Published on December 9, 2022 by Gopal Soni

Environmental, social and governance (ESG) are the three core factors for measuring long-term corporate sustainability. With increasing environmental challenges and conscious efforts to achieve equity, ESG considerations have become crucial for business today. Multilateral financial institutions, banks and other financial institutions (as major debt capital and liquidity providers) play a key role in fostering a culture of environmental and social responsibility.

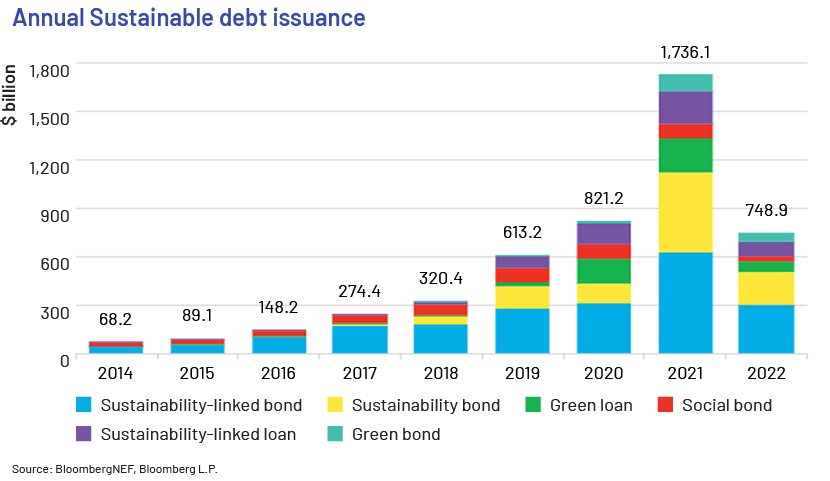

Sustainability-linked loans incentivise borrowers with reduced rates of interest/pricing for achieving certain predetermined key performance indicators (KPIs). Sustainability-linked loans have been increasing steadily in the global sustainable debt market (other than for a dip in 2020, possibly due to the pandemic), as depicted in the chart1 below.

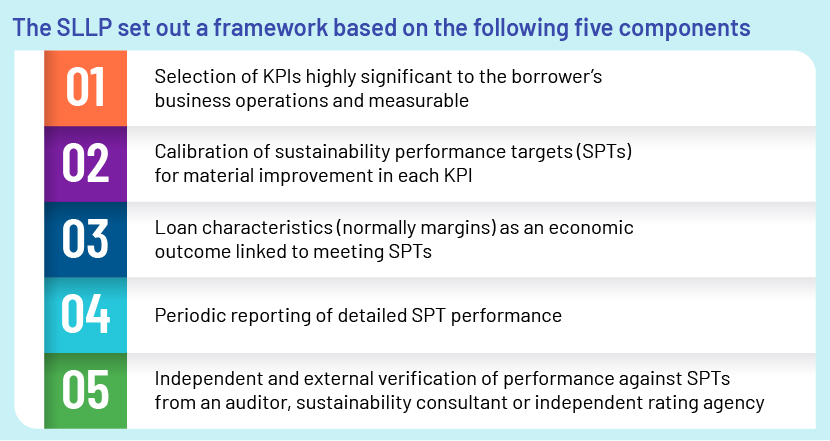

To facilitate and support environmentally and socially sustainable economic activity and growth through sustainability-linked loans, loan market associations, namely the LSTA, LMA and APLMA jointly published the Sustainability Linked Loan Principles (SLLP)2, and new roles such as sustainability co-ordinator/structurer have emerged in the loan market.

The SLLP are recommendations and are to be voluntarily applied by market participants on a deal-by-deal basis, depending on the underlying characteristics of the transaction.

To further address concerns related to inconsistent ESG reporting, the LSTA, Alternative Credit Council and PRI recently announced the launch of the ESG Integrated Disclosure Project (ESG-IDP). The ESG-IDP template benefits all stakeholders, namely investors, borrowers and credit fund managers. It provides borrowers with a harmonised and standardised approach to report ESG-related compliance to lenders.

Lenders currently use the SLLP framework for big-ticket deals, and lessons learnt from these deals should be used when there is an opportunity to work on KPIs for a deal in the middle market or SME segment. At the initial credit due-diligence level of looking at the borrower profile, common KPIs as set out in SLLP and sector-specific KPIs3 can be built in as part of sanction terms. There could be a financial outlay for borrowers for complying with additional ESG-related reporting requirements in the form of ESG audit reports/sustainability reports; borrowers could be incentivised through stepped-up margins. As part of the credit-monitoring requirement, these reports would indicate how many of the SPTs have been achieved. Commercial lenders could also include ESG performance as a parameter in their internal rating systems, along with existing financial and operating parameters. Incorporating ESG considerations in stress testing and ESG keywords/negative triggers/greenwash alerts into the borrowers’ related-party surveillance systems helps better integrate ESG criteria into commercial lending products across segments.

We are seeing more ESG data points now than in previous years, and data science and artificial intelligence (AI)-based solutions4 could effectively bridge ESG data gaps. Useful insights from machine-readable ESG documents could be extracted using AI/machine-learning techniques at the deal structuring stage as well as during the lifecycle of sustainability-linked loans.

Conclusion

Incorporating sustainability into the loan market is in a nascent stage, although lenders are not new to ESG factors5. The ability to assess potential borrowers using a standardised ESG approach and increased interest from borrowers to commit to long-term sustainability planning indicate integrating ESG criteria into commercial lending would become the new normal. ESG factors, being key considerations in determining the long-term sustainability of a business, would help lenders assess credit risk more holistically.

How Acuity Knowledge Partners can help

Our Lending Services business provides credit underwriting and portfolio management services. We assist in the initial underwriting of credit facilities and provide monitoring over the lifecycle of credit facilities. With our domain expertise in lending and associated services, we help clients integrate ESG criteria into commercial lending.

References:

-

Sustainable Debt Issuance Breezed Past $1.6 Trillion in 2021 | BloombergNEF (bnef.com)

-

https://www.lsta.org/content/sustainability-linked-loan-principles-sllp/

-

(PDF) Do environmental impacts matter to lenders? (researchgate.net)

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Gopal has about 9 years of experience in Lending Services with specialization in credit risk, LMA-APLMA documentation, credit, and agency operations. At Acuity Knowledge Partners, he is supporting the commercial banking group of a US-based bank, with exposure to the Utilities and Renewables Energy sectors. A significant aspect of his work involves writing new money requests, increase limit requests, refinance, annual reviews, and quarterly reviews. Gopal is a Chartered Accountant from the Institute of Chartered Accountants of India.

Blog

Blog

The US Public Finance Department’s national de....

Introduction The US faces a significant challenge in managing national debt, which has be....Read More

Blog

Blog

Green packaging material – understanding the ....

Sustainable materials are not always eco-friendly, but it has become necessary to adopt su....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox