Published on January 29, 2021 by Hitesh Acharya

Banks and financial institutions have developed two types of loans – green loans and sustainability-linked loans (SLLs) – in response to the constant pressure from stakeholders to address environmental, social and governance (ESG) and sustainability issues. While proceeds from green loans must be used towards an environmentally friendly project or purpose, proceeds from SLLs may be used for any purpose – green or otherwise. SLLs have an inbuilt pricing mechanism that makes their pricing cheaper, subject to the achievement of ESG targets (called key performance indicators, or KPIs) decided by the borrower. Other components of sustainable debt, not covered in this blog, are public instruments such as green bonds, social bonds and sustainability bonds.

SLLs are a relatively new concept, but their volumes have been increasing constantly – lenders issued USD122bn worth of SLLs globally in 2019, a 168% increase y/y, due to the benefits accruing to borrowers such as lower costs of borrowing, a stronger corporate reputation and compliance with ever-increasing government regulations on sustainability. For lenders, SLLs provide a chance to expand their portfolios, while improving their sustainability credentials. However, after registering strong growth in the first quarter of 2020, SLL volumes declined 15% for the full year due to the impact of the pandemic on the global economy

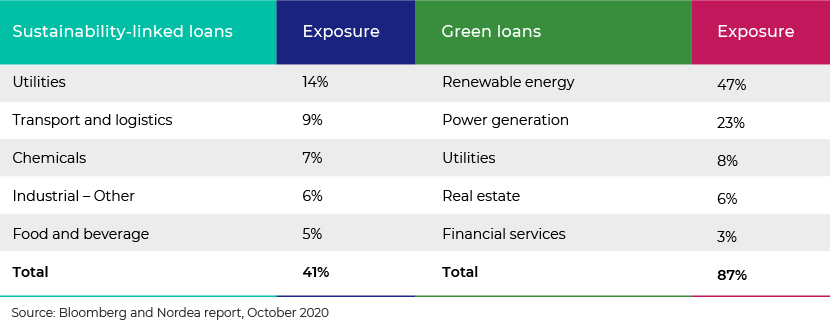

Unlike green loans, SLLs provide the flexibility to use the end proceeds for any general corporate purpose. SLLs are, therefore, available for a number of sectors, whereas green loans are mainly concentrated among a few sectors with clearly defined “green” assets, such as renewable energy and utilities. The following table provides a breakdown of exposure to SLLs and green loans of the top five sectors:

SLLs used to be structured on a “one-way” pricing basis, so that if a borrower’s ESG KPIs were met, a discount was applied to the applicable pricing. Inability to meet the set KPIs did not carry a penalty, and pricing remained unchanged in such cases. Lenders have recently been incorporating “two-way” pricing in SLL agreements where, if the borrower meets the prescribed KPIs, a discount is applied to the pricing, but if the KPIs are not met, a premium is added to the pricing and the lending cost increases. For example, Xylem Inc. was one of the earliest general industrial companies in the US to issue an SLL, with an USD800m revolving credit facility, in March 2019. Citibank, J. P. Morgan, Wells Fargo, ING Bank (also the sustainability coordinator) and BNP Paribus were the arrangers and book runners. Pricing was set at LIBOR + 110bps, which would vary by +/- 5bps depending on Xylem meeting the prescribed ESG KPIs. While the two-way pricing has raised concern about the lender benefitting from the borrower’s failure to meet its KPIs, it provides a stronger incentive for borrowers to increase their focus on sustainability. A possible solution could be to transfer the additional pricing premium paid by the borrower to a separate bank account used only to fund ESG activities.

In May 2020, a joint working group comprising the Loan Market Association (LMA), the US Loan Syndications and Trading Association, and the Asia Pacific LMA issued new guidance on the SLL Principles. The new guidance clarifies the application of the Principles. According to the guidelines, the KPIs set for borrowers must be ambitious and should not be lower than those adopted internally by a borrower. More importantly, they must be material to the borrower’s business. The guidance also recommends mapping KPIs against the most important ESG factors for a borrower within a given industry. Reference points for setting KPIs can include models such as the Sustainability Accounting Standards Board’s Materiality Map, which is an assessment of more than 40 ESG issues, ranked in order of priority, based on the industry that the borrower operates in. A loan may have more than one KPI to measure its progress.

KPIs can be general across industries, for instance, reduction of a certain amount of CO2 emissions per year, or they can be customised in line with the borrower’s operating model. For example, in the case of a real estate project, a KPI set by the lender could be obtaining a gold or platinum Leadership in Energy and Environmental Design (LEED) certification for a building to be constructed. For energy-intensive manufacturing units, the KPI may be for a certain percentage of the unit’s energy requirements to be sourced from renewable energy sources. For a food products manufacturer, it could be the proportion of raw materials sourced on an ethical and sustainable basis.

The SLL guidance mentions that borrowers should provide details of their KPIs to the lenders at least once a year. Borrowers should ideally provide particulars of the underlying methodology and assumptions used in the measurement of KPIs. The requirement for external review of whether the KPIs have been met should be determined on a case-by-case basis. For publicly listed companies, public disclosures may be deemed to be sufficient to assess ESG performance for the purposes of the SLL agreement.

How Acuity Knowledge Partners can help

Acuity Knowledge Partners has more than a decade’s experience in supporting financial institutions with designing and structuring their ESG frameworks. Our ESG experts can guide banks in setting up the pricing matrix for SLLs and monitoring the compliance of such SLL borrowers with the prescribed ESG KPIs, in line with a bank’s credit policy.

Sources:

-

Asia Pacific Loan Market Association – Green Loan Principles report

-

Bloomberg New Energy Finance report

-

Bloomberg and Nordea report

-

Reuters

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Hitesh has over 14 years of experience in working with leading global organizations in the banking and commercial lending domains. His expertise spans a broad range of analyses, including credit appraisal, leveraged lending, stressed assets, industry reports, cash flow modelling, and client pitch presentations. At Acuity Knowledge Partners, he has led sector and product-specialist pilot teams in Commercial Lending, focusing on diverse sectors such as real estate, manufacturing, aerospace and defense, transport and logistics, and business services.

Hitesh holds a Masters in Management Studies from K.J. Somaiya Institute of Management Studies and Research, University of Mumbai, and a B.Com from University of Mumbai.

Blog

Blog

ESG investing – beginner’s guide to responsi....

ESG investing in private markets integrates environmental, social and governance (ESG) att....Read More

Blog

Blog

Role of Technology in ESG Data and Reporting....

In recent times, environmental, social and governance (ESG) reporting has evolved from a p....Read More

Blog

Blog

Green steel manufacturing: a start to a greener ....

Introduction Steel has been one of the most important components in the construction of m....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox