Published on November 19, 2020 by Anurag

The COVID-19-induced recession has been pressuring small and medium-size enterprises (SMEs) in an unprecedented manner. SMEs account for a large share of employment (c.47% of the private sector’s) and other economic activity in the US, according to the 2020 Small Business Profile published by the Office of Advocacy of the US Small Business Administration.

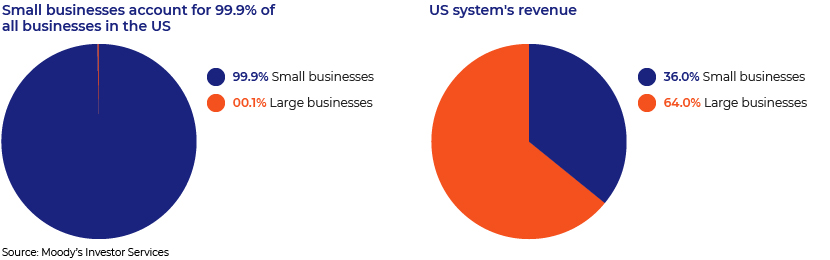

Small businesses account for c.99.9% of total businesses operating in the US and generate c.36% of the system’s business revenue. Thus, an impact on SMEs would have a ripple effect on other sectors.

Generally, such enterprises generate less than USD10mn revenue or operate with fewer than 500 employees.

A random survey ofc.8,000 small businesses in the US, as part of a broader collaborative project by researchers at Yale, Princeton and Oxford, revealed that 60% of the respondents had laid off at least one employee by 1 May2020. According to an ADP job survey, non-farming companies with fewer than 500 employees had cut c.23m jobs by July 2020.

The pressure on SMEs will likely affect other institutions such as banks, non-banking financial institutions (NBFIs), asset management companies, credit card companies, structured finance transactions, business development companies and non-financial companies with franchise-based business models. However, government-backed support programmes should partly mitigate the liquidity risk. Programmes such as the Pay check Protection Program(PPP) established by the US government’s Corona virus Aid, Relief, and Economic Security Act (CARES Act) can be used by small businesses to pay up to eight weeks of wages, interest on mortgages, rentals and utility expenses.

By 17 August 2020, a corpus of USD659bn was available to small businesses through the PPP programme.

Impact on banks:

Banks with strong exposure to SME lending are expected to witness a sharp fall in asset quality and profitability due the weakened debt repayment capacity of SMEs. However, such banks have not yet reported a material increase in impaired loans as a percentage of gross loans, due to the broader repayment deferral programmes driven by regulators. Total SME loans [proxy less than USD1mof loans in the commercial and industrial (C&I) loan book] stood atc.USD370bn, or 2% of total US commercial bank assets, as of December 2019. However, SME exposure outside of the C&I portfolio (i.e., commercial real estate loans, loans backed by residential mortgages, personal loans of SME employees and owners, lending to NBFIs that further lend to small businesses and leveraged loans) is much larger and difficult to quantify.

Regional banks are likely to take a bigger hit, given their large exposure to SME lending as they focus more on community needs. According to a recent FDIC survey, 80% of small banks (with less than USD10bn in assets) reported their C&I portfolios as comprising SMEs, compared to an average of just 10% for mid-size to large banks. However, the share of SME loans has declined by over one-third in the past decade.

Collateral used to secure debt:

The pandemic would, therefore, have a severe impact on banks’ asset quality, profitability and capitalisation in the coming quarters.

Impact on credit card companies:

Most credit card companies assist SMEs in meeting their spending needs and managing their working capital. We expect SMEs to reduce their daily spending, and delinquencies to increase, impacting the asset quality and profitability of such companies.

However, some large credit card companies have diversified their product lines and should, therefore, see the impact offset. One example is American Express (Amex; rated A3 by Moody’s).

Amex’s write-off rate on card member receivables was 2.2% as of 1Q FY20, We expect Amex’s strong fundamentals to support it during the pandemic, despite large exposure to SMEs (c.20% of its loans as of 1QFY20).

Advantage for asset managers:

Most asset managers have large amounts of dry powder in their funds, which should help them exploit the situation with attractive projected returns, paving the way for strong performance fee-generating capabilities in the coming years.

Asset managers have become an important source of funding for SMEs recently and have raised a significant amount of institutional and high-net-worth capital to invest in them.

Impact on business development companies (BDCs):

BDCs are closed-ended funds that provide funds to companies with less than USD250m in assets with debt or equity. The pandemic-led stress on SMEs and middle-market companies will likely weaken BDCs’ asset quality, profitability and capitalisation. Banks have reduced the funding granted to SMEs over the past decade, presenting an opportunity for BDCs to grow. As of March 2020, outstanding debt of Moody’s-rated companies stood at USD23.7bn. As SME loans are expected to deteriorate further due to the pandemic, we expect BDCs’ asset quality to be impacted.

Impact on structured finance transactions:

The economic weakness would also result in SME delinquencies and impairments in structured finance transactions. Transactions involving SMEs are the most vulnerable, as the economic shock would impact the credit quality of the asset pool in unsecured small business loans, equipment finance leases and commercial real estate asset-backed securities (ABS),leading to collateral losses.

Overall, the financial challenges faced by SMEs would weaken the asset quality of financial institutions and structured finance transactions that are tied to SMEs. The business losses of SMEs would impact corporations that have SME clientele and organisations that operate on a franchise-based business model. The impact on SMEs could lead to widespread job losses and reduced consumption, further dampening the asset quality and profitability of all issuers, partly mitigated by immediate government support.

How Acuity Knowledge Partners can help:

Acuity Knowledge Partners (Acuity) supports global and regional commercial banks and investment banks with constant and granular monitoring of their portfolios with the help of analysts at its delivery centres in India, Sri Lanka and Costa Rica. Our analysts (MBAs, chartered accountants, CFAs) work as an extension of the client team and provide support on various types of portfolio monitoring activities in the credit space, including financial modelling and valuation, financial spreading, covenant monitoring, extrapolating bankruptcy threshold triggers, providing refined early warning signals (negative news support), credit ratings, customised credit reports, short-term outlook, and a host of other value-added research involving art-of-the-craft IT solutions. All credit solutions provided by Acuity are customised and reflect the client’s proprietary and differentiated analysis. This gives the client a unique sustainable edge.

References:

https://www.fedsmallbusiness.org/survey/2020/report-on-employer-firms

https://news.yale.edu/2020/05/01/survey-shows-pandemics-severe-impact-us-small-businesses

https://www.moodys.com/researchdocumentcontentpage.aspx?docid=PBC_1226372

https://www.sec.gov/spotlight/sbcfac/2020-02-04-presentation-pitchbook-venture-climate.pdf

https://home.treasury.gov/policy-issues/cares/assistance-for-small-businesses

Tags:

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Anurag has over 13 years of experience in the financial services and banking domains in managing commercial credit portfolios and writing reports such as thematic credit, credit rating, annual review and counterparty risk reports. His key responsibilities at Acuity include managing a credit portfolio for a US-based regional bank. Prior to joining Acuity in 2019, Anurag worked as a manager with a large US bank.

Blog

Blog

China’s imports of Japanese food products decl....

Background China has consistently been one of Japan's most important trading partners: Ja....Read More

Blog

Blog

New Trends and Opportunities in SME Lending....

SMEs are generally defined based on parameters such as annual sales, number of employees, ....Read More

Blog

Blog

The mystery of black swans and how to prepare fo....

In the realm of global financial markets, there exist fascinating phenomena known as “bl....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox