Published on February 7, 2024 by Uttam Kumar Sharma

Overview

The International Sustainability Standards Board announced its new standards – S1 (covering general sustainability risk and opportunities) and S2 (climate-related risk and opportunity), creating a different and new space in capital markets for sustainability disclosures. These standards not only ensure confidence in a company's disclosures but also create a common platform and language for disclosing the effect of climate-related risks and opportunities.

Timeline

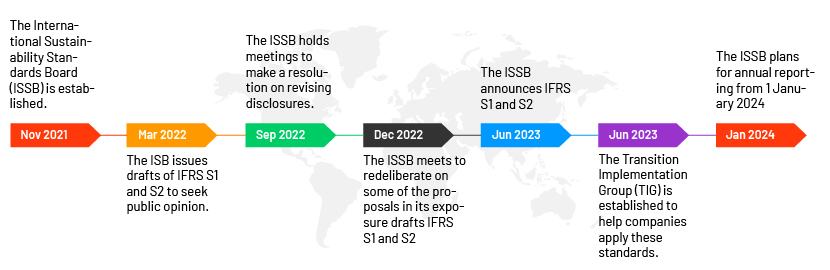

It took the ISSB committee more than 18 months of intense work to deliver these two standards; they are designed to help companies provide a picture of their robust sustainability structures that can be verified and are relevant for investment decisions. These helps investors make decisions faster in today’s dynamic capital markets.

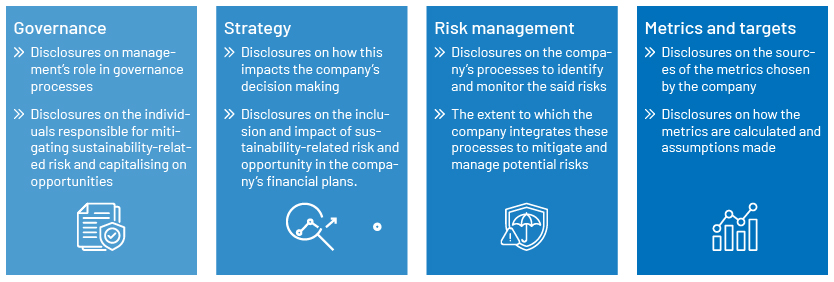

S1: Sustainability-Related Financial Disclosure: This framework provides guidance to identify and develop appropriate sustainability-related disclosures. An entity is required to disclose sustainability-related financial information on the following four parameters in terms of all risks and opportunities it faces.

S2: Climate-Related Disclosures: This sets the standards for climate-related disclosures, identifying the climate-related risks that could affect a company’s prospects and opportunities (such as for developing a new product).

Official launch of the IFRS standards: In November 2021, the IFRS committee formed the ISSB, backed by the G-20 economies in response to the need to formulate a global sustainability reporting standard. It plans for annual reporting from 1 January 2024. Companies in all jurisdictions are required to adopt these standards voluntarily, with their respective authorities deciding on the mandate. This as a game-changing step towards meeting sustainability reporting standards from the perspective of capital markets and investors.

Costs and benefits of sustainability reporting using IFRS S1 and S2

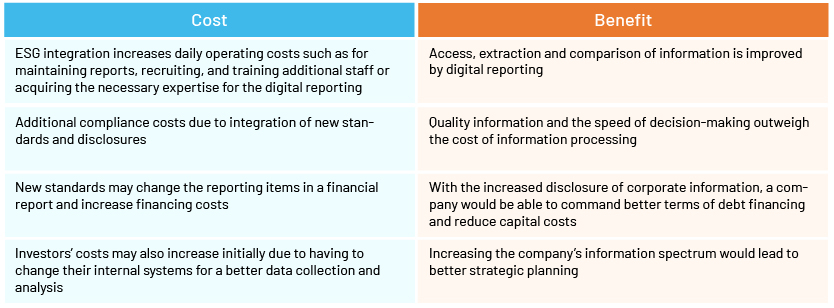

The ISSB’s standards could have a significant impact on the way companies disclose their information. The IFRS Effects Analysis describes the potential costs and benefits of adopting S1 and S2. There would be direct costs involved initially once a company is ready to apply these standards in its disclosures, but the ISSB committee believes that the benefits over time will outweigh the costs.

Impact of S1 and S2 on private equity companies

As ISSB standards are directly related to capital markets, private equity firms may also be affected by these reported standards to some extent, either directly or indirectly. It is in the interest of private equity firms to understand these new guidelines, assess their requirements and identify gaps in their current disclosure processes.

As transparency increases, integrating these standards with financial reporting would help private equity firms in their due diligence processes, enabling them to assess risks and opportunities of investments more holistically. It may also affect sustainability-minded limited partner. ISSB standards ensures uniformity of sustainability reporting, enabling private equity funds to be evaluated under a one standard; this would streamline reporting processes, reduce duplication, and improve comparability.

By adopting these standards and making a comprehensive assessment of sustainable risks and opportunities, private equity firms could strengthen and accelerate their decision-making processes.

How Acuity Knowledge Partners can help

We have been supporting global financial institutions for over two decades. We work as an extension of a client’s onshore research team, providing end-to-end support across ESG-specific RFPs/DDQs/RFIs, ESG validation, client reporting and content management. To help institutions communicate their ESG themes better, we leverage our extensive marketing experience, built over the years through collaboration with leading organisations.

Sources:

-

https://www.ifrs.org/projects/completed-projects/2023/general-sustainability-related-disclosures/

-

https://www.workiva.com/blog/new-issb-reporting-standards-how-will-your-business-be-impacted/

-

https://www.ifrs.org/news-and-events/news/2023/06/ten-things-to-know-about-the-first-issb-standards/

Tags:

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Uttam Kumar Sharma is Delivery Manager within the private markets domain working with private equity clients conducting bespoke research , benchmarking, competitive analysis, ESG research, ESG risk ratings, and helping the client with due diligence on companies/industries.

Uttam has over 12 years’ experience in this domain involved with renowned private equity players with furnishing research-based information comprising of industrial trends; interpreting the results of research studies.

Blog

Blog

ESG investing – beginner’s guide to responsi....

ESG investing in private markets integrates environmental, social and governance (ESG) att....Read More

Blog

Blog

Evolving landscape in ESG leadership in private ....

Introduction Several countries worldwide have mandated compulsory environmental, social ....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox