Published on December 5, 2019 by Achini Udugama

Environmental, social and governance (ESG) criteria have gained the attention of financiers worldwide, enabling lenders to align loan terms to a borrower’s sustainability profile and peg rates to sustainability performance targets.

How ESG parameters can determine sustainable insights and help evaluate a company’s progress and identify associated risks

Voluntary guidelines provide a framework for sustainability-linked loan products. However, companies like Sustainalytics assist borrowers and investors in incorporating ESG factors in their investment processes via a standard reporting mechanism. An ESG rating, once assigned to a borrower, acts as a check and helps assess the borrowing company’s level of commitment to achieving sustainability performance targets. Banks often look at this ESG rating before structuring a loan product. The interest rate is pegged to the ESG rating or uses the rating as a performance target within the terms of a loan. A borrower can review its ESG parameters and work towards getting lower interest rates on future loans by empowering existing sustainability initiatives.

Regulations are needed to standardise sustainability reporting and to enable the creation of a platform that compares peer performance effectively. The EU recently agreed to introduce new mandatory disclosures to minimise the information asymmetry between lenders and borrowers. In addition, Sustainalyics provides more credible and unbiased ESG risk ratings that help assess a company’s management of material ESG issues.

How banks develop solutions via products and mechanisms

Primarily, banks can review their advance portfolios by defining their expected stance in the market and identifying and strengthening ESG parameters. The following could be implemented based on these parameters:

1. Channelling credit lines and initiating programmes that improve the standard of living and enable the sustainable use of natural resources and environmental protection. Banks can use green loans to finance energy projects, solar energy and wind farms and fund a circular economy, aimed at eliminating waste and the continual use of resources.

2. When a client invests in an ESG project, banks could allocate a certain percentage of the fund that covers the value of the investment, enabling the client to invest in the future, ensuring smooth operation and continuity of the project.

3. Assessing ESG parameters periodically to check rating variances. This will be useful when monitoring a client and when trying to gauge the client’s commitment. Clients could then be rewarded accordingly, i.e., those who scored a higher ESG rating could be compensated with lower pricing (and vice versa for those who reported deterioration in performance).

4. Offering attractive pricing for savings products generated from sustainable/green revenue. If a client has obtained a loan to fund a plant for recycling purposes, banks could offer an attractive price for the effort by way of a comparatively higher savings interest rate for the monies or one equivalent to cost savings from the project.

5. Assessing probable ecological and social risks in loan application considerations by checking and upgrading ESG matrices on a regular basis.

How Acuity Knowledge Partners can help in developing these mechanisms

Acuity can help integrate ESG criteria into strategic operations and business functions and enable investors to make more informed decisions via symmetric information, covering all sustainable and ethical investment approaches (such as databases, ratings, sector analyses, and portfolio analyses).

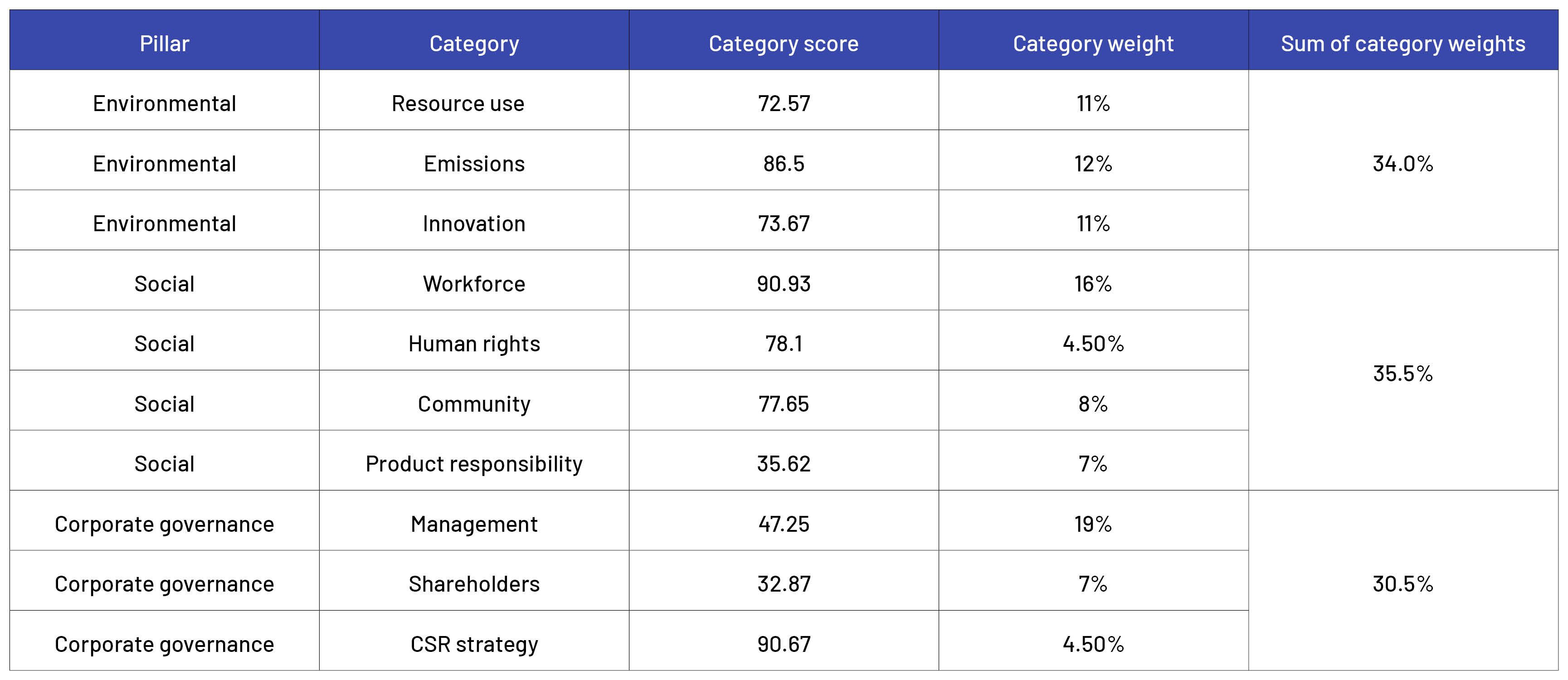

Sample ESG rating matrix

Source: esg-scores-methodology.pdf

Sources:

Tags:

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Achini is Delivery Lead at Acuity Knowledge Partners’ commercial lending team in the Colombo Office. She has over 6 years of onshore experience in corporate lending. Prior to this, she was part of the corporate banking team for a local bank in Sri Lanka. She has a Master of Economics and a Bachelor of Business Administration from the University of Colombo, Sri Lanka.

Blog

Blog

ESG investing – beginner’s guide to responsi....

ESG investing in private markets integrates environmental, social and governance (ESG) att....Read More

Blog

Blog

Evolving landscape in ESG leadership in private ....

Introduction Several countries worldwide have mandated compulsory environmental, social ....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox