Published on May 6, 2020 by Prachurjya Bharaly

COVID-19 has brought life to a complete standstill across the world. As of today, the virus has infected over 2.6m and claimed over 184,000 lives. The West has been hard hit, with the US accounting for c.32% of global cases and c.25% of global fatalities. Spain, Italy, France, Germany and the UK account for another third of total cases.

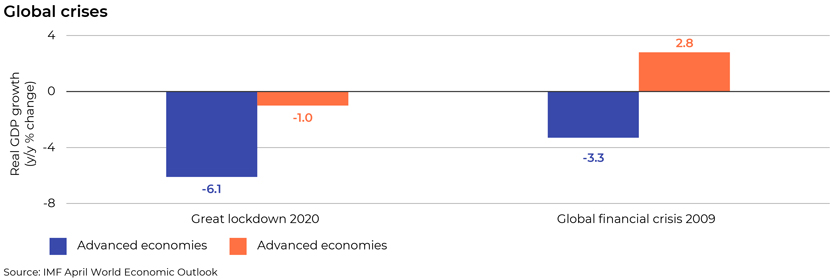

The Great Lockdown

With partial or complete lockdowns implemented across all major economies to prevent the spread of the virus, more than a third of the world’s population faces some form of restriction. The pandemic has already pushed the global economy into a slowdown that may potentially extend beyond 2021. In its April World Economic Outlook, the IMF described the current situation as “the Great Lockdown”, projecting that the global economy would grow at -3.0% in 2020. This is a sharp deterioration of 6.3 percentage points from its last forecast in January this year. The IMF has also said that the Great Lockdown would be the worst recession since the Great Depression of the 1930s and far worse than the Global financial crisis, 2008-09.

Difficult funding markets

Amid the coronavirus pandemic, the price of crude oil hit an 18-year low, and global oil demand is expected to reach its lowest level in more than 30 years. At the time of writing, West Texas oil futures that expired on 21 April were negative for the first time, primarily because the end-May contract forces physical receipt at a time when storage capacity is low. June prices settled around USD20 a barrel. The sudden drop in oil prices and record market volatility are pressuring the creditworthiness of companies, particularly those rated B- or lower by S&P, making it difficult for them to secure funding.

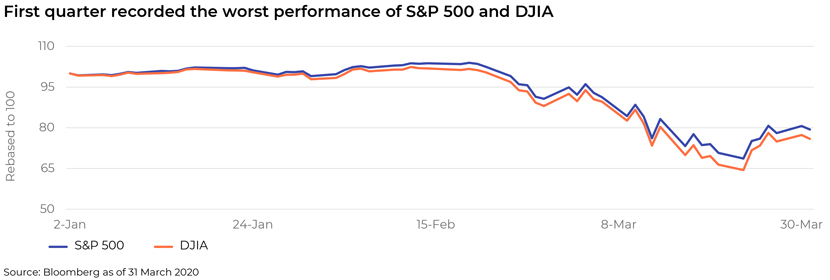

In the equities market, the S&P 500 and Dow Jones Indices slipped from their record highs of mid-February to reach their lowest levels on 23 March. The DJIA suffered its worst first quarter since 1987, tumbling 23%, and the S&P 500 saw its worst three months since the last financial crisis, declining 20%. With 5.25m Americans filing for initial unemployment benefits in the week of 10th April, around 22m Americans are currently out of job, indicating that the US labour market has effectively lost all the jobs created since the 2008 financial crisis. Dismal economic data from the US, coupled with weak first-quarter earnings, has reversed the optimistic tone of the recent trading sessions of the US stock market.

Primary investment-grade bond markets soaring

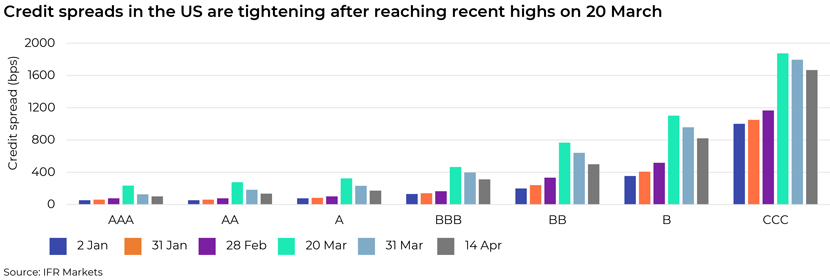

As COVID-19 wreaks havoc in the capital markets across the globe, there has been a flight to quality among bond investors, leading to a widening of bond spreads across most markets, especially the US. While spreads remain relatively wide, US investment-grade levels have tightened somewhat in recent weeks, as Figure 3 shows.

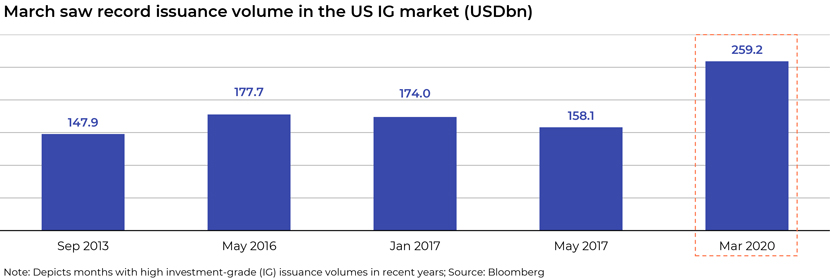

Amid the increasing number of coronavirus cases in the US and the impending global economic recession, US investment-grade issuers are rushing to tap the market to build their cash balances and refinance debt. The market set a new record in March 2020 with USD259.2bn of issuance volume, 46% higher than the previous record of USD177.7bn set in May 2016. 30 March saw USD37.175bn of issuance volume, the fourth-highest single-day volume total on record, led by Oracle’s USD20bn six-part offering (the eighth-largest deal on record). The week ended 27 March saw USD109.3bn in investment-grade issuance, 43% higher than the previous high of USD74.9bn priced in the week ended 6 September 2019. Apart from Oracle, we saw the likes of Exxon Mobil Corp.’s USD8.5bn five-part deal, McDonald's Corp.’s USD5.5bn seven-part deal, NIKE Inc.’s USD6.0bn five-part deal, Walt Disney Co.’s USD6.0bn five-part deal, Coco-Cola’s USD5.0bn five-part deal, and Intel Corp.’s USD8.0bn six-part deal coming to the market.

The significant resurgence of deals in the US investment-grade primary market was spurred by a series of unprecedented moves by the US Federal Reserve (Fed) to prop up liquidity in the country’s economy. Although the Fed used most of these programmes during the 2008-09 financial crisis, they have been implemented more aggressively and announced within a shorter period this time around. It is estimated that by the time the Fed finishes implementing these programmes, its balance sheet may have soared to as high as USD10tn. Key programmes announced by the Fed include the following:

-

3 March: In a bid to protect the longest-ever economic expansion in the US from the spreading coronavirus, the US central bank cut its interest rate by 50bps in an emergency move

-

15 March: The Fed made another 100bps cut in the interest rate, taking the benchmark for short-term lending to near zero. It also launched a new round of quantitative easing that encompasses USD700bn worth of asset purchases, including US Treasuries and mortgage-backed securities

-

23 March: The Fed created two new facilities that will directly impact the corporate bond market. The Primary Market Corporate Credit Funding Facility (PMCCF) will lend money directly to investment-grade companies. The Secondary Market Corporate Credit Funding Facility (SMCCF) will purchase investment-grade debt and investment-grade debt ETFs at market rates

-

9 April: The Fed announced its USD2.3tn lending programme that extended its primary and secondary bond-buying programmes to include “fallen angel” bonds, i.e., bonds issued by companies rated at least BB-/Ba3 and rated investment grade as of 22 March

These measures have given the markets the confidence that the central bank would do whatever it takes to ensure stability in the US credit market. Investors remain confident of a post-COVID-19 market recovery, with average new issue concession (NIP) improving in recent weeks. However, new issue premiums still vary significantly across tenors and ratings, and do not necessarily follow the ratings.

Despite Moody’s Investor Services forecasting that the US high-yield default rate could climb to 14.4% in a year from now, several crossover names and high-yield names have tapped the primary market recently in search of funding. In the crossover market, Ford Motors, after being downgraded to junk in late March, took advantage of the bond rally and priced a USD8.0bn three-part bond offering that carried Ba2/BB+/BBB- ratings. In the US high-yield space, 14 issuers raised a combined USD7.25bn in the week ended 17 April, taking the monthly issuance volume to USD12.425bn, well above the USD4.225bn for all of March.

Near-term outlook

As we move into the last trading week of April, we do not foresee a slowdown in the unprecedented pace at which US investment-grade issuers are tapping the US corporate bond market, trying to build up a war chest of cash amid the coronavirus outbreak. Most of the reputed businesses would be issuing bonds to pay down debt and push back maturities, while also repaying some of their intercompany loans. At the time of writing, April monthly volume issued in the US investment-grade market had already crossed USD163.2bn, in itself making the month the fourth-busiest ever.

Acuity Knowledge Partners is experienced in supporting investment banks in the US, Asia Pacific and Europe. We offer M&A, and debt- and equity-related solutions to onshore bankers. We have dedicated debt and loan syndication teams to help clients with research and analysis in terms of issuance and re-issuance related to bonds and other debt, so they could focus on pitching to clients and negotiations.

Sources:

https://www.worldometers.info/coronavirus/

Tags:

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Prachurjya has over 16 years of experience in investment banking with Acuity Knowledge Partners. At Acuity, he has led sector and product-specialist pilot teams across Capital Markets, ESG, Debt Advisory, Loan Syndications, Metals & Mining and Real Estate. He has been actively involved in setting up and on-boarding new ESG Advisory, ESG DCM and Sustainable Finance teams for various bulge bracket investment banks. Within DCM and Rating Advisory, he has been instrumental in helping the clients achieve over 30% in annual savings on both regular and adhoc tasks through standardization of the outputs and deployment of our proprietary BEAT tools.

Blog

Blog

China’s imports of Japanese food products decl....

Background China has consistently been one of Japan's most important trading partners: Ja....Read More

Blog

Blog

Interest Rate Divergence in 2024: A Global Conte....

Interest rates are diverging sharply in major economies, most notably in the US and the Eu....Read More

Blog

Blog

The mystery of black swans and how to prepare fo....

In the realm of global financial markets, there exist fascinating phenomena known as “bl....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox