Published on June 24, 2025 by Mohammad Seraj

Conventional datacentres rely mainly on fossil fuels and inefficient cooling systems. This results in direct and indirect emissions, including fuel combustion, chemical reactions, excessive electricity consumption and supply-chain emissions associated with the manufacturing, transport and disposal of equipment. These direct and indirect emissions are responsible for c.2% of global greenhouse gas emissions. Datacentres now account for c.3% of global electricity consumption.

Demand for datacentre infrastructure is growing, and companies are focusing on cost-efficient alternatives to balance their business need and sustainability goals. The best solution for both requirements is migrating to green data centers.

A green data center, also known as a sustainable datacentre, is a facility designed to minimise carbon footprint and emissions and ensure better overall energy consumption by deploying renewable energy sources, advanced cooling systems and transformed infrastructure designs for energy optimisation.

Deploying key metrics such as power usage effectiveness, carbon usage effectiveness and water usage effectiveness for measuring efficiency of green data centers is crucial for identifying areas of improvement and ensuring sustainability goals.

1. Power usage effectiveness (PUE): Measures total power consumption of a datacentre relative to the power consumed by its IT equipment only. A lower PUE value indicates a more energy-efficient datacentre, as it signifies that a higher proportion of the power is being used directly for computing rather than for supporting infrastructure.

The ideal PUE is 1.0, which means all energy consumed by the facility is used directly by IT equipment, with no overhead for cooling, lighting or other support systems. Globally, most datacentres have PUE values ranging from 1.5 to 2.0.

2. Carbon usage effectiveness (CUE): This focuses on the environmental impact by measuring the ratio of carbon dioxide emissions to energy consumption. The goal is to achieve the lowest possible CUE value, which indicates that the datacentre is operating in an environmentally sustainable manner.

3. Water usage effectiveness (WUE): Measures the water efficiency of the datacentre required for cooling equipment; this is expressed in litres per kilowatt-hour, indicating how much water is used per kilowatt-hour of electricity consumed.

By monitoring these metrics, datacentre operators can implement strategies to reduce energy consumption, optimise resource usage and enhance overall datacentre efficiency.

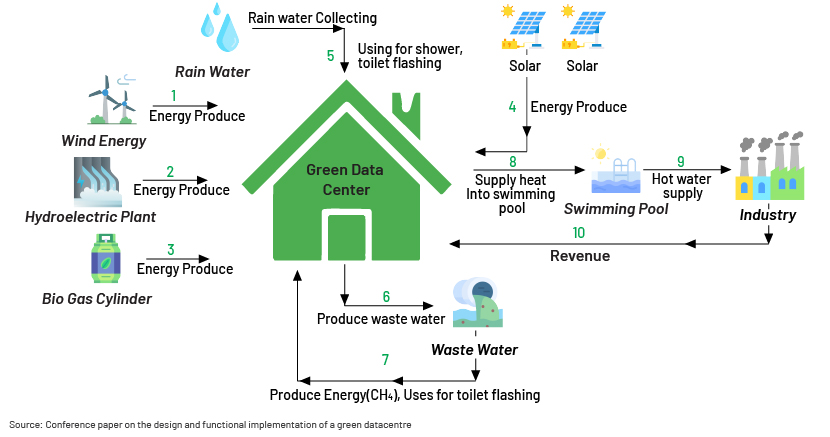

Features unique to green datacentres

Compact building design: Green data centers have compact layouts for the intake of natural light and airflow; all the infrastructure is created using eco-friendly materials.

Renewable energy procurement: Green data centers operators can procure renewable energy via multiple routes such as power purchase agreements, renewable energy credits, green tariffs and on-site microgrid systems.

Waste heat reuse: Waste heat generated by green data centers can be integrated with the district’s heating network via an insulated pipe system for reuse by commercial and residential buildings.

Wastewater reuse: An effective water-treatment strategy enables repeated use of water in a cooling system that can be recycled using cooling towers and exchangers, then recirculated in the system.

Green data centers also emphasise an asset-recovery strategy, which includes refurbishment, redeployment, resale and responsible recycling of equipment and components of datacentres.

Market structure and growth prospects across sectors and regions

The green data center market consists of the component and solution segments. The component segment includes consulting, designing, implementation and maintenance services. The solution segment further divides into cooling/HVAC systems, power systems, monitoring and management systems, and networking systems.

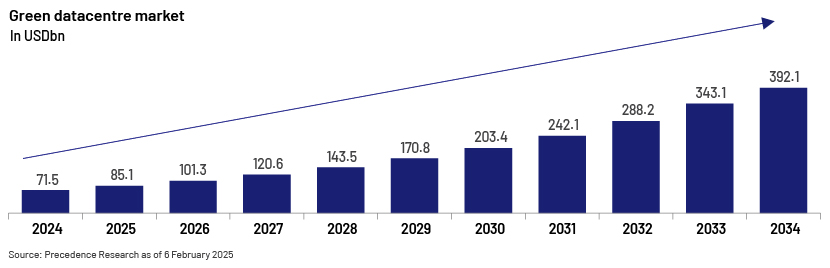

The current market is worth over USD71bn and is estimated to reach USD392bn by 2034. Cooling/HVAC systems account for a c.41% share of revenue in the current market.

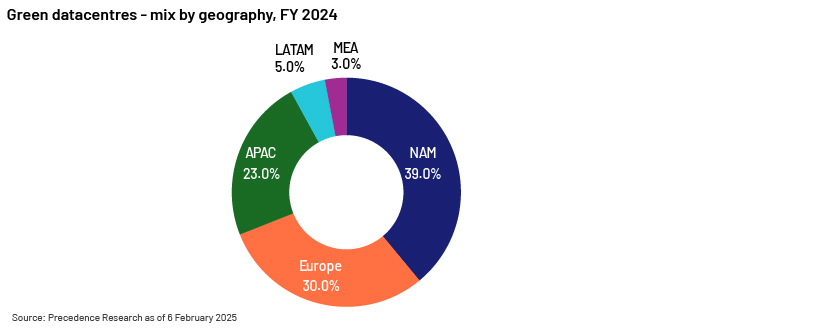

Large enterprises are early adopters of advanced cooling systems and energy-efficient technologies, accounting for c.74% of total market share. North America holds a significant c.39% market share, benefiting from technological headway, intelligent management techniques, integration of renewable energy resources, energy-efficient cooling systems, a strong financial environment and high demand for data services.

Market participants and strategies

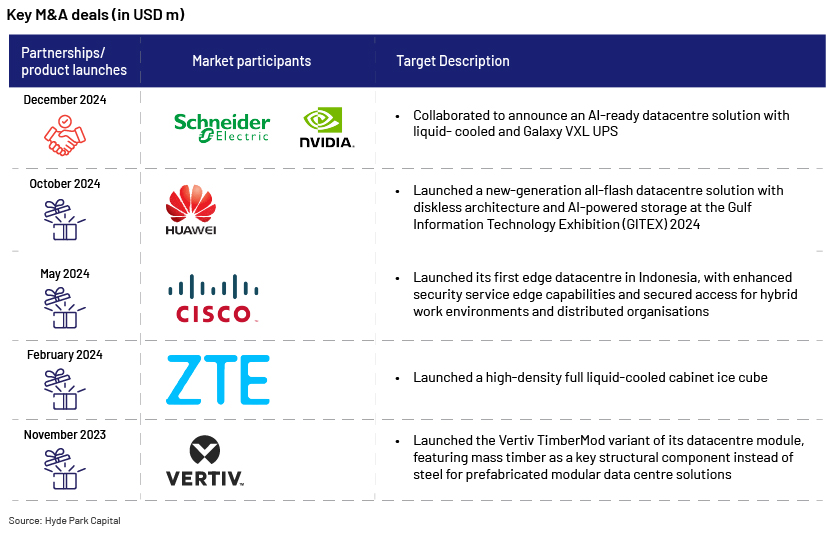

Datacentre developers and operators are focusing on new product launches and innovations as a development strategy to keep pace with end users’ changing demands and to remain competitive.

ABB Group, IBM, Eaton Corp., Hewlett Packard, Dell, NEC Corp. and Delta Electronics are some of the key innovators in this market.

Recent partnerships and product launches

Growth factors and trends

The increasing impact on the environment and a spike in energy costs have led to the adoption of energy- and cost-efficient solutions. The following factors support growth in this trend:

Digitalisation and AI technology: A surge in internet and e-commerce penetration, along with the internet of things, has amplified demand for datacentres. Current trends suggest that datacentre capacity could rise to 171-298GW annually globally over 2023-30, according to McKinsey’s analysis. Generative AI will be a key driver, expected to grow at a c.39% CAGR by 2030, resulting in AI-ready datacentres accounting for c.70% of total demand for datacentre capacity.

Regulatory trends and incentive programmes: With increased AI adoption, demand for datacentre power is expected to surge by c.160% by 2030. As a result, governments have changed their stance and become cautious due to increased power use and the environmental impact of datacentre projects. All major countries have mandated climate disclosure for companies listed on their stock exchanges. The Energy Efficiency Directive (EED), the Digital Operational Resilience Act (DORA) and the Corporate Sustainability Reporting Directive are some of the key regulations being developed and adopted in Europe.

In Asia, Japan issued its sustainability disclosure standards in March 2025; it allows a voluntary compliance period for prime listed companies for the next two years and will make disclosure mandatory from 2027. The standards will incorporate key elements of the ISSB standards. Hong Kong has also issued its final disclosure standards, effective from 1 August 2025, fully aligned with ISSB standards. Other countries such as Malaysia, South Korea and Taiwan are also developing roadmaps for reporting sustainability data.

In the US, the SEC has voluntarily stayed the adoption of its climate disclosure rule that requires companies to report greenhouse gas emissions and other climate-related information. The rule was announced in March 2024, but implementation was suspended within 10 days following multiple lawsuits by companies, US states, NGOs and climate advocates. However, local jurisdictions are developing community-focused regulations such as those limiting locations and reducing noise pollution.

Governments are also running incentive programmes and providing subsidies in the form of grants or tax breaks. Companies can obtain emission-reduction credits by transitioning to liquid immersion cooling from air. Purchasing a wind or solar generator can help them qualify for investment tax credits. Construction costs can also be covered by investment tax exemptions and credits. Companies can obtain incentives from state governments in India on land with electrical and network connections to a datacentre using 30% or more renewable energy.

Consumer preference for choosing eco-friendly products: All brands making ESG claims have consumer support, with consumers willing to pay 9.7% above the average price for sustainably produced or sourced brands, according to PwC’s Voice of the Consumer Survey 2024. Such trends are motivating businesses to adopt more sustainable practices, fuelling demand for eco-friendly resources in their operations.

Recent power purchase partnerships towards sustainable data centres

The following are some recent power purchase agreements (PPAs) between renewable power suppliers and datacentre operators.

Conclusion

Green data centers are not just a trend but a necessary step towards an eco-friendly digital world. Industries are shifting towards cost-efficient and sustainable options to meet their energy requirements. However, the transition to green data centers is facing a number of challenges, including high initial costs, lengthy processes and hurdles in integrating new technologies with existing systems.

An efficient cost-benefit analysis of such a long-term investment makes the transition feasible. A smooth transition towards such sustainable practices would also avoid greenwashing practices (where companies falsely claim they are sustainable). The authorities should enforce strict penalties for malicious activity and synchronise the tracking of the sustainability of datacentre premises.

Technology advancements such as AI-driven energy management, efficient renewable energy storage solutions and further developments in cooling technology could help overcome the technical hurdles and further drive this evolution.

How Acuity Knowledge Partners can help

Our Business Information Service team helps global investment banks and asset management firms capitalise on the transition to data processing and warehousing solutions, providing actionable insights through support ranging from thematic research, timely alerts on important events, identification of ESG trends and regulatory developments, and highlighting relevant KPIs for data-driven recommendations relating to green data centers for making informed investment decisions.

Our team sources relevant information on sustainable data infrastructure and strategies for reducing carbon footprint and ESG compliance, organising disparate data into usable formats to support investment analysis. By leveraging our Business Information Service, firms can stay ahead of market trends, identify investment opportunities and develop insightful content.

Sources:

-

https://www.computer.org/publications/tech-news/trends/sustainable-it-infrastructure

-

https://blog.sintef.com/digital-en/this-is-how-we-reduce-data-centers-carbon-footprint/

-

https://www.device42.com/data-center-infrastructure-management-guide/data-center-carbon-footprint/

-

https://www.datacenterdynamics.com/en/news/vertiv-launches-wooden-data-center-modules/

-

https://www.fortunebusinessinsights.com/green-data-center-market-105173

-

https://sustainability.atmeta.com/wp-content/uploads/2024/08/Meta-2024-Sustainability-Report.pdf

-

https://www.datacenterdynamics.com/en/news/odata-signs-ppa-with-atlas-to-power-chilean-data-center/

-

https://www.telehouse.net/news/telehouse-and-rwe-agree-10-year-power-purchase-agreement/

Tags:

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Mohammad Seraj – Working as sector specialist in Business Information Services team and responsible for Industry level research for a UK based investment bank. He has 10 years of working experience in niche sector research. Seraj holds an MBA from IILM Institute for Higher Education Gurgaon and has completed his B.Com from H.N.B Srinagar Garhwal University

Like the way we think?

Next time we post something new, we'll send it to your inbox