Published on November 26, 2019 by Khushboo Periwal and Yashas Gilganchi

In a first of its kind move, Dyke Bank will levy negative interest rates to mortgage lenders. Effectively, a borrower will repay monthly amounts which add up to less than the disbursed amount.

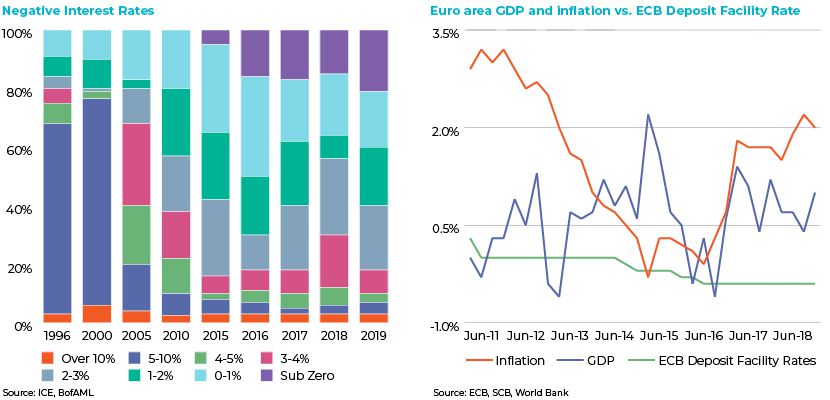

Economic down cycles prompt central bankers to slash interest rates to spur growth, investment and consumption. While monetary policy tools have seen some success in the past, during the current decade the world has witnessed limited effectiveness of monetary tools in boosting growth; this is in line with the Keynesian school of thought that money supply as a tool cannot spur growth. The continuous drawdown on using interest rates by central bankers has resulted in close to 20% of the outstanding global bonds yielding negative rates. This can be viewed as a situation wherein there is too much money chasing too few investment opportunities, hence investors are willing to pay a premium (negative interest rate) to forego future consumption/investment (due to uncertainty and risk) in exchange for parking money in safe assets. While there is limited headroom to lower interest rates further (considering rates are already negative), central banks have also resorted to asset purchases as a quantitative easing tool. Despite this, inflation in these countries remain stubbornly low and growth in most economies continues to languish.

Fallout of negative interest rates: While negative interest rates are aimed at spurring growth some economists have argued that negative interest rates erode bank profitability, encourage relaxed and risky lending, give rise to zombie firms1 , cause asset bubbles and encourage the use (or hoarding) of cash. We will take a closer look at the impact of prolonged low-interest rates in the real estate market

The case of Sweden:

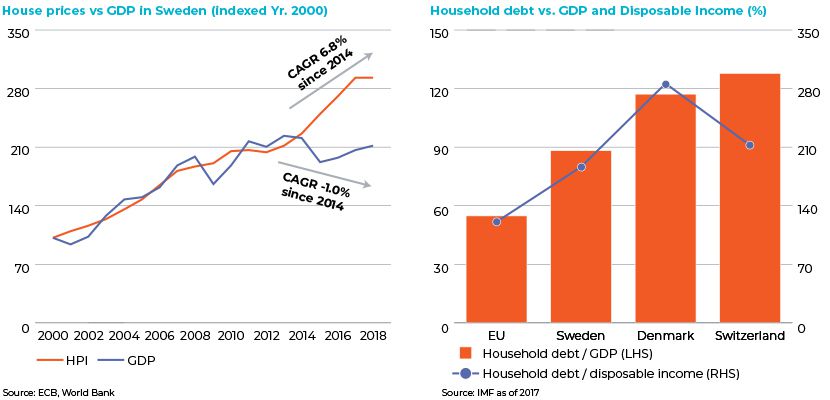

Risks: Low interest rates and relaxed mortgage repayment norms has allowed for a smart uptick in housing prices while preventing large scale defaults. For instance, typical mortgage loan maturity in Sweden 40 years as against 15-25 years in other EU countries2 . In Sweden, the excessive household leverage has been flagged as a risk by the central bank, IMF and OECD among others. Authorities are concerned that any stringent measures might trigger a sharp correction leading to cascading risks to the banking system.

Swedish banks fund mortgage loans by issuing covered bonds that have residential real estate as the collateral. A decline in house prices would increase refinancing costs of such loans.

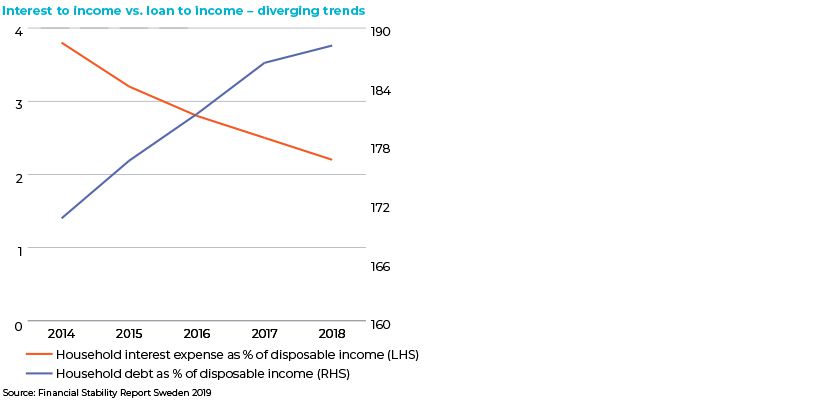

A sensitivity analysis conducted by Swedish financial institutions in 2018 indicate that under a stress scenario (increased unemployment rate, interest rate and simultaneous decline in property prices), 2.3% of the households would witness a negative equity and deficit. While the proportion is not significant, it is considerably higher than ~0.2%3 arrears on mortgage loans currently. We note that 70% of the mortgage loans are at floating rates.

Conclusion: The impact of lower interest rates has been lopsided on house prices. We believe, authorities should float reforms such as higher property taxes, housing purchase restrictions and accelerated mortgage repayments to mitigate the impact of lower interest rates on sectors prone to bubbles. In Sweden for instance property tax/GDP is among the lowest (~1% vs 1.7% in EU in 2017 as per IMF) while mortgage repayment tenures is among the highest in the region. Of late, Sweden has placed curbs on LTVs and implemented accelerated principal repayments to curtail excessive money flow in real estate, however these measures come after 4-5 years of a bull run in property prices. As property prices correct, banks and financial institutions would likely see a rise in NPL portfolios containing mortgages as collateral which would be put up for sale as banks would want to free up capital.

Acuity Knowledge Partners supports global asset managers to internalise more of their investment research process by building dedicated teams of research analysts out of our delivery centres in South Asia, Beijing and Costa Rica. Our analysts (MBA’s, Chartered Accountants, CFAs) work as an extension of the client team and support them on various types of client-specified research assignments. In the past, Acuity Knowledge Partners has supported real-estate focussed asset managers in bidding for secured NPL portfolios. The process included stratification and analysis of the loan portfolio to better understand the risks associated with these loan portfolios.

Source:

1. As per a World Bank study, zombie firms are entities that will be unable to sustain debt servicing costs over an extended period

2. European Economy Issue 21, Dec 2016

3. As per Skandinaviska Enskilda Banken AB

What's your view?

Thank you for sharing your Comments

Share this on

About the Authors

Khushboo has over 2 years of experience in equity research on various sectors. She has recently joined Acuity Knowledge Partners and is working in Real Estate sector as Senior Associate. As an equity research analyst she has worked in US and Australian markets and is proficient in modelling, forecasting and valuation. Khushboo holds a Post Graduate Diploma in Management (Finance) and a Bachelor’s Degree in Engineering (Information Technology).

Yashas has about 5 years of experience in investment research and capital markets. In his 6+ months experience in Acuity Knowledge Partners, he has been working on the real estate sector as a Senior Associate. He is proficient in financial modelling, understanding and interpreting debt issuance term sheets, assessing changes in capital structure and its impact on cost of capital and understanding evolution of capital under Solvency II regulations. Yashas holds a Post Graduate Diploma in Management (Majors in Corporate Finance and minors in Macroeconomics).

Blog

Blog

Independent research firms must scale up to gain....

Executive summary Independent research firms play a vital role in the investment researc....Read More

Blog

Blog

Advantages of having a remote executive assistan....

“They’re troubleshooters, translators, help desk attendants, diplomats, human database....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox