lithium-iron phosphate batteries even when the unit cost price is higher. The world's major power battery manufacturers are actively conducting nickel battery research and development.

High-nickel technology has the significant advantage of high energy density. As to whether the application of high-nickel ternary will be accelerated in the future, we believe the answer should be found from the current application of ternary battery: (1) In terms of high-nickel technology, the technical reserves of enterprises are relatively low, and the safety and stability of materials are not easy to ensure. In terms of inherent properties, with the increase of nickel content, the thermal stability of the system becomes worse. (2) Modification of the physical structure of high-nickel ternary batteries has not been widely popularised. (3) Different market regions select different technical routes.

4. Conclusion

The application of high-nickel technology is being gradually popularised. In addition to the research and development of high-nickel batteries, some listed companies are studying the storage and application of high-nickel technology. High-nickel ternary is commonly used by leading power battery companies. Rongbai Technology, Long-term Lithium Technology and Dangsheng Technology have all formed a 10,000-ton level. Shipping with the required technical conditions for large-scale application, CATL, LG Chem and SKI have all delivered 811 batteries in batches, and Samsung SDI has begun planning to produce power batteries with a nickel content of 88%.

There is still much room for improvement in the ternary anode material system. The battery sector is essentially a technology-driven one, and technology presents both the biggest opportunity and the biggest risk. Industrialisation of anode materials for sodium-ion batteries has just started, and industrialisation of lithium-rich manganese-based batteries would take time. Ternary materials are still needed in the era of solid-state batteries.

How Acuity Knowledge Partners can help

We have in-depth knowledge of China’s anode material sector. We provide end-to-end support to funds on investment, including but not limited to identifying high-value new-energy and battery enterprises, in-depth new-energy vehicle sector research, pre-investment opportunity evaluation and post-investment value-added strategy. We have new-energy sector research teams that focus on China to help our clients capitalise on investment and M&A opportunities in the country.

References:

-

Datayes: https://r.datayes.com/

-

Byresearch: https://baijiahao.baidu.com/s?id=1748904351854223904&wfr=spider&for=pc

-

Qianzhan: https://bg.qianzhan.com/report/detail/300/200410-57cece20.html

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Binwei LV has 1 year of experience in private equity investment analysis with a focus on China market. In her current role at Acuity Knowledge Partners, Binwei supports both pre-investment research and post-investment management for a large Asia private equity fund, covering a wide spectrum of industries such as clean energy. Binwei holds a master degree in Corporate Finance from Queen Mary University of London.

Blog

Blog

EV public charging infrastructure – a bottlene....

A recent survey by McKinsey revealed that 29% of EV owners globally are looking to switch ....Read More

Blog

Blog

Major technological trends in the electric trans....

Technological advancements in the electric transport market are crucial for improving batt....Read More

Blog

Blog

How electric vehicles threaten the ESG ecosystem....

According to the International Energy Agency (IEA), 10.3m electric vehicles (EVs) were sol....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox