Published on May 15, 2020 by Anithavani Devaraj

History

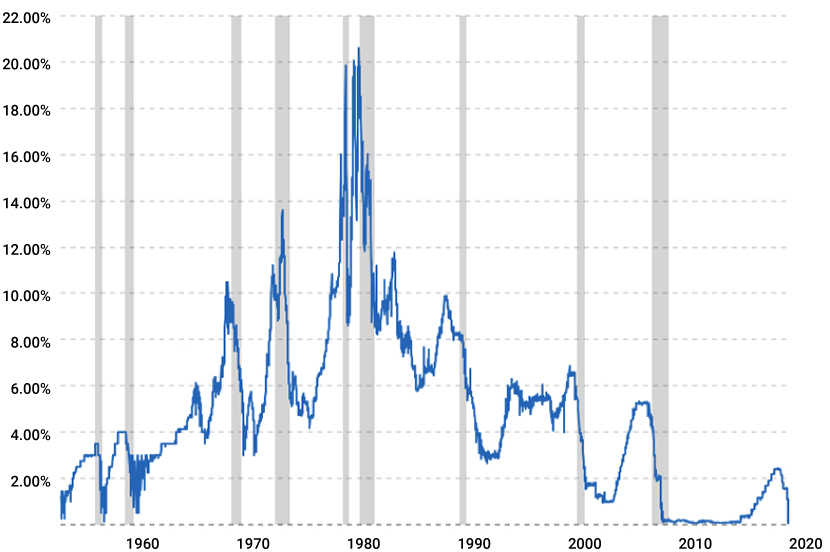

The Fed funds rate has a history of ups and downs. It reached a high of 20.0% in 1979 and 1980 due to a spike in inflation since the 1970s. Subsequently, the rate declined gradually, ending the decade at around 8.0%. US Inflation also fell to 4.65% by 1989 and has not moved above 10.0% since then. The recession of the mid-1990s lasted for eight months (from July 1990 to February 1991). Thereafter, the Fed rate remained quite steady for the rest of the 1990s. It increased from 1.00% to 5.25% from June 2004 to June 2006. The economy recovered, and the rate had increased further by 2007. The Fed lowered the rate to 0.0 to 0.25% in 2008, during the worst financial crisis, and the rate remained within that range until 2015.The dot-com market crash, the 9/11 terrorist attacks and the recession drove rates lower in the first half of the decade. The Fed then began to raise the benchmark rate, and it rose steadily until 2018. It cut the rate gradually in 2019, signaling that economic growth was beginning to slow. In March 2020, the Fed lowered the interest rate to zero due to the escalating COVID-19 outbreak that has impacted not only the financial markets but also the global economy and everyday life.

Covid-19 outbreak – The Fed’s action plans

The Fed has taken emergency action to boost liquidity in the U.S. financial system.

-

-

It lowered its target interest rate by a full percentage point nearly to zero, followed by a 50 bps cut on 3 March. The Fed rate is considered as a basis for fixing short-term and long term rates which will reduce the cost of borrowing on different types of loans like mortgages, home equity loans, auto loans and other loans.

-

Initially, the Fed said it will purchase at least USD700bn in Treasuries and mortgage-backed securities in the coming months. But, it expanded the purchases to other money market instruments on 23 March to enable uninterrupted credit flow in the economy.

-

To keep up the credit market functioning even during crisis time, the Fed has come up with Primary Dealer credit Facility (PDCF) program which offers reduced interest rate loans for a period up to 90 days to 24 financial organizations with large capital base.

-

To ease liquidation of money market instruments like commercial paper and treasury securities for investors, the Fed has re-launched them program called Money Market Mutual Fund Liquidity Facility (MMLF). This program aims to lend the banks against collateral they purchase from the primary money market funds. The scope of REPO operations are also expanded considerably.

-

It is encouraging banks to borrow from its discount window, where it extends credit to banks backed by a wide range of collateral, by reducing the penalty banks have to pay above market rates and extending the maturity of the loans to 90 days.

-

To increase public lending during crisis period, the Fed is temporarily relaxing on regulatory requirements for both largest and community banks. It also reduced the reserve requirements for thousands of banks to zero, effective from 26 March.

-

The Fed is directly lending to high rated US corporations. It is establishing new programs to provide up to USD300bn in new financing to support the flow of credit to employers, consumers, and businesses. The Department of the Treasury, using the Exchange Stabilization Fund (ESF), will provide USD30bn in equity to these facilities.

-

The Fed buys commercial paper directly there by lending to corporations for up to three months at a rate higher than overnight lending rates through Commercial Paper Funding Facility (CPFF) program. This step will ensure maintaining the employment and investment nationwide.

-

The Fed and five major foreign central b

The Fed is taking steps to ensure credit continues to flow to households and businesses at this time so the financial system is not affected.anks cut pricing on their swap lines to make it easier to provide dollars to financial institutions around the world that are facing stress in credit markets.

-

The Main Street program will help the small and medium sized business by lending up to USD600bn in four years loans.

-

The Fed will support consumers, households and small businesses through Term Asset-Backed Securities Loan Facility (TALF) by lending new collateral loans up to USD100bn.

-

The Fed has initiated direct lending to state and municipal government by purchasing up to USD500bn of investment grade notes maturing within maximum of 3 years period.

-

The Fed announced a new package on 9 April, providing up to USD2.3tn in loans to support the economy. The Fed is deploying these programs and will be proactively followed until the market is recovered fully. The Fed also takes measures daily to curb the financial crisis due to the COVID-19 outbreak. Fed chair Jay Powell stated that economic conditions were so vulnerable to the spread of the virus that the Fed had suspended its regular economic projections until June 2020.

Impact on mortgage interest rates

Mortgage rates are determined by factors such as the inflation rate, employment rate and market conditions. The Fed does not fix the mortgage rates directly, but changes in the Fed rate affect the mortgage rate indirectly. The Fed funds rate and the mortgage rate generally move in the same direction.

Refinancing mortgage during a Pandemic: The Fed continues to try to mitigate the financial impact of this COVID-19, in part through low mortgage rates. According to Freddie Mac, twice the US Mortgage rates hit an all-time low in March 2020 and 30 April 2020, wherein the average rate of the 30-year fixed-rate mortgage dropped to 3.29% and 3.23%, respectively. The interest rate on 15-year fixed-rate mortgages are at 2.77% which is in line with March 2020. Interest rates on five-year adjustable-rate mortgages fell from 3.28% to 3.14%. Borrowers are willing to move from a 30-year term to lower terms, such as a 20-year or 15-year term, because interest rate are very low and they could complete payment in,say,15 years the earliest. Lower interest rates encourage more money to flow into the economy, promoting businesses to invest and consumers to spend and borrow. While the majority of mortgage movement has centered on refinancing, Freddie Mac credits the low rates with improving home purchase activity in recent weeks. According to the Mortgage Bankers Association, Nationally, applications for home purchase loans increased12% for the week ended 24 April.

A lower rate can prove beneficial in terms of home financing, but the impact depends on what type of mortgage the consumer has, whether fixed or adjustable, and which rate the mortgage is linked to. Amid the outbreak, a lender would want to be assured of a borrower’s potential income-that the borrower is employed and still working – when the lender calculates the valuations and considers the underwriting.

A lower rate makes adjustable-rate home loans cheaper, improving the housing market. If a borrower is looking for a shorter-term mortgage, say a 5/1 adjustable rate mortgage (ARM; meaning the interest rate is initially fixed for five years and is then adjusted each year), the borrowers could save considerably on interest. This is because the introductory rate of an ARM is usually lower than that of a fixed-rate mortgage.

Impact on existing borrowers with fixed-rate loans: A fixed-rate mortgage has an interest rate that remains the same for the entire duration of the loan. A Fed rate cut would not affect the monthly payments of existing borrowers, as the rate has already been locked in.

Due to the Covid-19 outbreak, mortgage rates may fall more in the days and weeks to come; existing borrowers could, therefore, opt for refinancing lock in the interest payments at a lower fixed rate than before, although they would need to spend a few thousand dollars in closing costs. Experts say that rates on fixed-rate mortgages generally fall after a Fed rate cut.

Before a refinancing decision is made based on a Fed rate cut and mortgage rates, borrowers should consider any upfront costs and fees associated with refinancing to ensure these do not offset potential savings.

If a mortgage is federally backed and a borrower experiences financial hardship directly or indirectly due to COVID-19, a lender is supposed to exercise forbearance. The Coronavirus Aid, Relief, and Economic Security (CARES) Acts allows certain borrowers to defer their mortgage payments for up to 180-days, and possibly longer. The mortgage servicer should not collect additional fees, penalties, or interest from the borrower. A Servicer may also not initiate a foreclosure or execute a foreclosure sale within 60 days from 18 March 2020. Landlords with multifamily mortgages are allowed 30 days of forbearance, with the option of extending it for a maximum of another two 30-day periods, to exercise the options borrower should give at least 15 days prior notice to the servicer from the current forbearance period. Temporary financing loans (i.e., construction loans) are not qualified for forbearance. A multifamily borrower can terminate the forbearance option at any time. The industry has requested that the Fed and Treasury use the powers granted by the CARES Act to create a new liquidity facility to support the forbearance policies included in the Act.

How interest rates affect bond markets

Investors generally watch the Fed funds rate closely. As interest rates are low at present, it is easier to borrow money, and many companies will likely issue new bonds to finance expansion. This would create demand for higher-yielding bonds, forcing bond prices higher. However, the higher prices would mean that yield is less for the investors; this situation will likely continue until supply and demand reach a new equilibrium.

For this reason, when the Fed Reduced interest rates by 50bps on 3 March 2020, the bond market fell. The yield on 30-year Treasury bonds dropped to 1.64% from 1.66%, the yield on 10-year Treasury notes fell to 1.02% from 1.10% and the yield on 2-year notes fell from 0.71% to 0.23%.

Recently Fed announced to purchase at least USD500bn of Treasury to supports the smooth flow of credit to corporate and government. At this point of time, issuers of callable bonds may choose to refinance by calling their existing bonds so they can lock in a lower interest rate.

For the new investor, these lower interest rates directly impact the bond market, as yields on everything from US Treasuries to corporate bonds tend to fall, making them less attractive.

The Fed’s role in controlling recession and inflation

The foremost job of the Fed and global central banks is to control inflation to avoid a recession. During a financial crisis, the primary tool the Fed uses to do this is the manipulation of short-term interest rates. This results in raising or lowering interest rates to slow or encourage economic activity and control inflation.

In order to manage inflation in the economy, consumer Price Index (CPI) and Producer Price Index (PPI) are being continuously monitored by Fed. When these indicators start to increase by more than 2–3% a year, the Fed would raise the Fed funds rate to control the increase in prices. This is because if interest rates increase, borrowing cost will rise and people will eventually spend less. Demand for goods and services will fall, causing inflation to drop.

For example, Inflation was 14% in both 1981 and 1982.The Fed raised interest rates to 19%, resulting in a severe recession. To reduce inflation, the Fed reduced the interest rates, which contributed greatly to a recovery. When the Fed lowers the Federal funds rate, it becomes cheaper to borrow money, encouraging people to start spending again.

The bottom line

The Fed funds rate is adjusted to control inflation and maintain healthy economic growth. The rate would be maintained near zero until the economy has overcome the recent crisis and is on track to return to growth, previous consumption levels, prices and stock market returns; and maximum employment. The Fed is taking steps to make sure that credit continues to flow to households and businesses during this crisis time so that it does not affect financial system of the economy. Various preventive measures are initiated to limit the long term damage to the country. This will help economy to grow again, supply goods and services to meet demand. However, the COVID 19 outbreak is having a significant impact on the economy, and it is too early to predict how far-reaching the effects will be.

Reference

https://www.consumeraffairs.com/finance/types-of-mortgage-loans.html

https://www.thebalance.com/fed-funds-rate-definition-impact-and-how-it-works-3306122

https://www.nerdwallet.com/blog/mortgages/fed-mortgage-rates/

https://www.macrotrends.net/2015/fed-funds-rate-historical-chart

https://www.brookings.edu/research/fed-response-to-covid19/

https://money.com/mortgage-rates-new-record-low/

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Anithavani Devaraj has been part of Acuity Knowledge Partners’ RECM team since 2015. Prior to this, she spent 4 years at Accenture Credit Services. She has 9 years of experience in commercial real estate cash flow modelling, valuation analysis, lease abstraction, loan origination and detailed loan underwriting.

Blog

Blog

China’s imports of Japanese food products decl....

Background China has consistently been one of Japan's most important trading partners: Ja....Read More

Blog

Blog

New Trends and Opportunities in SME Lending....

SMEs are generally defined based on parameters such as annual sales, number of employees, ....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox