Published on May 9, 2024 by Jyotsana Khatter

A brief look at their history and facts

Gold holds cultural significance, signals affluence and is considered to be the most secure investment option, as its price remains stable when everything else is unstable.

India is one of the biggest consumers of gold and imported more than INR2.8tn worth of gold in fiscal year 2023, an 18% drop from 2022. It reported production of 1.2 metrics tons of gold in December 2022 and 780kg in fiscal year 2023; global mine production amounted to 3,100 metric tons of gold in 2022. India’s low domestic gold production resulted in its needing to import large quantities of gold, devaluing the INR and depleting its foreign exchange reserves. The government, therefore, implemented a number of measures in 2015, including the Sovereign Gold Bond Scheme (SGBS) to make productive use of gold and reduce imports.

The Sovereign Gold Bond Scheme

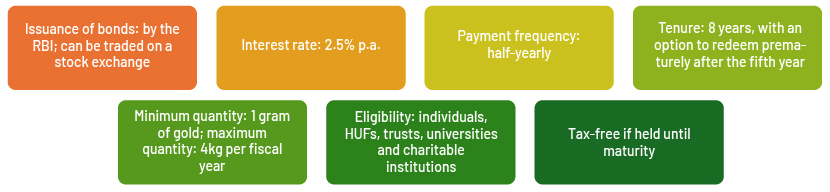

The government launched the SGBS in November 2015 to reduce demand for physical gold. Under the scheme, the Reserve Bank of India (RBI) opens issuance for subscription in traches, in consultation with the government. Bonds are denominated in multiples of grams of gold; the basic unit is 1 gram. These bonds are available in different series, with 2023-24 Series IV being the latest.

Investing in SGBs and key features

The bonds can be purchased from nationalised banks, selected private-sector and foreign banks, selected post offices, the Stock Holding Corporation of India Ltd (SHCIL) and designated stock exchanges either directly or via authorised agents. Bonds can be purchased by individuals, Hindu Undivided Families (HUFs), trusts, universities and charitable institutions. However, the RBI does not allow Non-Resident Indians (NRIs), Overseas Citizens of India (OCIs), Persons of Indian Origin (PIOs), private limited companies, other companies or LLPs to buy SGBs. Bonds can be purchased via cash (up to INR20,000 worth)/cheques/demand drafts/electronic fund transfers.

The RBI issues SGBs in a variety of tranches over a year; issuance is every two to three months, and the purchasing window remains open for about a week. Investors could also purchase bonds in digital or dematerialised form. Once physical purchase is completed, an investor could request the bonds to be credited in their demat account. The bonds remain in the RBI’s records until the dematerialisation process is completed. Investors can also purchase units via the stock exchange or secondary market.

Redemption/payout

The bonds have a lock-in period of eight years, with an option to redeem prematurely after five years via a direct sale on the primary market. However, if the bonds are in a demat account, they can be sold at any time on the secondary market. Investors can take loans against the bonds and could also gift/transfer bonds to relatives, friends and eligible investors.

On maturity, the redemption price is based on the simple average of the closing prices of gold of 999 purity of the previous three business days from the date of repayment, as published by the India Bullion and Jewellers Association Limited. In the secondary market, prices are based on prevailing prices in the market, based on demand and supply.

Taxation

Fixed interest income of 2.5% p.a. is fully taxable according to individual tax slabs; there is no tax deducted at source (TDS) on interest income.

If the bonds are held until maturity, capital gains arising from the redemption of SGBs will be tax-free. If SGBs are redeemed before maturity (i.e., after the fifth year and up to the eighth year), they will be taxable.

SGBs are permitted to be sold on the stock exchange even before the fifth year. Any gain arising from the sale of bonds will be considered as a capital gain. If a bond is sold before three years, it will be considered as a short-term capital gain; otherwise, it will be a long-term capital gain.

Investing in SGBs compared with other investments

| Parameter | Physical gold | Gold coin | Gold ETF | SGB |

| Regular earnings | No | No | No | 2.5% p.a. interest |

| Safety | Risk in handling and loss of value due to use | Risk in handling | High, as it is in electronic form | High, as it is backed by the government of India |

| Purity | Always doubtful | Depends on the issuer | High | High |

| Long-term capital gain (LTCG) | LTCG after 3 years | LTCG after 3 years | LTCG after 3 years | LTCG after 3 years. No capital gain tax if redeemed after maturity. |

| As loan collateral | Accepted | Accepted | Not accepted | Accepted |

| Exit option | Restrictive | Can be sold only on the market | Can be traded on the exchange | Can be traded on the exchange or redeemed from the government of India after 5 years |

| Storage cost | High, with risk | High, with risk | Low | Low |

Risks associated with investing in SGBs

-

Gold price fluctuations:

The price of gold is subject to market fluctuations. There may be a risk of capital loss if the market price of gold declines. However, an investor would not lose in terms of the quantity of gold paid for.

-

Liquidity risk:

The tenor of the bond is eight years, with an exit option from the fifth year. Selling bonds before maturity may result in limited liquidity. Additionally, secondary-market transactions may result in capital gain or loss.

-

Interest rate risk:

SGBs offer a fixed rate of interest; higher interest rates offered by other investments could make these investments more lucrative.

-

Inversely related to the stock market:

Gold prices have an inverse relationship with stock prices, with any upturn in the stock market leading to a reduction in gold prices.

Conclusion

The RBI sold 44.3 tons worth of SGBs in FY24, according to Business Standard, the most since their introduction in November 2015. SGBs worth USD3.26bn in FY24 would save 7-8% of the country’s annual import bill for the precious yellow metal. SGBs are a unique opportunity for long-term investors. Investing in them is convenient and secure, with a number of benefits, including safety, interest income and capital gains. However, investors should be aware of associated risks such as price fluctuations, liquidity risk and interest rate risk.

Sources:

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Jyotsana has over 10 years of experience in financial analysis and credit underwriting. Currently she is a part of Lending Services at Acuity Knowledge Partners undertaking credit underwriting for Asset Finance Group (AFG) for a leading US bank. Her expertise spans a broad range of credit analysis, financial modelling, credit underwriting and client facing role. She holds an MBA in Finance from Apeejay School of Management and Bachelors from University of Delhi.

Blog

Blog

India Budget 2025: Betting on Consumption and Fi....

The government is on track to achieving its multi-year fiscal consolidation target b....Read More

Blog

Blog

Will “angels” fall? Are BBB-rated borrowers ....

After an optimistic start to the year, higher interest rates and sticky inflation have dam....Read More

Blog

Blog

India Budget 2024: Prudent fiscal stance while b....

The government maintains a glide path to fiscal consolidation in the FY25 budget wit....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox