Published on August 28, 2025 by Abhisek Sasmal

The International Financial Reporting Standard 17 (IFRS 17) came into effect on 1st January 2023, with IFRS 17 implementation by hundreds of insurers managing trillions of dollars in assets globally. It eliminates existing inconsistencies and allows investors, analysts, and others to make meaningful comparisons among insurance companies across various jurisdictions.

Through this blog, we will explore the IFRS 17 impact on insurers, and how investors and analysts interpret the various changes in financial statement representations.

What is IFRS 17?

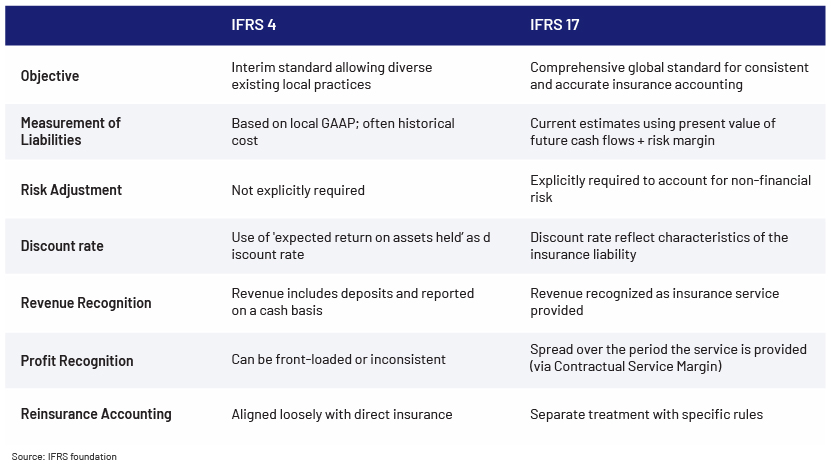

IFRS 17 Insurance Accounting is the first global, comprehensive standard that covers insurance contracts. IFRS 17 applies consistent accounting for all insurance contracts. It replaces the outdated IFRS 4, which allowed inconsistent practices across companies and countries.

Who are affected?

-

All entities that issue insurance and reinsurance contracts

-

Reinsurance contracts that the company holds (“ceded reinsurance”)

-

Investment contracts with discretionary participation features (“DPF”) that it issues, provided that the entity also issues insurance contracts

-

Excluding product warranties from manufacturers, financial guarantee contracts, fixed-fee service contracts

What has changed from IFRS 4?

IFRS 17 core requirements

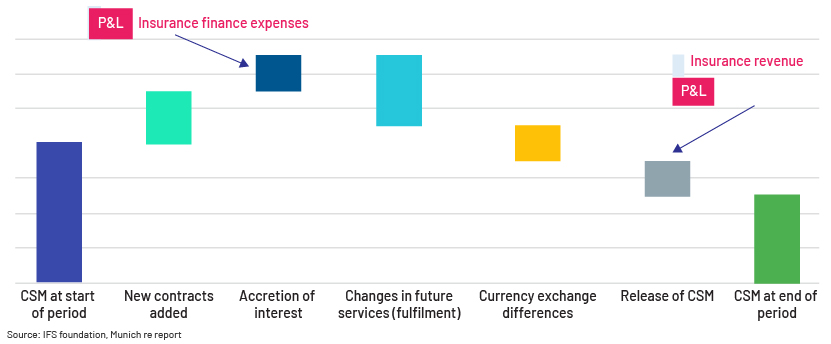

Under IFRS 17, companies must measure their insurance contracts as the sum of the fulfilment cash flows – representing a sum of the present value of probability weighted expected cash flows and an explicit risk adjustment to reflect the uncertainty of the insurance risk – and the contractual service margin (CSM).

CSM is again adjusted by changes in estimates and allocated to P&L over a period of time. In each reporting period, insurance entities re-measurers the fulfilment cash flows based on updated assumptions on risk adjustments and discounting rate.

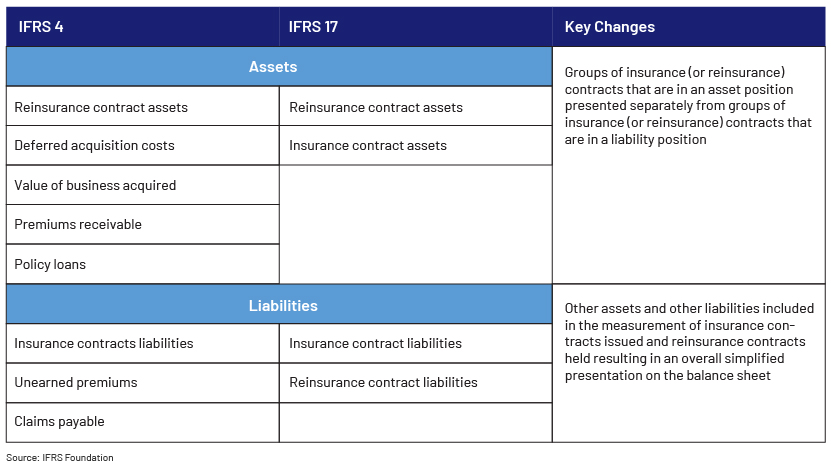

How it has changed the balance sheet presentation for insurers?

Balance sheet presentation under IFRS 4 comprised many inconsistent terminologies and measurements, whereas under IFRS 17, it is meaningfully different, reflecting a clear shift towards a more transparent, consistent and financially realistic view of insurance liabilities and related assets. Under IFRS 17, a group of insurance contracts that are in the asset position are different from the insurance contacts that are in the liabilities position. This avoids netting unrelated contracts and shows underlying profitability more clearly.

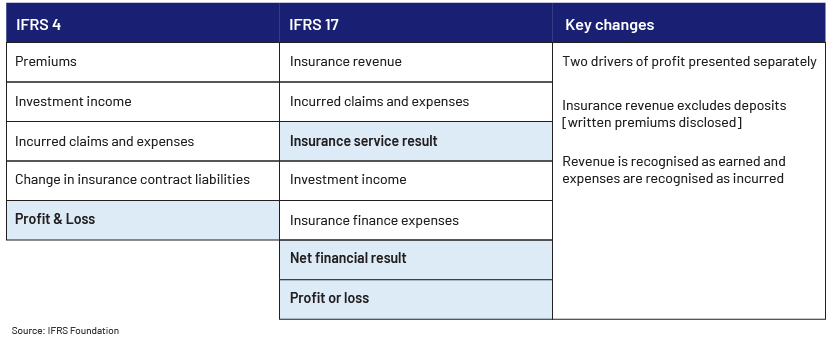

How has it changed the income statement presentation for insurers?

Under IFRS 4, income statement formats varied under various jurisdictions. Written premiums were commonly recognised as revenue, which included collection of deposits. Insurance and investment components were often combined. Changes in insurance contract liabilities included different non-comparable items and were challenging to project. But IFRS 17 has clearly demarcated insurance service results and insurance finance income and expenses. Under IFRS 17, profit is recognised over the coverage period via the release of the CSM.

How IFRS 17 is helping investors and analysts?

In the earlier regime of insurance accounting and reporting, investors and analysts faced two major problems: (a) lack of relevant and transparent information and (b) lack of comparability at multiple levels. As shown in the previous sections of this blog, IFRS 17 now presents a simpler, transparent and comparable way of accounting and report presentation, which will help investors and analysts make informed and value-driven decision. Analysts can understand what portion of income is now from underwriting compared to investments, improving profitability analysis. Investors gain insights into sustainability and riskiness of future earnings. Earnings become less volatile and more reflective of performance over time by spreading profit recognition over the service period (via the CSM). This helps analysts build more accurate forecasts and valuation models.

How Acuity Knowledge Partners can help

Acuity Knowledge Partners has built a pool of subject-matter experts and sector leads who are capable of understanding the nuances of complex accounting rules and are updated with all the latest changes happening in various industries. Their in-depth knowledge will help all investors to catch the early trends and make financial models that reflect the current accounting policies, regulatory changes and country-specific rules.

References

Tags:

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Abhisek Sasmal has over 15 years of work experience in equity and macro research, financial and credit risk modelling. Currently he is supporting a European buy side client mainly on the diversified financial sector. He has been with Acuity for last 14 years supporting Global Fund Managers and sell side analysts in their research on Global BFSI. He is an MBA in finance and CFA charter holder. Before joining Acuity Knowledge Partners, he used to work with some leading domestic sell side firms in India on diversified sectors.

Blog

Blog

IFRS S1 and S2 mark a new era in sustainability....

The International Sustainability Standards Board’s (ISSB’s) first environmental, socia....Read More

Blog

Blog

IFRS 18 – a step in the right direction; what ....

IFRS 18 brings significant changes to the way the statement of profit and loss (income sta....Read More

Blog

Blog

Unlocking the value of collateral: Insights on t....

Introduction Collateral management is the cornerstone of financial transactions, encomp....Read More

Blog

Blog

Silent stress: CRE refinancing risks hidden i

Despite having a robust banking system, the US financial sector has one segment that could....Read More

Blog

Blog

EU banks: better equipped to ride out the sto

Old habits die hard In every financial crisis, when market crashes, it brings down everyt....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox