Published on August 19, 2022 by Debabrata Nayak

Private equity (PE) is a niche segment of the financial services sector. Due to the increasing complexity of the global financial system, regulators are kept busy trying to control the banking sector (which is capable of bringing the world economy to a halt, as it did in 2008) and the asset management sector, overseeing USD100tn of assets worldwide. The USD5tn managed by PE is small in comparison and has been largely under less supervision since its emergence in the 1970s.

Over time, there have been a number of cases of ethical violations in the banking sector for which banks and financial institutions have been heavily penalised. It should not, therefore, come as a surprise that an under-regulated sector such as PE could be suffering from the same problem.

Due to the under-regulation and loose control of the asset management sector, there is a lot of ambiguity surrounding PE, giving fund managers a great deal of freedom in determining performance valuation.

PE fund managers have traditionally followed these two approaches to fund performance valuation:

1. Investment multiple

Describes the value of investments returned to a limited partner as a multiple of its cost base

-

Distributed to paid-in (DPI) and total value to paid-in (TVPI) capital

DPI is calculated by dividing the cumulative distributions by the capital called and is often used in conjunction with equity capital market solutions to assess the performance and capital efficiency of private equity investments.

TVPI is calculated by dividing the realised amount added to the NAV of unrealised investment by the investment cost.

2. Internal rate of return (IRR)

The IRR is the annual yield on an investment that accounts for all cash flow of the investments since inception. The higher the IRR, the better the investment is performing (or is expected to perform).

The IRR is the standard performance measure and is widely used in analysing investments for PE; hence, we will analyse this valuation method in detail.

A growing body of research suggests IRR provides an imprecise assessment of performance. If the researchers are to be believed, an IRR makes returns seem better than they are due to the following limitations in its methodology:

-

Ignores economies of scale: When comparing projects, it does not take the project size into account. There can be a problem with this when two projects require significantly different capital expenditure but the smaller project has a higher IRR. For example, one should always prefer a project value of USD1,000,000 with an 18% rate of return over a project value of USD10,000 with a 50% rate of return.

-

Ignores future costs: The IRR is based on cash flow projected to generated by a capital investment without considering possible future costs that may affect profits. For example, if one is investing in transport vehicles, one needs to arrange a place for parking them, but such costs may not be factored into the IRR. The IRR may permit the purchase of a vehicle, but if the benefits will be offset by having to arrange for parking, the investment is not worthwhile.

French economist Ludovic Phalippou argues that “IRRs are not rates of return” (i.e., what is presented as a net return is not the rate of return actually earned by investors) due to a fundamental flaw of IRR mathematics — the reinvestment assumption. When early investments earn outsized gains, the IRR calculation automatically assumes that these early distributions will continue to be reinvested at unusually high rates of return regardless of whether those reinvestment opportunities truly exist. This, in turn, produces an IRR result that is implausibly high, if it is being thought of as a rate of return that an investor actually earns. Phalippou cites Apollo's IRR of 39% since its founding in 1990, According to him, a USD100m investment made in 1990 with a 39% return would be worth USD2.3tn if it compounded for 29 years through 2019. It is evident that Apollo does not make this claim.

However, investment banking professionals argue in favour of using the IRR methodology,

As PE is a cashflow business, the IRR is the most effective way to calculate returns for investors, allowing for easier comparisons between PE investments and other asset classes.

What makes the IRR ideal is that there is no cost of capital or hurdle rate, which are often subjective and end up as rough estimates. Using the IRR method, there is no requirement for calculating the hurdle rate; minimising the risk of calculating the wrong rate. After computing the IRR, projects whose IRR exceeds the estimated cost of capital can be selected.

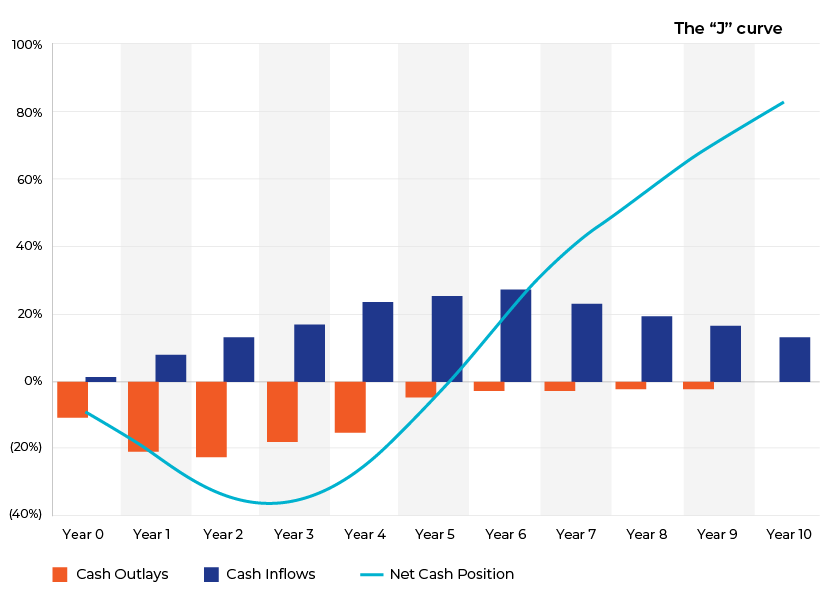

The IRR also has the distinctive potential to compute annual yield when cash flow is irregular and can measure performance under the J-curve effect, where it takes into account negative cash flows in the initial investment period of two to five years and positive cash flow after that. Measuring performance using other methods such as investment multiples has drawbacks, as they do not take the time-value of money into account, and are often fuelled by unrealised gains.

The graph above shows that the IRR of an investment is negative in the early years of a fund and turns positive in the later years of a fund’s life. It is called a “J” curve because the shape of the line vaguely resembles the letter “J”.

The IRR is still one of the most important and comprehensive performance measure used in PE sector, but the sector needs to improve its performance valuation methods and address the deficiencies in the current approach such as by taking into account the cost of capital calls. Holding the cash available to invest when requested by the general partner has a cost, and this needs to be factored in. More advanced methods such as the modified IRR (MIRR) could be used for performance evaluation. This assumes positive cash flow is reinvested based on the cost of the capital of the firm unlike the IRR, which assumes positive cash flow is reinvested at the same rate of return as that of investments. Although the sector is evolving, we hope more advanced performance measures would become the standard in the future.

How Acuity Knowledge Partners can help

As a global leader in investment services, we have a team of highly experienced PE professionals who dig deeply into cash flow and IRR calculations to discover hidden facts and provide an accurate picture of a PE fund's performance. We also specialise in areas of regulatory compliance, taking a holistic view of risk and regulatory reporting, and offer end-to-end due diligence and performance-monitoring services for PE and hedge fund service providers.

References:

https://www.sciencedirect.com/science/article/abs/pii/S0304405X18303015

https://www.jstor.org/stable/30225708

https://www.nber.org/papers/w22493

https://www.forbes.com/sites/forbesfinancecouncil/2021/06/08/private-equity-market-poised

https://www.bcg.com/en-in/publications/2021/global-asset-management-industry-report

http://www.ayakoyasuda.com/papers/2017/Paper12JFE.pdf

Tags:

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Debabrata has over 6 years of experience in Mutual Fund and Private Equity Fund Accounting under Asset Management space with BNP Paribas and State Street, he has been working with Acuity’s Compliance Operations team for over a year and responsible for Investment Monitoring and Trade support of Investment Compliance Services. Debabrata has done his MBA from Ravenshaw University.

Blog

Blog

ESG investing – beginner’s guide to responsi....

ESG investing in private markets integrates environmental, social and governance (ESG) att....Read More

Blog

Blog

Sustainable finance – regulations and trends 2....

Introduction Sustainable finance has become a critical theme internationally to pave th....Read More

Blog

Blog

Decoding SWIFT’s MT-to-MX migration – ch....

The global financial messaging space has taken centre stage since the migration to ISO 200....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox